China’s Double 11 2025: Why the Record GMV Hides Stagnant Daily Sales & The Retail Data Crisis

Double 11, Singles Day, or just 11/11, it is the biggest shopping holiday in the world, outstripping Black Friday and Cyber Monday combined. Originally a celebration instigated by college students (singles) in the 1990’s, Alibaba (BABA), one of China’s largest e-commerce retailers turned it into a commercial event in 2009 and it has grown ever since.

The Only True Metric: Daily Gross Merchandise Value (Daily GMV)

In earlier periods Chinese retailers, like JD.com (JD) and Douyin (pvt) would release GMV (Gross Merchandise Value) reports after the holiday, extoling the holiday’s growth and their own, but as consumption growth slowed in recent years, retailers no longer supplied such information, with results being based on 3rd party estimates rather than actual reports from retailers. Another mitigating factor is the number of days the GMV covers, as it has changed over the years, increasing from 11 days in 2020 to 36 days this year. This means that the only true measure of the holiday’s success is the total GMV/number of days, or daily GMV, a very different metric from the published gross GMV data.

Decoding the Spin: 2025 Syntun & Media Highlights

The press release from China’s Syntun does not state the GMV on a y/y basis, but the headline, which reads “The GMV during China ‘Double 11 Shopping Festival’ reached 1695 billion CNY (~238 billion USD)” would lead one to believe that the number estimated was a positive one, and the copy continued that effort with phrases like “this year's festival has transcended its role as a mere shopping frenzy, reflecting a profound transformation within the retail ecosystem and deep technological integration”, and does not miss the chance to reference AI (“the comprehensive integration of AI technology has emerged as a defining feature...”).

One can see that the data shown in the 2025 Chinese media snippets below have little or no base from which to verify the calculation

But the bottom line is that nothing expands forever and manufacturing headlines that would imply growth to the general public is not unusual in China or any other country. The Chinese government is very oriented toward proving it can ‘outgrow’ the US and other large economies, and while we expect the state did not force Alibaba and others to stop showing GMV that might point to slow or no growth, we expect it is psychologically ingrained enough that retailers will follow that path without hesitation.

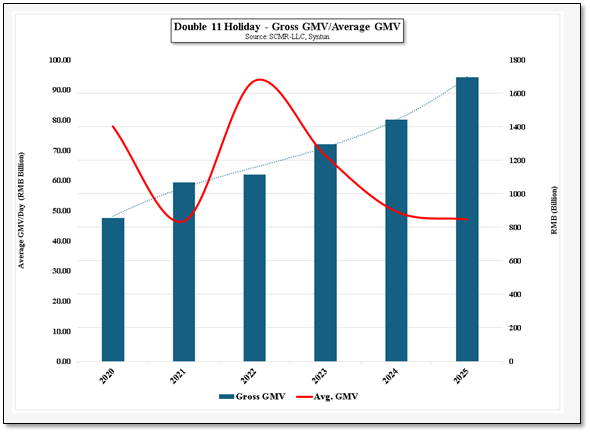

All of that said, Figure 1 shows the reported GMV without compensation for the number of days included, and the average GMV which compensates for the total number of days included in the GMV, which paints a different picture, one where the average GMV/day seems to have leveled off for the last two years. This is consistent with Chinese retail (on-line and physical) results as the ‘New for Old’ subsidies wind down this year and the generally slower consumer electronics growth seen during previous holidays this year. 2026 will be a test for the Chinese CE space as we expect another year of consumer subsidies will have a diminished effect. Consumers have borrowed against forward sales now for 18 months+ and we expect there will have to be a ‘true up’ quarter sooner or later.

The Only True Metric: Daily Gross Merchandise Value (Daily GMV)

In earlier periods Chinese retailers, like JD.com (JD) and Douyin (pvt) would release GMV (Gross Merchandise Value) reports after the holiday, extoling the holiday’s growth and their own, but as consumption growth slowed in recent years, retailers no longer supplied such information, with results being based on 3rd party estimates rather than actual reports from retailers. Another mitigating factor is the number of days the GMV covers, as it has changed over the years, increasing from 11 days in 2020 to 36 days this year. This means that the only true measure of the holiday’s success is the total GMV/number of days, or daily GMV, a very different metric from the published gross GMV data.

Decoding the Spin: 2025 Syntun & Media Highlights

The press release from China’s Syntun does not state the GMV on a y/y basis, but the headline, which reads “The GMV during China ‘Double 11 Shopping Festival’ reached 1695 billion CNY (~238 billion USD)” would lead one to believe that the number estimated was a positive one, and the copy continued that effort with phrases like “this year's festival has transcended its role as a mere shopping frenzy, reflecting a profound transformation within the retail ecosystem and deep technological integration”, and does not miss the chance to reference AI (“the comprehensive integration of AI technology has emerged as a defining feature...”).

One can see that the data shown in the 2025 Chinese media snippets below have little or no base from which to verify the calculation

- “Electronics categories showed bifurcated performance. AI glasses sales jumped 25x YoY as consumers adopted emerging form factors, according to People’s Daily. “

- “Smart glasses increased 346%, while robotics brands recorded double-digit growth, the article stated.”

- “Mobile phone and computer device sales concentrated on JD, which captured 56.9% and 62.7% market shares respectively in these segments, according to China Britain Business Council analysis.”

- “Home appliances benefited directly from government trade-in subsidies. 139 brands exceeded RMB 14M in GMV, with over 9,600 home appliance and furniture brands doubling sales YoY, according to Queue-it’s November 2025 statistics compilation.”

But the bottom line is that nothing expands forever and manufacturing headlines that would imply growth to the general public is not unusual in China or any other country. The Chinese government is very oriented toward proving it can ‘outgrow’ the US and other large economies, and while we expect the state did not force Alibaba and others to stop showing GMV that might point to slow or no growth, we expect it is psychologically ingrained enough that retailers will follow that path without hesitation.

All of that said, Figure 1 shows the reported GMV without compensation for the number of days included, and the average GMV which compensates for the total number of days included in the GMV, which paints a different picture, one where the average GMV/day seems to have leveled off for the last two years. This is consistent with Chinese retail (on-line and physical) results as the ‘New for Old’ subsidies wind down this year and the generally slower consumer electronics growth seen during previous holidays this year. 2026 will be a test for the Chinese CE space as we expect another year of consumer subsidies will have a diminished effect. Consumers have borrowed against forward sales now for 18 months+ and we expect there will have to be a ‘true up’ quarter sooner or later.

Figure 1 - Double 11 Holiday Gross GMV/Average GMV - Source: SCMR-LLC, Syntu

RSS Feed

RSS Feed