April Taiwan Panel Debacle

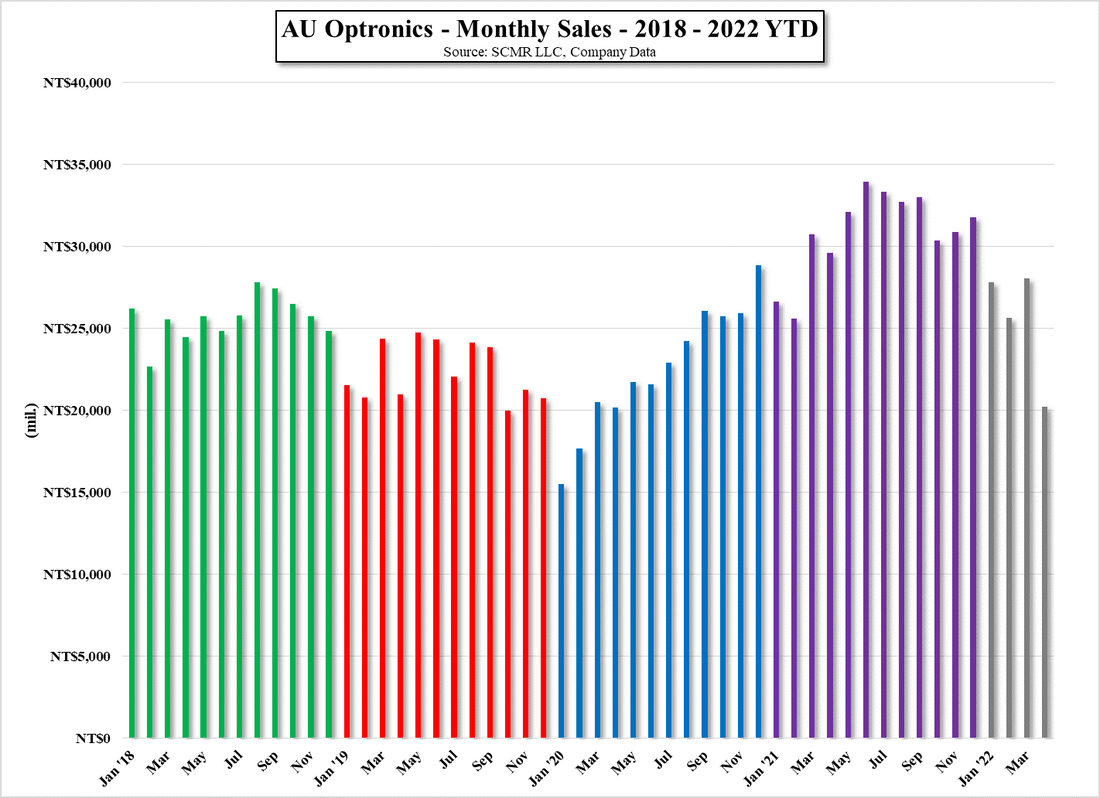

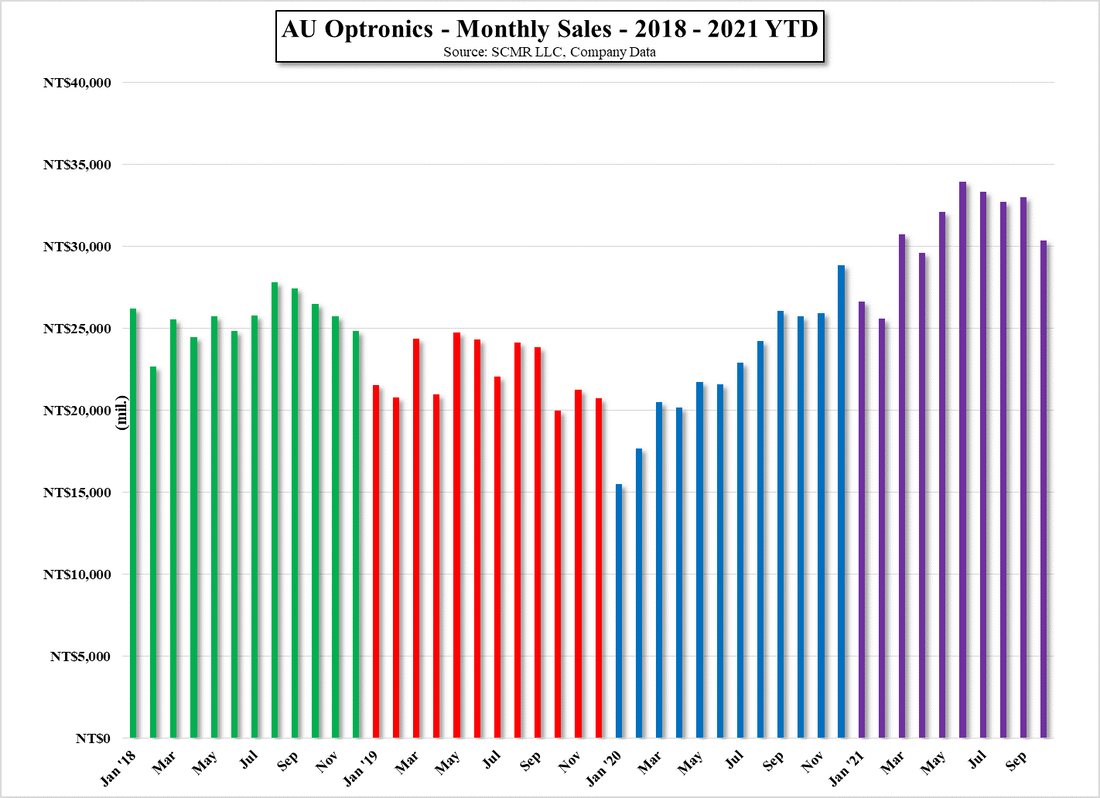

April was not a good month for panel producers in Taiwan, and likely similar results would be found for other panel producers. AU Optronics (2409.TT) reported April sales of NT$20.22b ($682.37m US), down 27.9% m/m and down 31.7% y/y. Area shipments were also down 73.9% m/m and down 23.7% y/y. To put this data in perspective, the drop in sales seen by AUO was the largest m/m decline seen since November 2008, the y/y decline was the largest seen since January 2009, and the panel area shipments were the lowest since AUO began reporting those numbers in February 2020. Typically these monthly numbers are reported without any commentary however this month AUO added the following to the report, which we feel sums up the month quite succinctly:

“Revenues dropped sharply in April, largely due to weaker demand amid macroeconomic uncertainties caused by war and inflation, together with higher channel inventory resulted from previous port congestions and container shortage. In addition, eastern China has introduced strict Covid-19 related lockdowns since April. Given the challenges of lack of workers, combined with supply chain disruptions under these lockdown measures, the Company has lowered utilization rates at its production sites in Kunshan and Suzhou. Meanwhile, shipments to customers were also impacted by these lockdown restrictions. Currently, lockdown measures were lifted in certain areas while the pandemic gradually eased. However, it may still take some time for market to return to normal.”

“Revenues dropped sharply in April, largely due to weaker demand amid macroeconomic uncertainties caused by war and inflation, together with higher channel inventory resulted from previous port congestions and container shortage. In addition, eastern China has introduced strict Covid-19 related lockdowns since April. Given the challenges of lack of workers, combined with supply chain disruptions under these lockdown measures, the Company has lowered utilization rates at its production sites in Kunshan and Suzhou. Meanwhile, shipments to customers were also impacted by these lockdown restrictions. Currently, lockdown measures were lifted in certain areas while the pandemic gradually eased. However, it may still take some time for market to return to normal.”

AU Optronics - Monthly Sales - 2019 - 2022 YTD - Source: SCMR LLC, Company Data

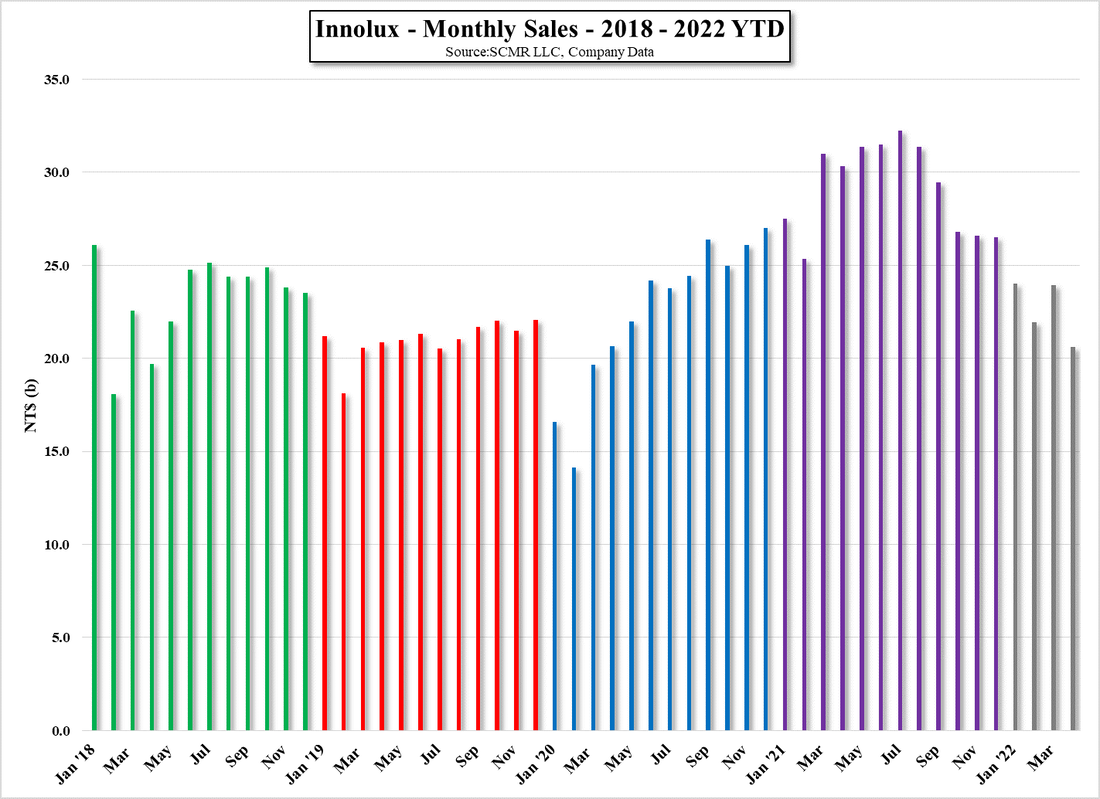

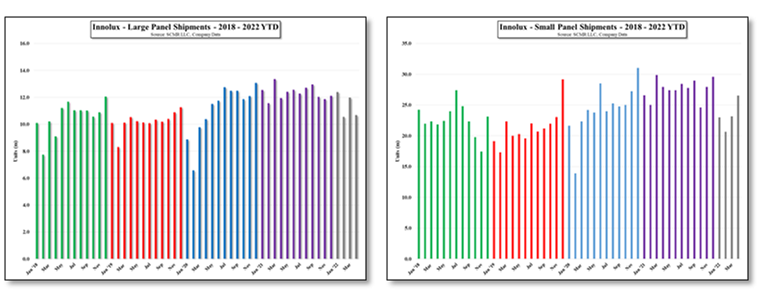

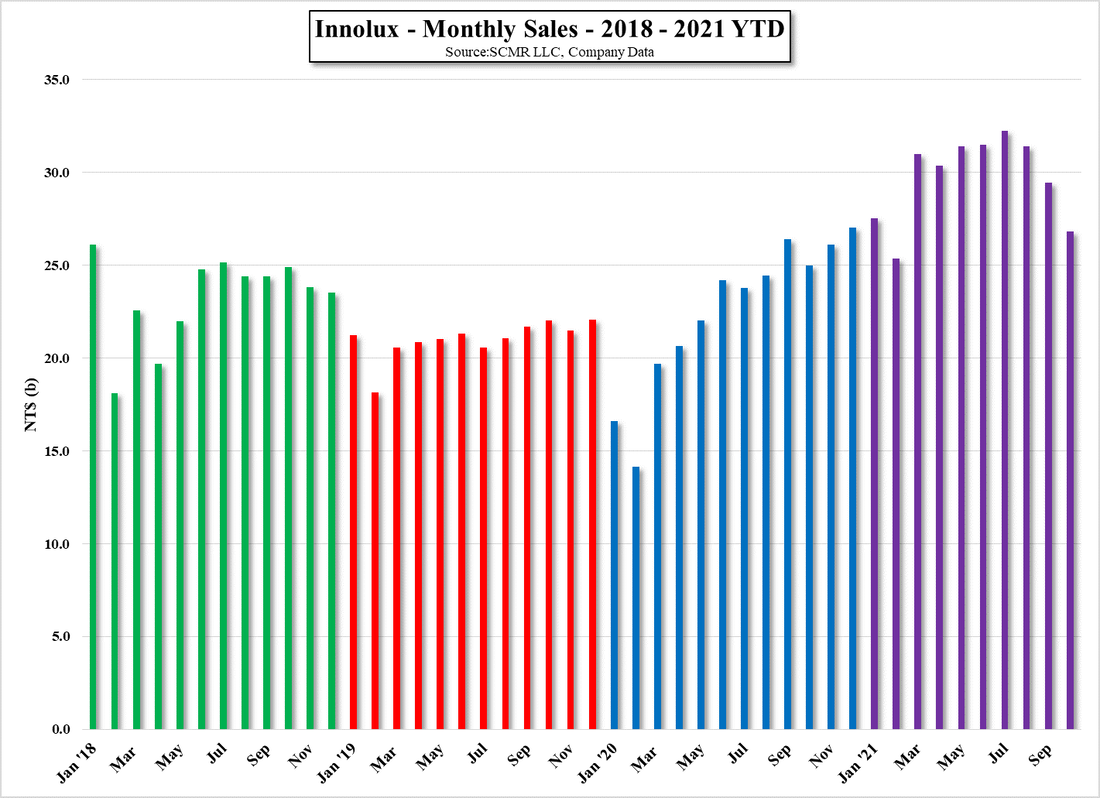

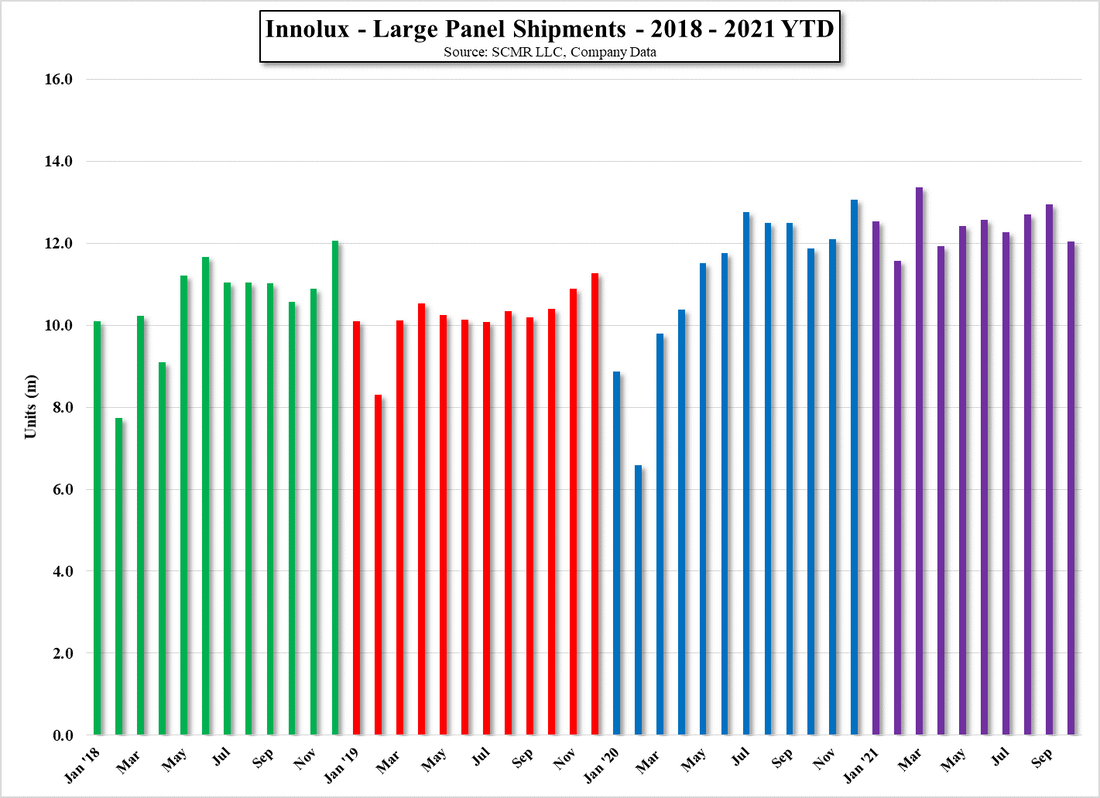

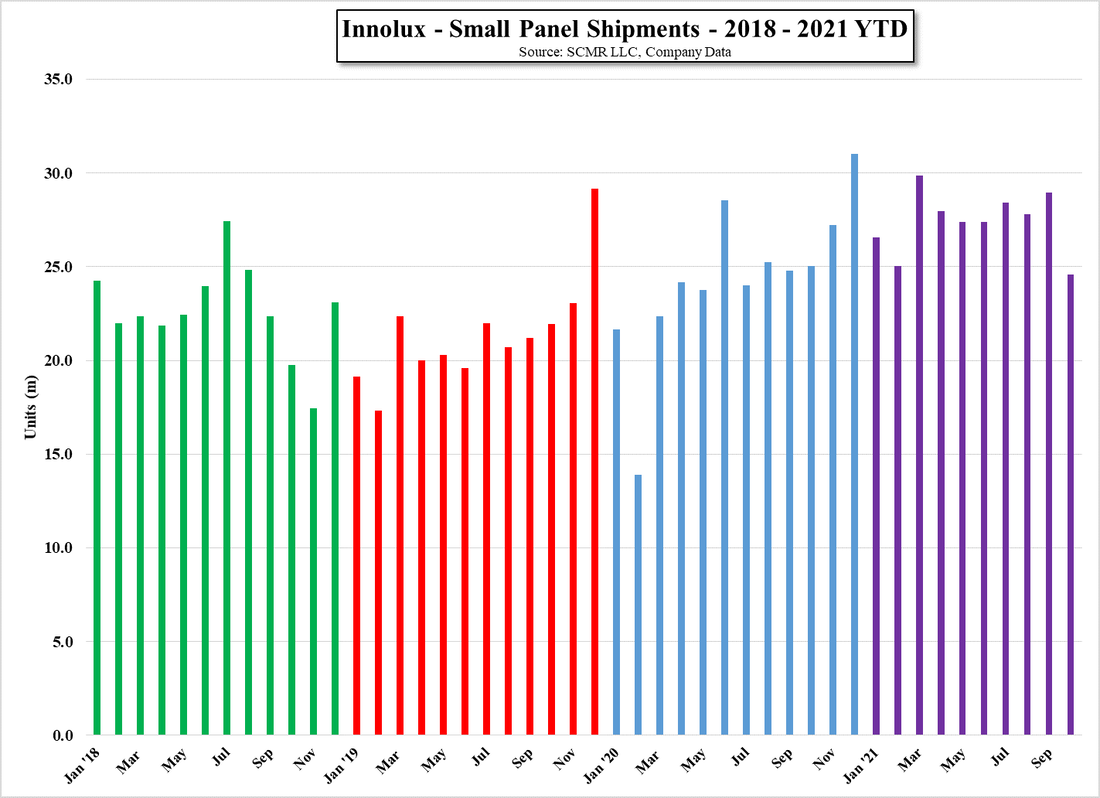

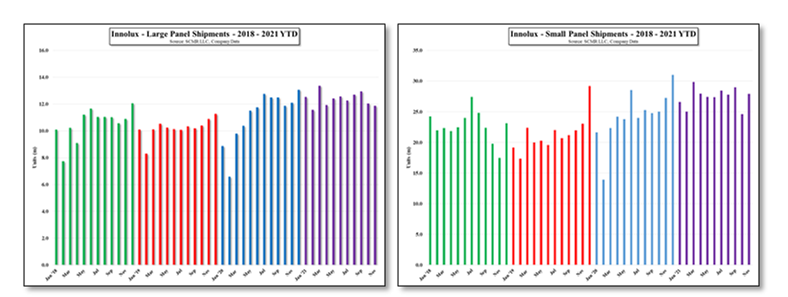

Innolux (3481.TT) did not fare much better in April reporting sales of NT$20.6b ($695.2m US), down 13.9% m/m and down 32.1% y/y. Innolux shipped 10.7m large panels in April, down 10.9% m/m and down 10.6% y/y and shipped 26.55m small panels during the month, which was up 14.5% m/m but down 5.0% y/y. Innolux made no comments about the results for the month

Innolux - Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

Innolux - Large & Small Panel Shipments - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

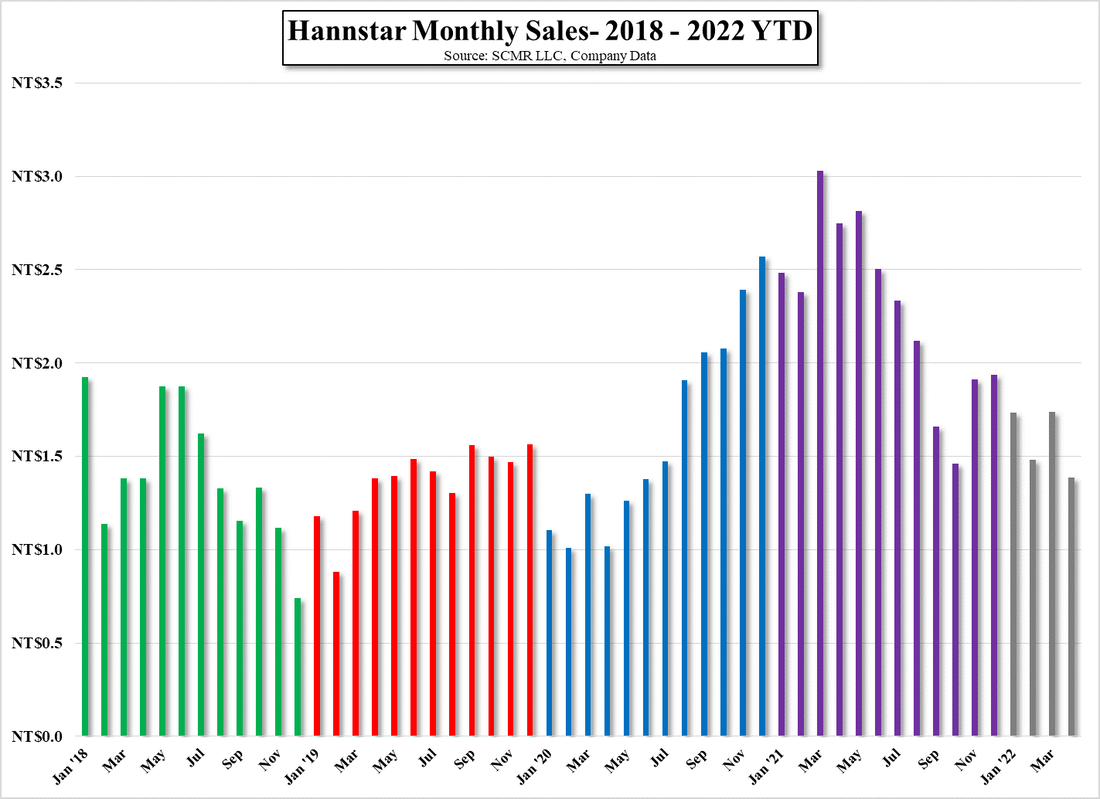

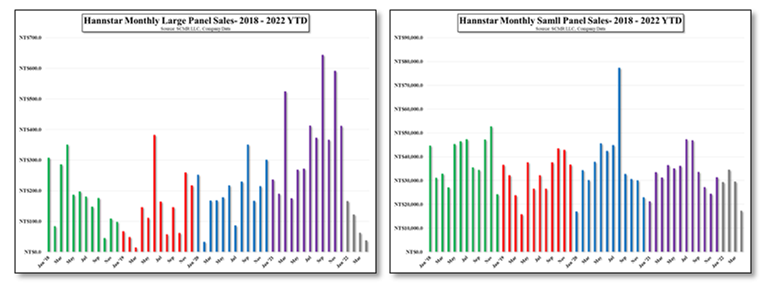

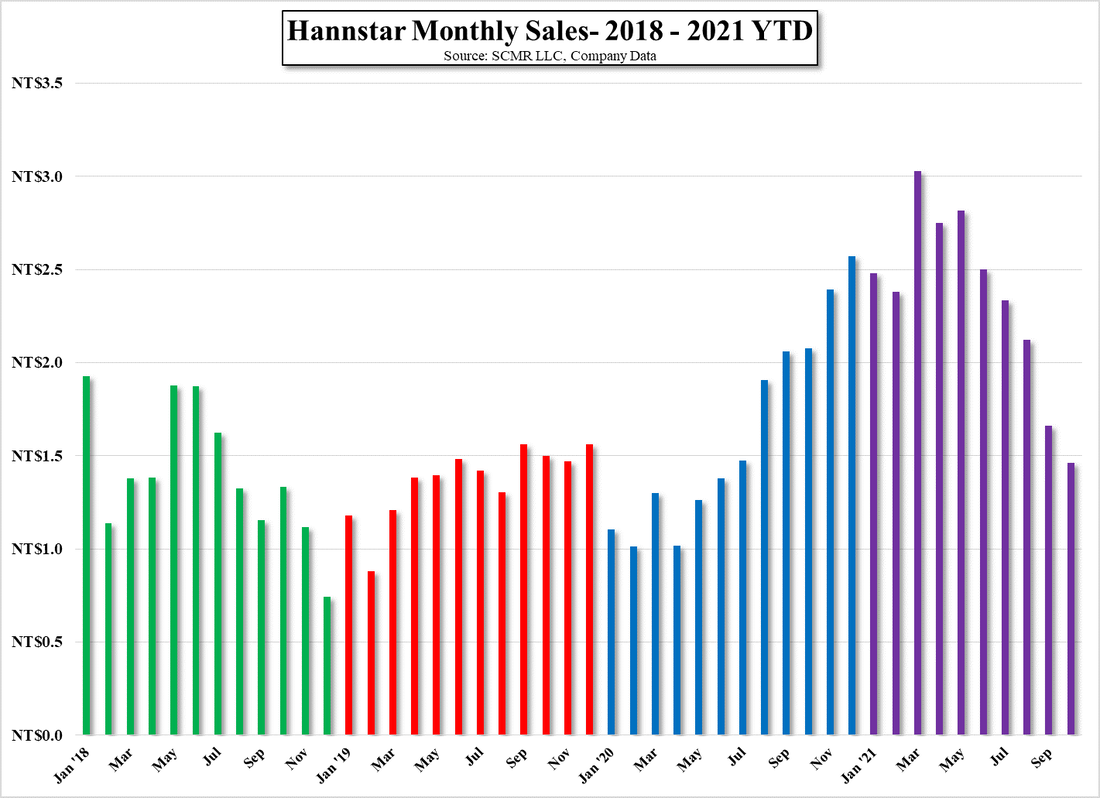

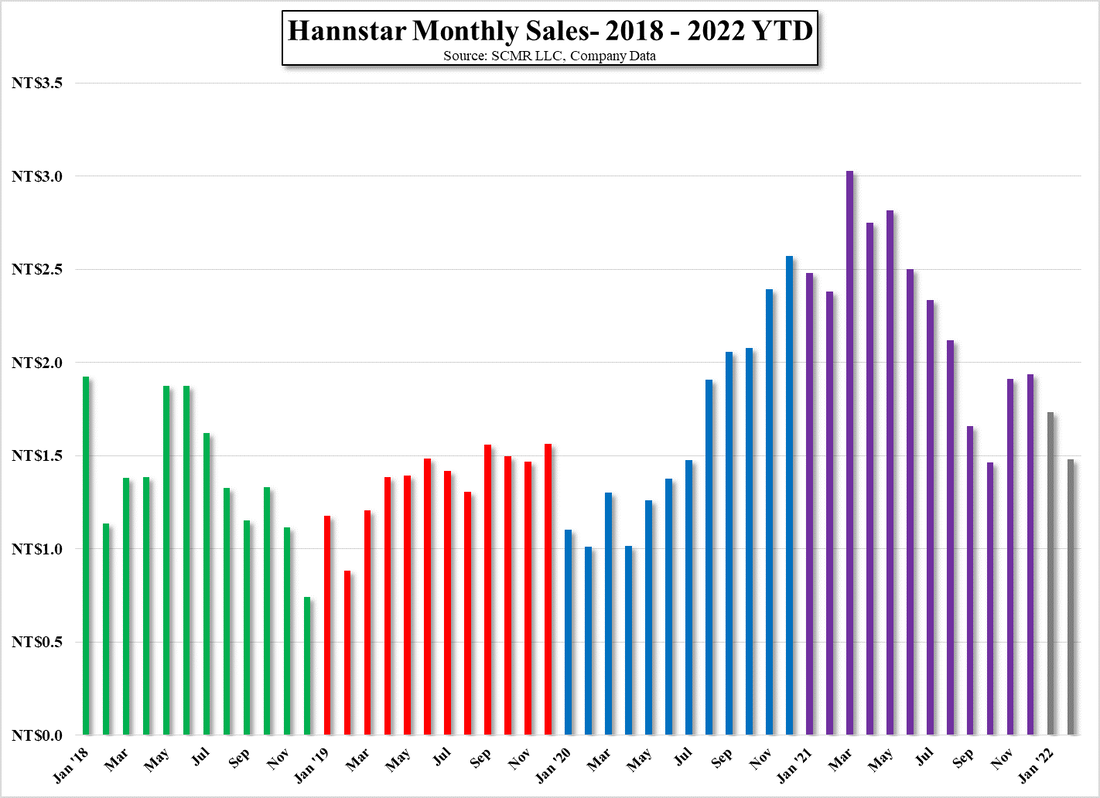

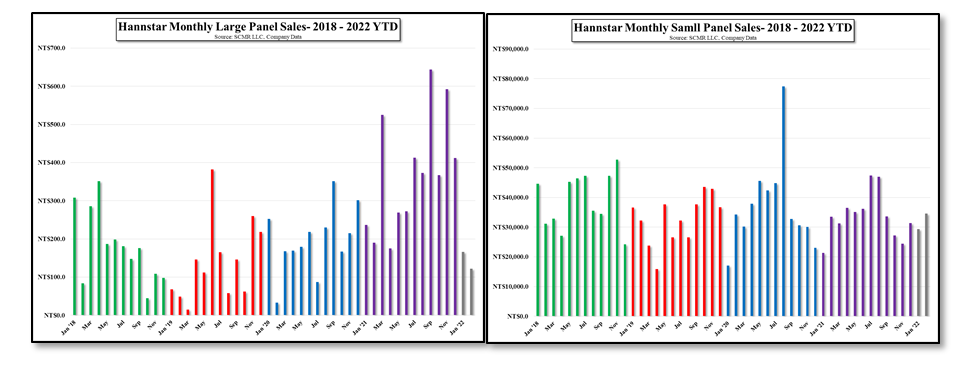

Hannstar Display (6116.TT), who is primarily a small panel display producer, saw sales of NT$1.39b ($46.91m US), down 20.3% m/m and down 49.6% y/y, while large panel shipments declined to 38,000, down 39.7% m/m and down 78.3% y/y, while small panel shipments declined to 17.32m, down 41.4% m/m and down 52.6% y/y.

Hannstar Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

Hannstar Display Large & Small Panel Shipments - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

Characterizing April as a bad month for Taiwanese panel producers is a bit of an understatement, although some fared better than others. As panel producers face lower sales and bring down utilization rates to compensate for weaker demand, we expect to see margins turn negative and if the recovery from China’s COVID lockdowns and the war in Ukraine take much of May, the 2nd quarter will be quite poor, even with a bit of a snap back in June. While each panel producer will see different results in May and June, we expect Chinese panel producers will still try to maintain shipment levels by continuing to discount panel prices into June, but will soon see those prices fall below cash costs, at which point they have no choice but to lower utilization rates. While those lower utilization rates will lead to more stable panel prices in 3Q demand does not seem to be strong enough to warrant increasing utilization to previous levels, which means 3Q panel results will be negative on a y/y basis. We expect the only hope for results better than this scenario would be if China gets COVID under control and there is a bit of a recovery in the Chinese economy, but that is an optimistic scenario.

RSS Feed

RSS Feed