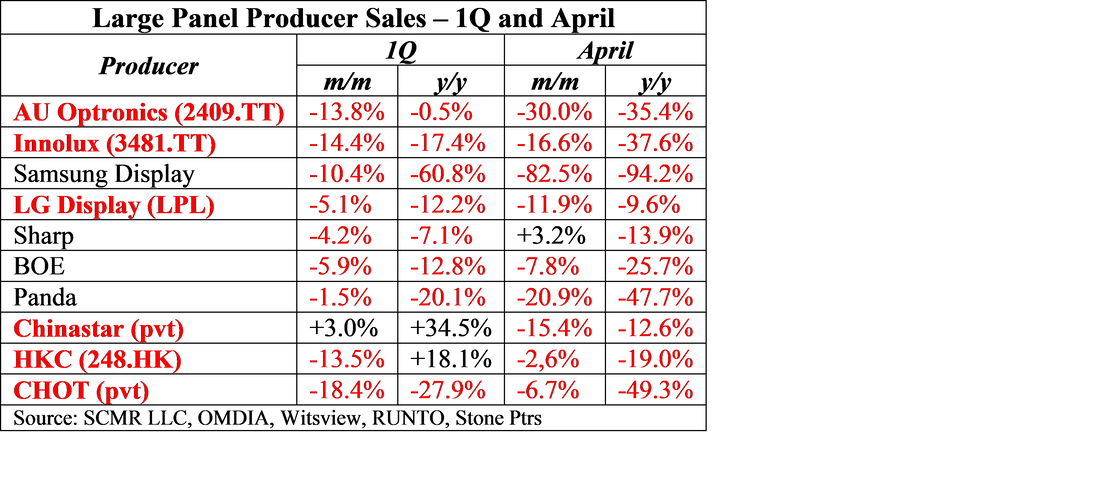

AU Optronics/Innolux Merger Rumors Squelched

Over the last few days various sites have speculated that Taiwanese panel producers AU Optronics (2409.TT) and Innolux (3481.TT) would merge to create an LCD powerhouse that could compete with Chinese panel producers, such as BOE (200725.CH) and Chinastar (pvt). Given the poor performance seen by LCD panel producers in April and a continuation of same for the 2nd quarter, we expect drawing such conclusions would be a way for some to refocus the declining profitability of the display space toward such combinations that would give promise to a new order, but it seems that neither company was interested in the idea and Innolux went as far as to appeal to the media not to publish false reports that would mislead the public. AUO indicated that the transformation it has made over the last few years, moving from commodity panel production to more specialized displays, and branching out into Mini-LED and Micro-LED technology, have performed well and are creating value, so a merger would only be viable if it were synergistic to that goal.

The problem with such a merger is the capacity that both parties already have and how that plays into today’s market. Both AUO and Innolux have significant Gen 5 and Gen 6 capacity, which is ideal for IT panel production, but combined lave less Gen 8 capacity than China’s leading TV panel producer BOE, which is essential for efficient TV panel production. Both also have a number of Gen 4 and Gen 5 fabs, which are relatively old and therefore inefficient by current standards. We note that AUO has recently indicated that it is planning to build a new Gen 8.5 LCD fab and has expanded capacity at its fab in Kunshan, the first capacity expansion project that the company has made in many years, and Innolux has stated it will not build any new LCD capacity but will upgrade existing LCD lines. With the continuing downturn in LCD panel pricing, we expect such plans are less prone to be rushed and the result of combining existing assets would likely also be less crucial.

The problem with such a merger is the capacity that both parties already have and how that plays into today’s market. Both AUO and Innolux have significant Gen 5 and Gen 6 capacity, which is ideal for IT panel production, but combined lave less Gen 8 capacity than China’s leading TV panel producer BOE, which is essential for efficient TV panel production. Both also have a number of Gen 4 and Gen 5 fabs, which are relatively old and therefore inefficient by current standards. We note that AUO has recently indicated that it is planning to build a new Gen 8.5 LCD fab and has expanded capacity at its fab in Kunshan, the first capacity expansion project that the company has made in many years, and Innolux has stated it will not build any new LCD capacity but will upgrade existing LCD lines. With the continuing downturn in LCD panel pricing, we expect such plans are less prone to be rushed and the result of combining existing assets would likely also be less crucial.

RSS Feed

RSS Feed