Modus Operandi

The panel industry tends to be dominated by a small number of producers, with those producers located in a common region. Over the years the dominating panel producers and those regions have changed, with the early leader in the LCD space being Japanese companies like Sharp (6753.JP) or Sony (SNE). Over time South Korea became the leading LCD producing country with Samsung Display (pvt) and LG Display (LPL) taking the lead as Japan’s influence diminished, but as early as 2004 China’s BOE (200725.CH) began building out LCD capacity followed by Chinastar (000100.CH) in 2011, Panda (553.HK), and Tianma (000050.CH) in 2011, and others in 2017 and beyond.

The Chinese strategy, similar to what was used to dominate the global LED industry, was to offer low-priced generic panels to customers in order to build market share, while the Chinese government subsidized the construction and operations of many local fabs. This had a profound effect on South Korean suppliers, who realized relatively quickly that they could not compete with Chinese LCD panel producers on price in the LCD space. In 2020 Samsung Display announced it would cease all LCD panel production, although a spurt in demand put that timeline off until mid-year 2022. LG Display indicated that it would do the same with its large panel production, with both shifting to OLED panel production, although LGD did not end large panel production until it sold its last remaining large panel fab to Chinastar in March of this year.

During these ‘transition years’, China’s fab policy remained the same, with panel price being the leverage that its producers used most often to continue to grow share, but we believe that in 2024 that policy changed and Chinese panel producers began to use utilization as a way to gain stability and profitability rather than price. While it is extremely difficult to isolate how coordinated this change was and is among China’s larger LCD panel producers, there is certainly state and local government influence considering the loans, grants and tax breaks the government has given to these companies, and the fact that the state and local governments are typically the largest shareholders in these seemingly private companies.

We believe that Chinese LCD panel producers have faced large depreciation issues, a result of government sponsored and financed capacity growth, which has weighed heavily on bottom line results, and made it difficult for the government to see any return on these large investments. This was less of an issue when the Chinese economy was growing rapidly, but as its economy slows, the need to see some return on investment in the display space becomes more intense. This is exaggerated by the additional subsidies the government uses to stimulate the economy through direct-to-consumer subsidies, and the more recent AI race, where massive funding is needed to maintain China’s Ai standing on a global basis.

The Chinese government (local governments also) seem to have tightened their purse strings when it comes to the display space. Case-in-point being the Visionox (002387.CH) Gen 8.6 IT OLED project, which was stated to be a hybrid blend of a FMM Vacuum deposition line and an ink-jet printing line (the world’s first intended for mass production) using the company’s VIP technology. The project was initially thought to be starting with the vacuum deposition line, to hasten the mass production timeline, and to give the fab a way to compete against rivals in this relatively new product space. It seems that financing for the project was unable to be obtained given that concept, and only when the initial line was changed to ink-jet did the government see enough differentiation to finance the project.

So what does this mean? It means that Chinese panel producers have to pay more attention to the bottom line and produce positive financial results, eventually leading to a way for these companies to buy back the shares owned by the government. This makes the most sense when a fab is fully depreciated although we expect the mechanics are not necessarily developed by the companies themselves, as was the case with the recent SMIC (688981.CH) purchase of the National Integrated Circuit Industry Investment Fund ("Big Fund") stake in SMIC North, making it a wholly owned entity and giving the fund liquidity.

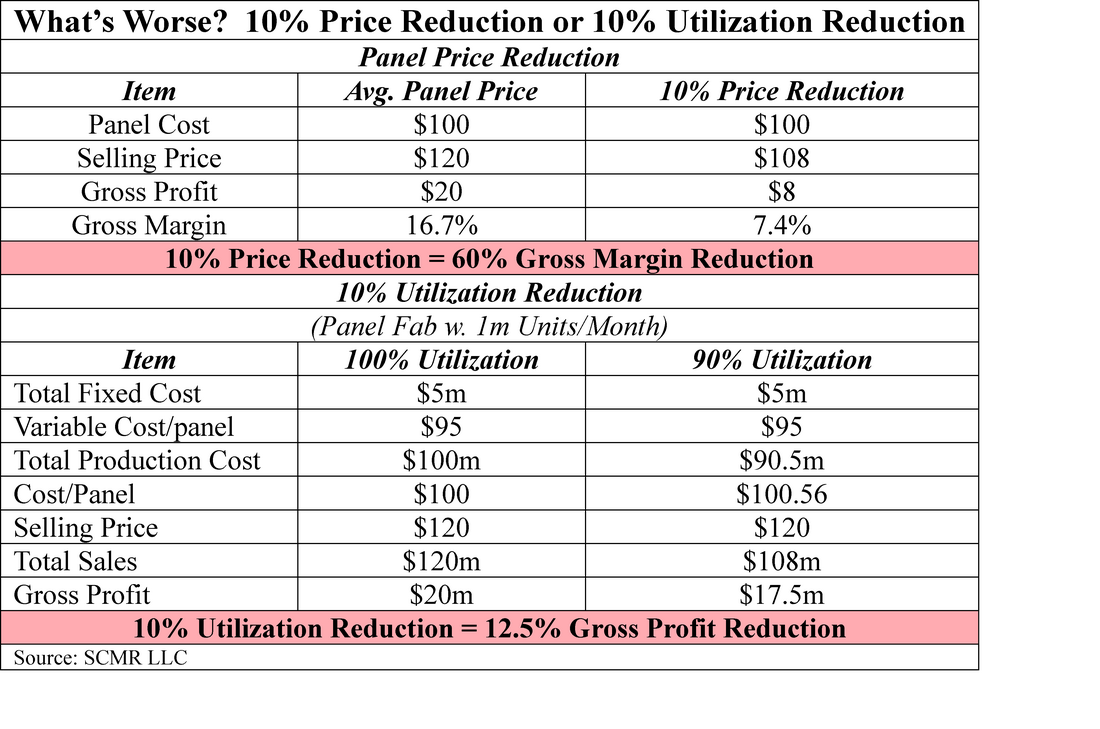

But, the bigger question is, how does this change affect China’s LCD display producers? As we noted earlier, China’s LCD panel producers have been using utilization rate changes rather than price changes to generate a more profitable bottom line. Here’s why:

The Chinese strategy, similar to what was used to dominate the global LED industry, was to offer low-priced generic panels to customers in order to build market share, while the Chinese government subsidized the construction and operations of many local fabs. This had a profound effect on South Korean suppliers, who realized relatively quickly that they could not compete with Chinese LCD panel producers on price in the LCD space. In 2020 Samsung Display announced it would cease all LCD panel production, although a spurt in demand put that timeline off until mid-year 2022. LG Display indicated that it would do the same with its large panel production, with both shifting to OLED panel production, although LGD did not end large panel production until it sold its last remaining large panel fab to Chinastar in March of this year.

During these ‘transition years’, China’s fab policy remained the same, with panel price being the leverage that its producers used most often to continue to grow share, but we believe that in 2024 that policy changed and Chinese panel producers began to use utilization as a way to gain stability and profitability rather than price. While it is extremely difficult to isolate how coordinated this change was and is among China’s larger LCD panel producers, there is certainly state and local government influence considering the loans, grants and tax breaks the government has given to these companies, and the fact that the state and local governments are typically the largest shareholders in these seemingly private companies.

We believe that Chinese LCD panel producers have faced large depreciation issues, a result of government sponsored and financed capacity growth, which has weighed heavily on bottom line results, and made it difficult for the government to see any return on these large investments. This was less of an issue when the Chinese economy was growing rapidly, but as its economy slows, the need to see some return on investment in the display space becomes more intense. This is exaggerated by the additional subsidies the government uses to stimulate the economy through direct-to-consumer subsidies, and the more recent AI race, where massive funding is needed to maintain China’s Ai standing on a global basis.

The Chinese government (local governments also) seem to have tightened their purse strings when it comes to the display space. Case-in-point being the Visionox (002387.CH) Gen 8.6 IT OLED project, which was stated to be a hybrid blend of a FMM Vacuum deposition line and an ink-jet printing line (the world’s first intended for mass production) using the company’s VIP technology. The project was initially thought to be starting with the vacuum deposition line, to hasten the mass production timeline, and to give the fab a way to compete against rivals in this relatively new product space. It seems that financing for the project was unable to be obtained given that concept, and only when the initial line was changed to ink-jet did the government see enough differentiation to finance the project.

So what does this mean? It means that Chinese panel producers have to pay more attention to the bottom line and produce positive financial results, eventually leading to a way for these companies to buy back the shares owned by the government. This makes the most sense when a fab is fully depreciated although we expect the mechanics are not necessarily developed by the companies themselves, as was the case with the recent SMIC (688981.CH) purchase of the National Integrated Circuit Industry Investment Fund ("Big Fund") stake in SMIC North, making it a wholly owned entity and giving the fund liquidity.

But, the bigger question is, how does this change affect China’s LCD display producers? As we noted earlier, China’s LCD panel producers have been using utilization rate changes rather than price changes to generate a more profitable bottom line. Here’s why:

Aside from the financial aspects as shown above, changing utilization is an internal change made at the fab or company level and technically has no effect on other competitors, while price reductions not only affect other producers but are harder to recover from. Bringing up utilization after a short period is relatively easy compared to bring up prices after a reduction, adding to the attraction of using utilization as a tool rather than price.

In 2024 large panel prices increased only 0.5% while there were utilization swings on a m/m basis of over 18% (average was 2.1%/month), and we expect similar results for this year, although we expect pricing to be down a relatively small amount. Given the volatility we have seen this year regarding tariffs and how that has affected buying patterns, it is surprising how little prices for large panels have moved. We constantly hear feedback that panel producers, particularly Chinese panel producers are very hesitant to allow panel prices to fall and are managing utilization to keep a balance between supply and demand. They have had pull-in demand on their side for much of this year, so it has likely been a bit easier than last year, but the tactics seem to have changed from adjusting price to adjusting utilization, just as the focus on market share has now migrated to a focus on profitability.

In 2024 large panel prices increased only 0.5% while there were utilization swings on a m/m basis of over 18% (average was 2.1%/month), and we expect similar results for this year, although we expect pricing to be down a relatively small amount. Given the volatility we have seen this year regarding tariffs and how that has affected buying patterns, it is surprising how little prices for large panels have moved. We constantly hear feedback that panel producers, particularly Chinese panel producers are very hesitant to allow panel prices to fall and are managing utilization to keep a balance between supply and demand. They have had pull-in demand on their side for much of this year, so it has likely been a bit easier than last year, but the tactics seem to have changed from adjusting price to adjusting utilization, just as the focus on market share has now migrated to a focus on profitability.

RSS Feed

RSS Feed