Money Talks - How Government Subsidies are Influencing the OLED Fab Race

Display fabs are expensive, ranging from ~$300 million for existing fab upgrades to over $8 billion for current greenfield Gen 8.6 OLED fabs. There is a very substantial geographical imbalance in how these fabs are financed, with South Korea, home to Samsung Display (pvt) and LG Display (LPL), typically using company based fab financing, and China, home to BOE(200725.CH), Chinastar (pvt), Visionox (002387.CH), Tianma (000050.CH), HKC (248.HK), EverDisplay (688538.CH), using government financing.

South Korea's Private Capital Model vs. China's Direct Government Equity

The South Korean government rarely gives direct subsidies to its large companies for fab expansion or new fab construction, but they do finance up to ~50% of R&D costs associated with the project (75% for smaller entities) and between 30% and 50% of the cost of infrastructure improvements (Water, power, access) through tax benefits, with only a few smaller projects getting direct funding.

China is different. Almost all display projects, expansions or Greenfield, are directly subsidized by the government. In most cases it is the local and provincial governments that partner with the producer to provide financing, along with guaranteeing bank loans. These government entities become shareholding partners with the company in each project, taking stakes typically between 30% and 100% depending on the company, the type of project, and the technology, and in most cases continuing to fund the project after the fab is operational.

This gives a distinct advantage to China’s large panel producers who face far fewer financial constraints when developing project timelines and making equipment purchases, while allowing them to sustain losses for longer periods as the fab becomes established. While some of the Chinese panel producers are public entities and have general public shareholders, they march to the beat of their local or provincial funding partners who control the purse strings, while Korean and Taiwanese producers are far more influenced by their shareholders and traditional profitability measures.

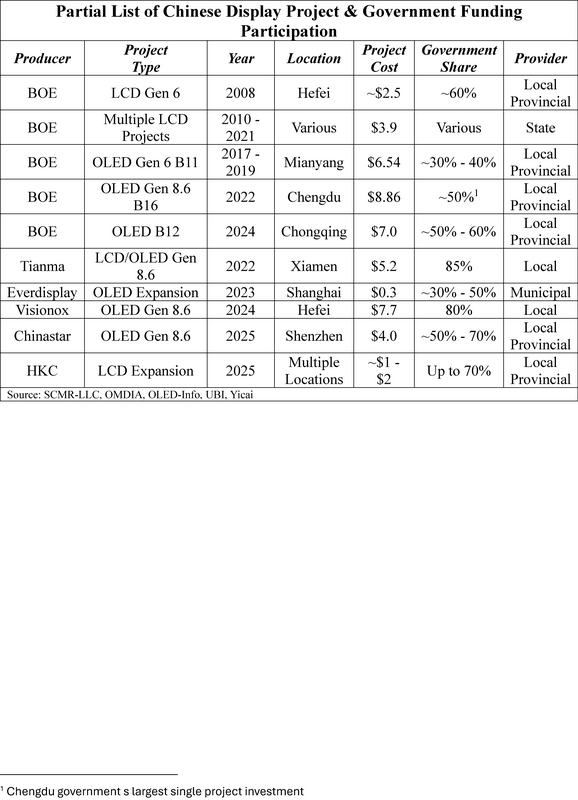

This is particularly important in the latest battle between Korean and Chinese OLED suppliers. Both constituencies are developing Gen 8.6 OLED fabs for the production of IT products and funding for these massive projects is biased toward Chinese producers. While not a new scenario, to understand how pervasive Chinese government display funding is, we list a number of Chinese display projects and the estimated government funding participation percentages

South Korea's Private Capital Model vs. China's Direct Government Equity

The South Korean government rarely gives direct subsidies to its large companies for fab expansion or new fab construction, but they do finance up to ~50% of R&D costs associated with the project (75% for smaller entities) and between 30% and 50% of the cost of infrastructure improvements (Water, power, access) through tax benefits, with only a few smaller projects getting direct funding.

China is different. Almost all display projects, expansions or Greenfield, are directly subsidized by the government. In most cases it is the local and provincial governments that partner with the producer to provide financing, along with guaranteeing bank loans. These government entities become shareholding partners with the company in each project, taking stakes typically between 30% and 100% depending on the company, the type of project, and the technology, and in most cases continuing to fund the project after the fab is operational.

This gives a distinct advantage to China’s large panel producers who face far fewer financial constraints when developing project timelines and making equipment purchases, while allowing them to sustain losses for longer periods as the fab becomes established. While some of the Chinese panel producers are public entities and have general public shareholders, they march to the beat of their local or provincial funding partners who control the purse strings, while Korean and Taiwanese producers are far more influenced by their shareholders and traditional profitability measures.

This is particularly important in the latest battle between Korean and Chinese OLED suppliers. Both constituencies are developing Gen 8.6 OLED fabs for the production of IT products and funding for these massive projects is biased toward Chinese producers. While not a new scenario, to understand how pervasive Chinese government display funding is, we list a number of Chinese display projects and the estimated government funding participation percentages

Case Study: Hefei Government’s $415M Cash Infusion Secures Visionox's ViP Gen 8.6 Fab

But the buck does not stop there. Focusing on the Visionox entry in the table above, it seems that the Hefei government noticed that the company had not been profitable since 2020 and was having some cashflow issues, especially given the large project the company has taken on. The Hefei government decided to make sure that nothing would disturb this very large investment in Visionox’s IT OLED Gen 8.6 fab project. The funding for the Gen 8.6 OLED fab project remained intact, Visionox (the corporate entity) itself was where this were less solid, so the Hefei government stepped in and provided up to $415 million through a private placement (16% below market price), increasing its stake in Visionox from 11.45% to 31.9%. We also note that the Visionox project (Gen 8.6) was originally slated to be both a standard mask-based OLED line and a maskless photolithography based line using Visionox’s proprietary VIP process. Visionox had been leaning toward starting the project with the standard mask line to potentially generate income, but ‘funding sources’ indicated that unless the project began with the new maskless fab, it would not get funded. Needless to say, the plans changed to the VIP fab being the initial project goal.

Conclusion: The State-Backed Display Arms Race

The evidence overwhelmingly demonstrates a profound and strategically critical geographical imbalance in the financing of the global display industry. While South Korean producers like Samsung Display and LG Display rely on internally generated capital, traditional debt financing, and marginal government support for R&D and infrastructure, Chinese panel makers are fueled by direct and substantial government equity participation and subsidies.

This model of State-Backed Capitalism for display manufacturing fundamentally shifts the competitive landscape and has pushed Chinese producers to value visible share over global competitors over profitability. The Chinese system, driven by local and provincial governments taking stakes often ranging from 30% to over 80% in capital-intensive projects (such as the 80% government share in Visionox's Gen 8.6 fab), grants domestic producers a decisive advantage:

But the buck does not stop there. Focusing on the Visionox entry in the table above, it seems that the Hefei government noticed that the company had not been profitable since 2020 and was having some cashflow issues, especially given the large project the company has taken on. The Hefei government decided to make sure that nothing would disturb this very large investment in Visionox’s IT OLED Gen 8.6 fab project. The funding for the Gen 8.6 OLED fab project remained intact, Visionox (the corporate entity) itself was where this were less solid, so the Hefei government stepped in and provided up to $415 million through a private placement (16% below market price), increasing its stake in Visionox from 11.45% to 31.9%. We also note that the Visionox project (Gen 8.6) was originally slated to be both a standard mask-based OLED line and a maskless photolithography based line using Visionox’s proprietary VIP process. Visionox had been leaning toward starting the project with the standard mask line to potentially generate income, but ‘funding sources’ indicated that unless the project began with the new maskless fab, it would not get funded. Needless to say, the plans changed to the VIP fab being the initial project goal.

Conclusion: The State-Backed Display Arms Race

The evidence overwhelmingly demonstrates a profound and strategically critical geographical imbalance in the financing of the global display industry. While South Korean producers like Samsung Display and LG Display rely on internally generated capital, traditional debt financing, and marginal government support for R&D and infrastructure, Chinese panel makers are fueled by direct and substantial government equity participation and subsidies.

This model of State-Backed Capitalism for display manufacturing fundamentally shifts the competitive landscape and has pushed Chinese producers to value visible share over global competitors over profitability. The Chinese system, driven by local and provincial governments taking stakes often ranging from 30% to over 80% in capital-intensive projects (such as the 80% government share in Visionox's Gen 8.6 fab), grants domestic producers a decisive advantage:

- Financial Resilience: They can sustain massive losses for years as they establish new fabs, free from the immediate pressures of private shareholders and traditional profitability metrics that constrain their Korean and Taiwanese rivals.

- Strategic Mandate: The case of Visionox's Gen 8.6 project—where the Hefei government provided a $415 million capital injection to stabilize the parent company and mandated the use of the proprietary, high-risk ViP maskless technology—underscores that these investments are driven by governmental strategic imperative: to secure technological leadership and domestic supply, not just commercial returns.

RSS Feed

RSS Feed