Panel Producer Metrics - November

Earlier this week we reviewed panel pricing for December and the year, and we are close to having full data for panel producer sales in December and for the full year. In the interim, we show results for November, which were slightly better than October, and walk through the display industry on a regional and company by company basis.

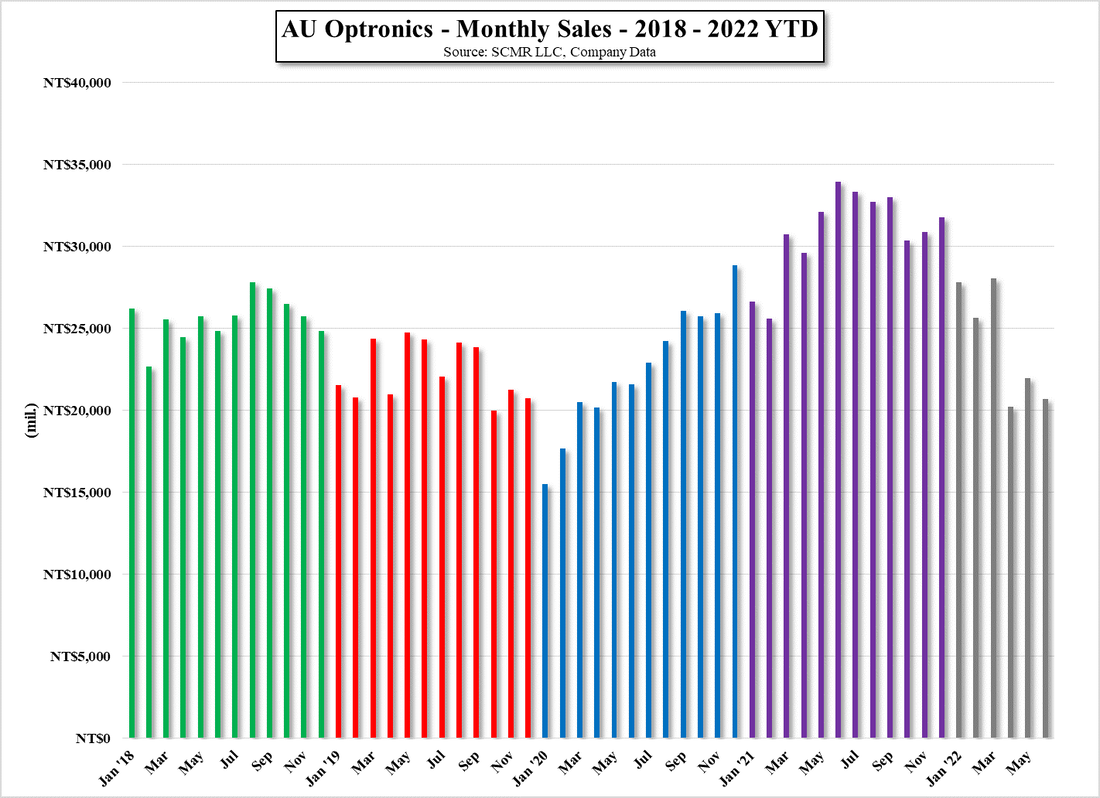

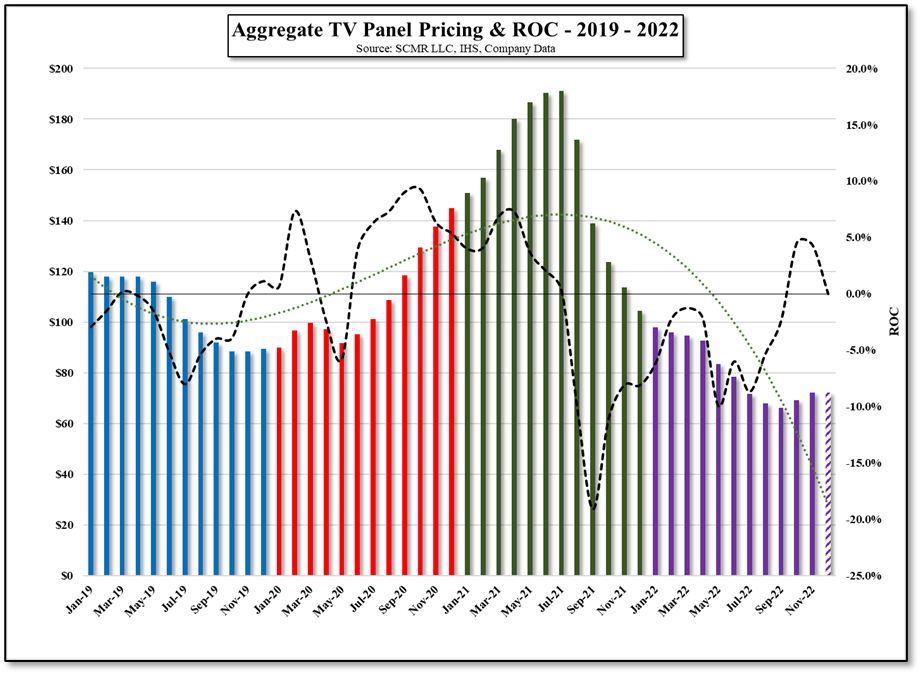

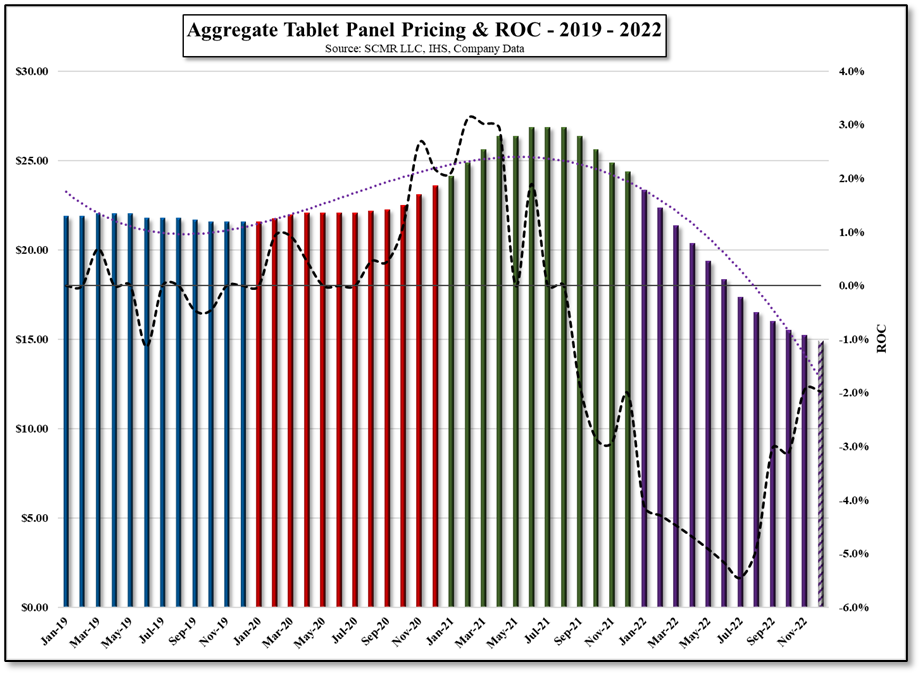

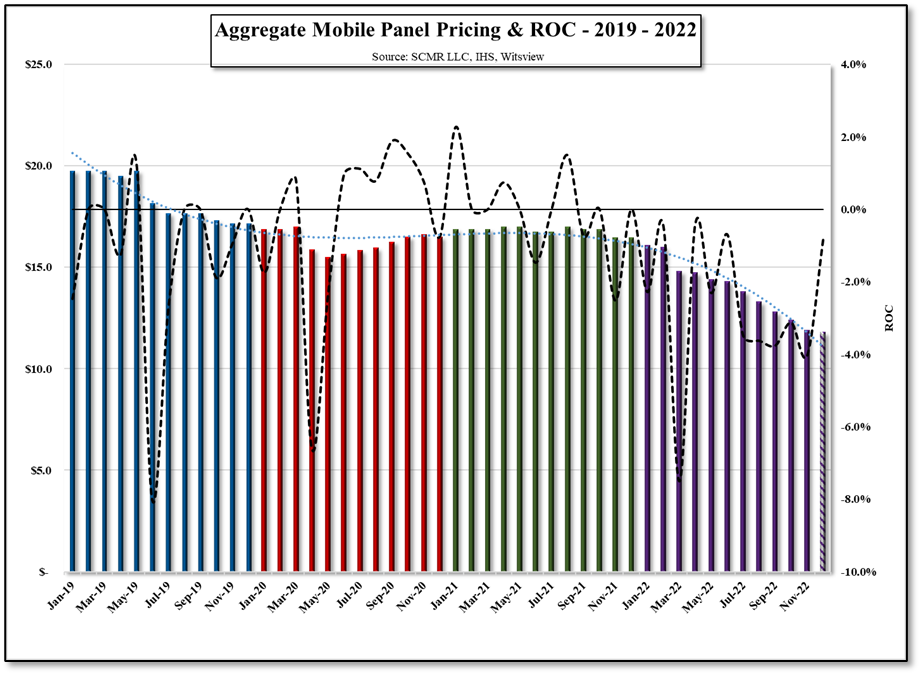

November large panel revenue was up 0.8% m/m but down 30.9% y/y which puts the 2022 YTD (11 months) down 25.8% y/y, while large panel shipments are down 10.7% over the same period. On a regional basis, both Taiwan and Korea saw m/m revenue increases, surprising in that Samsung Display (pvt) has been winding down large panel LCD production capacity as has LG Display (LPL) to a lesser degree. Chinese large panel LCD producers saw their overall revenue share decline, following October’s rise, and has seen its revenue share decline YTD from 49.0% in December of last year to 46.6% in November of this year, while Korea has seen its share increase from 19.0% last December to 28.0% this year.

November large panel revenue was up 0.8% m/m but down 30.9% y/y which puts the 2022 YTD (11 months) down 25.8% y/y, while large panel shipments are down 10.7% over the same period. On a regional basis, both Taiwan and Korea saw m/m revenue increases, surprising in that Samsung Display (pvt) has been winding down large panel LCD production capacity as has LG Display (LPL) to a lesser degree. Chinese large panel LCD producers saw their overall revenue share decline, following October’s rise, and has seen its revenue share decline YTD from 49.0% in December of last year to 46.6% in November of this year, while Korea has seen its share increase from 19.0% last December to 28.0% this year.

From a company perspective, out of the 10 large panel LCD producers that make up the bulk of sales for the space, 4 saw positive m/m results for November, while the remaining six saw m/m declines. Of the four that saw positive m/m revenue growth in November, two were Taiwanese, one Korean, and one Chinese, while none are up on a y/y basis. As noted, industry revenue is down 30.9% y/y for the 11 months and looking at the top 10 large panel LCD display producers, only two are above the average, with the remaining 8 below. LG Display performed the best on a YTD y/y basis and CEC Panda (600775.CH) the worst. All in November was, as expected, a relatively quiet month, as panel producers remained beholden to continuing weakness in China, weak early holiday sales, and little change in panel pricing. We expect little change again in December.

From a company perspective, out of the 10 large panel LCD producers that make up the bulk of sales for the space, 4 saw positive m/m results for November, while the remaining six saw m/m declines. Of the four that saw positive m/m revenue growth in November, two were Taiwanese, one Korean, and one Chinese, while none are up on a y/y basis. As noted, industry revenue is down 30.9% y/y for the 11 months and looking at the top 10 large panel LCD display producers, only two are above the average, with the remaining 8 below. LG Display performed the best on a YTD y/y basis and CEC Panda (600775.CH) the worst. All in November was, as expected, a relatively quiet month, as panel producers remained beholden to continuing weakness in China, weak early holiday sales, and little change in panel pricing. We expect little change again in December.

Large Panel LCD Display Shipments - 2020 - 2022 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO, Company Data

RSS Feed

RSS Feed