Panel Shipments & Sales

Shipments and sales of large panels are a month behind (August) so while we are already looking ahead to October, the shipment and sales data here is from August, a month during which both panel producers and brands were happy campers. August is typically the beginning of the build period for products that will be offered during the 4th quarter holidays, and restocking orders are front and center in the minds of brands. Panel producers typically use August orders to gauge how brands are viewing the 4Q holiday outlook and they seemed pleased with panel orders and the general tone, despite the constant barrage of tariff rhetoric.

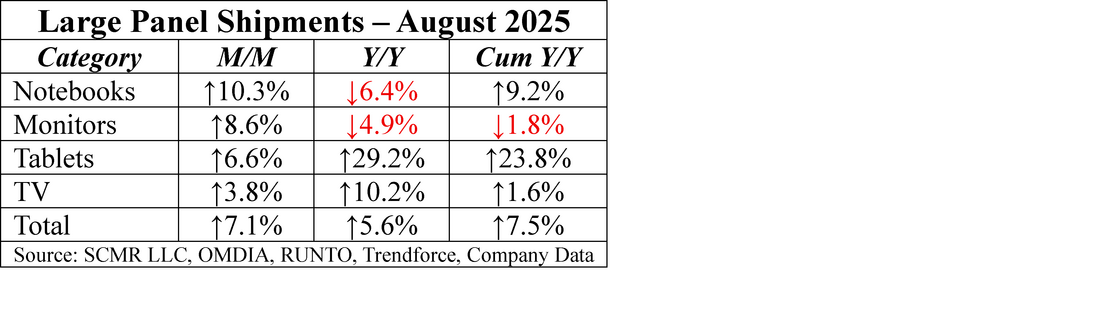

This optimism translated into large panel shipments, increasing 7.1% m/m, 5.6% y/y and up 7.5% on a cumulative basis, with the breakdown by product type shown in the table below.

This optimism translated into large panel shipments, increasing 7.1% m/m, 5.6% y/y and up 7.5% on a cumulative basis, with the breakdown by product type shown in the table below.

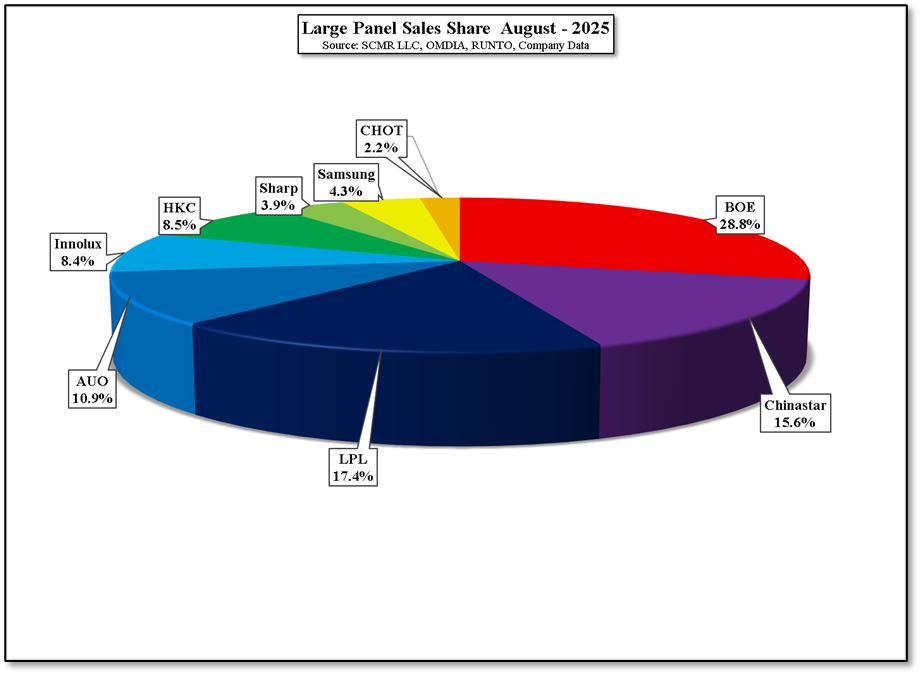

Large panel sales were also strong in August, up 11.6% m/m, 1.9% y/y, but down 1.3% on a cumulative y/y basis. Share for the nine large panel producers are shown in Figure 2. LG Display (LPL) saw the largest m/m gain (46.9%), likely due to the commencement of iPhone panel production after a weak July, but remains down on a cumulative y/y basis due to the sale of its Guangzhou LCD fab to Chinastar (000001.CH), who will likely see that same metric continue to improve for the remainder of the year.

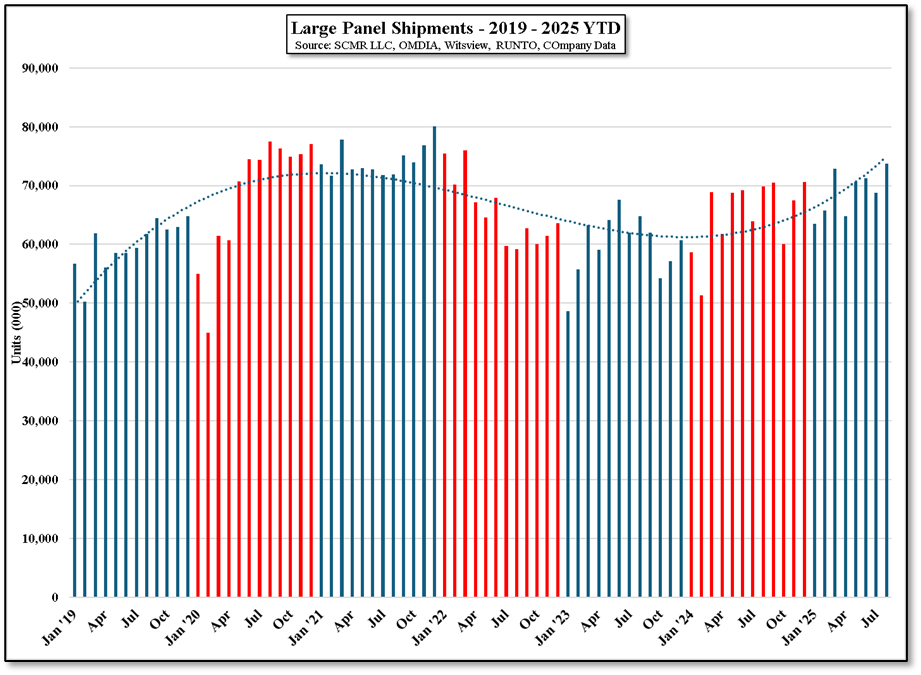

Based on Figure 4, one might get more optimistic about the remainder of the year as the trend line continues to rise, which is exactly what both brands and panel producers did in September, basing that optimism on the potential for tariff settlements and a lessening of trade tension heading into 4Q. As we know that sentiment changed rapidly moving from inventory building at the brand and producer level to utilization cuts and target reductions in September and early October. That optimism was also based on continuing pull-ins from brands who were still trying to avoid new tariffs and not on real consumer demand. In addition China’s consumer subsidy program, which had stimulated demand for much of last year and earlier this year, was beginning to run out of steam (and likely money), so suddenly sentiment went from glass half full to glass half empty.

There is a lot of movement at this time of year in the panel space, and we have seen pretty much every configuration of supply/demand possible play out over the years. This year does seem to be a bit more difficult to figure out given the ‘Big Stick’ trade policy of the current administration and the effect it has on CE companies, but we expect that the holidays might not be as good as thought a few months back but not quite as bad as some expect currently. We see consumers more aggressively looking for high-end products that are discounted and potentially looking to trade down a bit to a mid-range device to offset price increases, as long as AI is on the box. We expect the current administration to report that the holidays were “Fantastic”, “Best ever”, “the result of ‘America First’ tariffs”, regardless of the actual outcome, so we wait a bit to see how October unfolds, while the November onslaught of promotions, discounts, and bundles that we hope will drive CE product consumers through the end of the year. Then there is January…

Based on Figure 4, one might get more optimistic about the remainder of the year as the trend line continues to rise, which is exactly what both brands and panel producers did in September, basing that optimism on the potential for tariff settlements and a lessening of trade tension heading into 4Q. As we know that sentiment changed rapidly moving from inventory building at the brand and producer level to utilization cuts and target reductions in September and early October. That optimism was also based on continuing pull-ins from brands who were still trying to avoid new tariffs and not on real consumer demand. In addition China’s consumer subsidy program, which had stimulated demand for much of last year and earlier this year, was beginning to run out of steam (and likely money), so suddenly sentiment went from glass half full to glass half empty.

There is a lot of movement at this time of year in the panel space, and we have seen pretty much every configuration of supply/demand possible play out over the years. This year does seem to be a bit more difficult to figure out given the ‘Big Stick’ trade policy of the current administration and the effect it has on CE companies, but we expect that the holidays might not be as good as thought a few months back but not quite as bad as some expect currently. We see consumers more aggressively looking for high-end products that are discounted and potentially looking to trade down a bit to a mid-range device to offset price increases, as long as AI is on the box. We expect the current administration to report that the holidays were “Fantastic”, “Best ever”, “the result of ‘America First’ tariffs”, regardless of the actual outcome, so we wait a bit to see how October unfolds, while the November onslaught of promotions, discounts, and bundles that we hope will drive CE product consumers through the end of the year. Then there is January…

Figure 3 - Large Panel Sales Share - August 2025 - by Producer - Source: SCMR LLC, OMDIA, RUNTO, Witsview, Company Data

Figure 4 - Large Panel Shipments - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, RUNTO, Witsview, COmpany Dat

RSS Feed

RSS Feed