Hail Mary

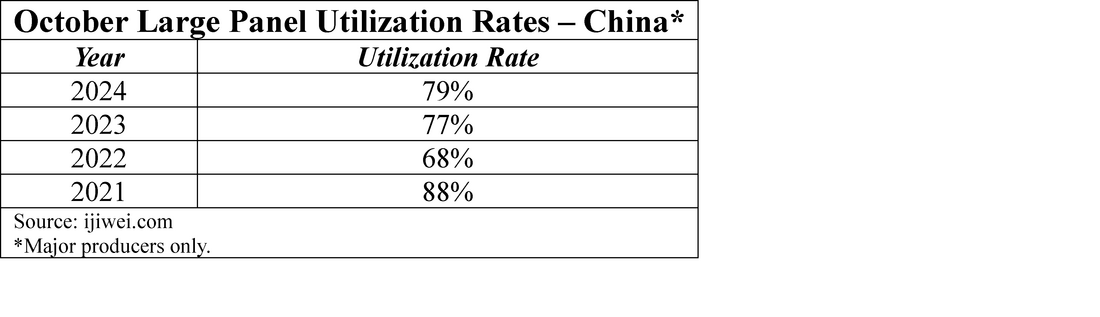

Yesterday we noted how Chinese LCD panel producers had made a philosophical change in the way in which they managed panel pricing over the last 18 months. We can add some more detailed information about the current state of sentiment among said LCD panel producers using utilization calculations based on their projected shut-down schedule for the Chinese National Holiday and Mid-Autumn Festival, which begins Monday October 1 and lasts for the week. The three major Chinese large panel LCD manufacturers will be shutting down their fabs for a number of days during the holiday in anticipation of relatively weak demand in 4Q. Thios is not as unusual as it sounds, but the number of days the fabs are closed is a good indicator of the level of concern that Chinese panel producers have for the upcoming quarter. The math for this year seems to prove out that while publicly each producer is careful about projecting extended demand weakness, the shutdown schedule points to the largest supply contraction in the last three years.

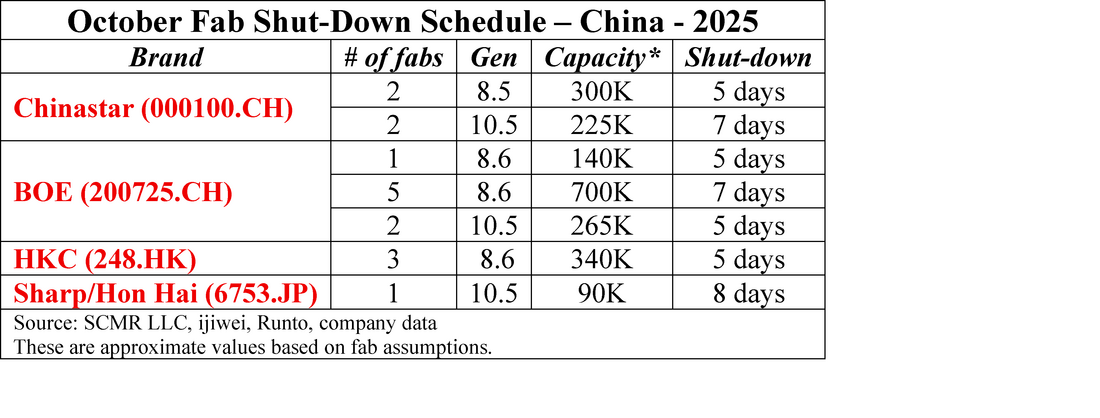

Here is what the shut-down schedule looks like:

So what does it mean in terms of utilization and capacity for October?

For each 15K line (Divide the capacity column by 15) a Gen 8.6 fab operating at 90% utilization can produce 54,000 65” equivalent panels per month. A 5 day hiatus for such a line would reduce the number of units produced from 54,000 to 44, 232, or an 18.1% reduction. It would reduce the monthly utilization rate from 90% to 73.7%. Gen 10.5 fabs have a unit count that is higher (6 units/sheet rather than 4) so the reduction percentage is the same but the reduction in the number of units is higher.

We have to make a number of assumptions to make these calculations, first of which is converting unit volumes to 65” equivalents. Second is adding a ½ day of zero production to account form shut-down and restart periods. Third, we have to make assumptions as to which fabs panel producers are shutting down, which makes the capacity estimates approximate. Fourth, we start by assuming that all fabs are typically operating at 90% utilization. Perhaps a bit optimistic but a starting point.

All in, the utilization cuts indicated above show that Chinese panel producers are a bit less optimistic about the 4th quarter than they might be indicating publicly but are more willing to reduce utilization than to make price concessions that might keep fabs full. The secondary problem is that many of these fabs have been operating just above break-even for the 3rd quarter, certainly lower than 2Q, so a price reduction would likely put the fabs in a loss position for the 4th quarter as it tends to be difficult to bring back panel price reductions toward year end. Utilization drops are an internal adjustment (See yesterday’s note for more detail) so they can be more easily reversed and have less of a bottom line impact than product price reductions.

Given that the demand outlook for the holiday season is not robust, panel producers have one last hope for a better 4th quarter, and that is based on the idea that brand panel buyers will anticipate a price increase in 1Q ’26 and pull-those 1Q orders into 4Q. Unfortunately we have little hope that such a scenario will play out to a large enough degree to offset inherently weak 4Q demand, and even if it does play out, it would leave a weaker 1Q to deal with in a few short months. While we can never rule anything out completely, we are unsure that these utilization cuts will even be adequate to tighten capacity significantly enough to avoid a 4Q loss for many producers and we are beginning to feel that not only will we see these aggressive utilization cuts but there is a chance that panel producers will also have to cut prices a bit to pull panel buyers out of their languor. It’s a Hail Mary scenario, but you never know.

For each 15K line (Divide the capacity column by 15) a Gen 8.6 fab operating at 90% utilization can produce 54,000 65” equivalent panels per month. A 5 day hiatus for such a line would reduce the number of units produced from 54,000 to 44, 232, or an 18.1% reduction. It would reduce the monthly utilization rate from 90% to 73.7%. Gen 10.5 fabs have a unit count that is higher (6 units/sheet rather than 4) so the reduction percentage is the same but the reduction in the number of units is higher.

We have to make a number of assumptions to make these calculations, first of which is converting unit volumes to 65” equivalents. Second is adding a ½ day of zero production to account form shut-down and restart periods. Third, we have to make assumptions as to which fabs panel producers are shutting down, which makes the capacity estimates approximate. Fourth, we start by assuming that all fabs are typically operating at 90% utilization. Perhaps a bit optimistic but a starting point.

All in, the utilization cuts indicated above show that Chinese panel producers are a bit less optimistic about the 4th quarter than they might be indicating publicly but are more willing to reduce utilization than to make price concessions that might keep fabs full. The secondary problem is that many of these fabs have been operating just above break-even for the 3rd quarter, certainly lower than 2Q, so a price reduction would likely put the fabs in a loss position for the 4th quarter as it tends to be difficult to bring back panel price reductions toward year end. Utilization drops are an internal adjustment (See yesterday’s note for more detail) so they can be more easily reversed and have less of a bottom line impact than product price reductions.

Given that the demand outlook for the holiday season is not robust, panel producers have one last hope for a better 4th quarter, and that is based on the idea that brand panel buyers will anticipate a price increase in 1Q ’26 and pull-those 1Q orders into 4Q. Unfortunately we have little hope that such a scenario will play out to a large enough degree to offset inherently weak 4Q demand, and even if it does play out, it would leave a weaker 1Q to deal with in a few short months. While we can never rule anything out completely, we are unsure that these utilization cuts will even be adequate to tighten capacity significantly enough to avoid a 4Q loss for many producers and we are beginning to feel that not only will we see these aggressive utilization cuts but there is a chance that panel producers will also have to cut prices a bit to pull panel buyers out of their languor. It’s a Hail Mary scenario, but you never know.

Figure 2 - "Hail Mary" - Source: SCMR LLC, Nano-banana

RSS Feed

RSS Feed