Panel Price Perturbation

Our concern for the CE space has been that tariff issues, particularly in the US, have pushed brands to pull-in production to avoid potential tariff deadlines. This has caused on-shore inventory levels to climb at a time when demand was flat to down slightly. While some of the less onerous CE tariffs have remained, the concern for brands is that another deadline is approaching in July, and it will be difficult to manage additional pull-ins on top of what exists. During the 1st half of the year large panel prices have increased by 1.3% while small panel prices have declined by 2.9% for a total panel price (lg. & Sm.) increase of 1.0%. The breakdown by panel type is included in our monthly panel price table below:

While TV panels have been the weakest category of late, panel producers are struggling to maintain prices in other categories. TV set brands are working against higher basic costs and possible further tariffs and have been pushing for lower panel prices to offset these increases while reducing yearly targets. June saw TV set brand order reductions impact panel prices for the first time since last August, and unless a tariff truce of some sort is called in July, we expect this lower demand level will be maintained until mid-August.

Figure 1 - Aggregate TV Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

Figure 2 - Aggregate NB Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

Figure 3 - Aggregate Monitor Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

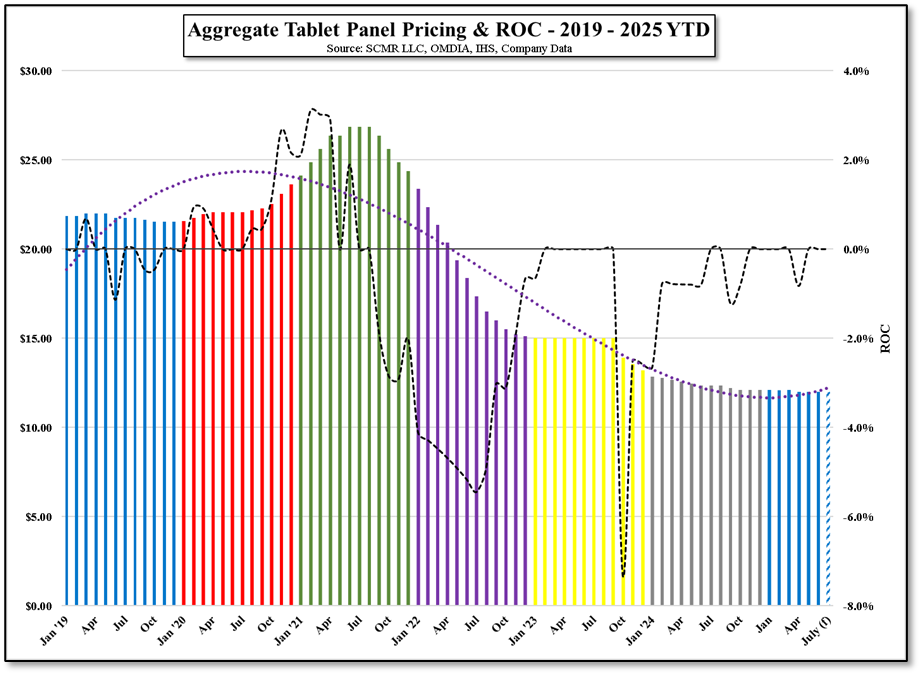

Figure 4 - Aggregate Tablet Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

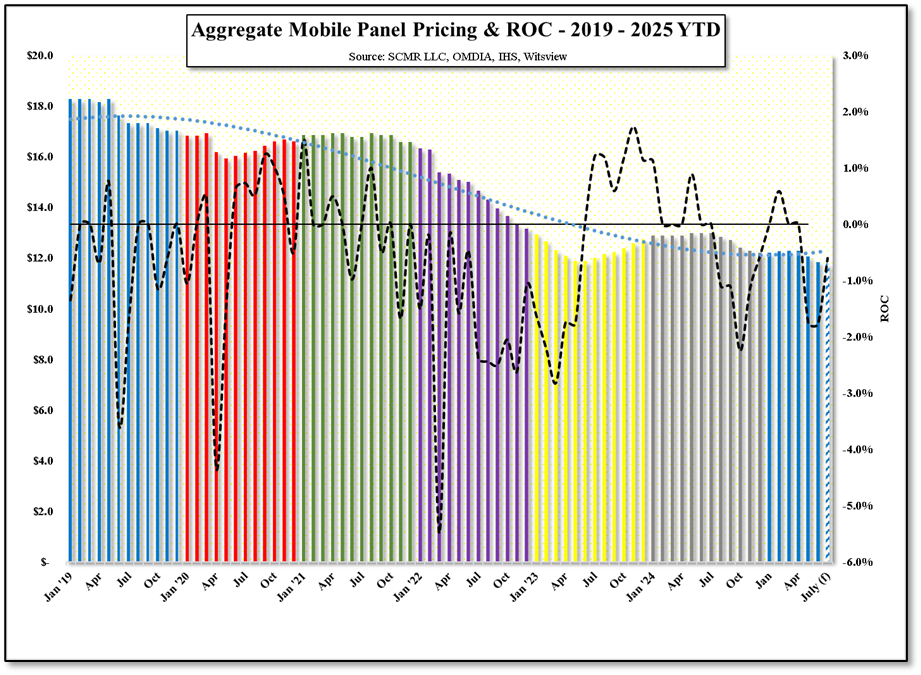

Figure 5 - Aggregate Mobile Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

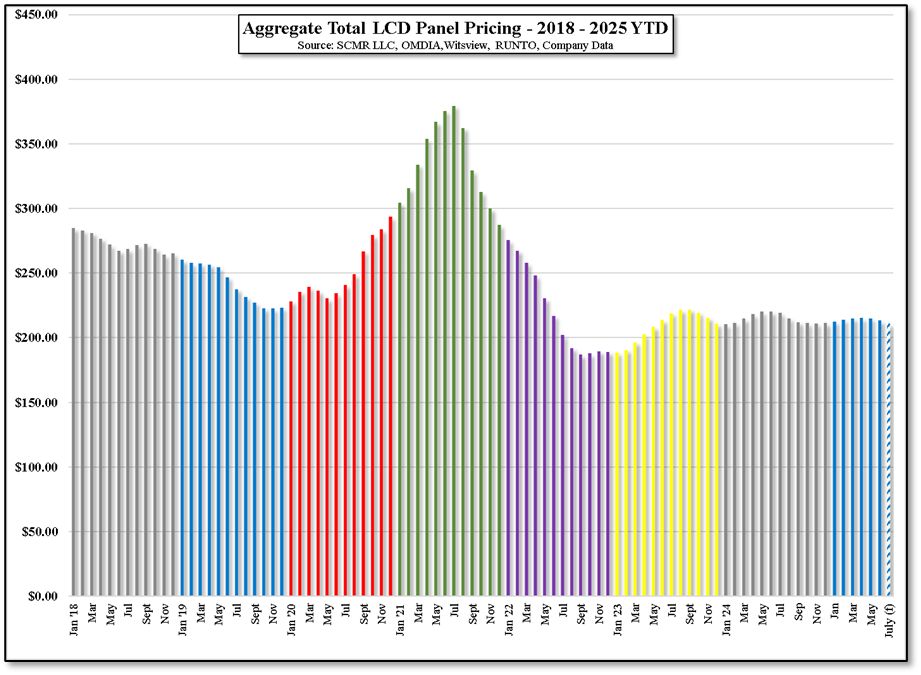

Figure 6 - Aggregate Total LCD Panel Pricing - 2018 - 2025 YTD - Source: SCMR LLC, OMDIA, RUNTO, Company Data

RSS Feed

RSS Feed