Panels in May

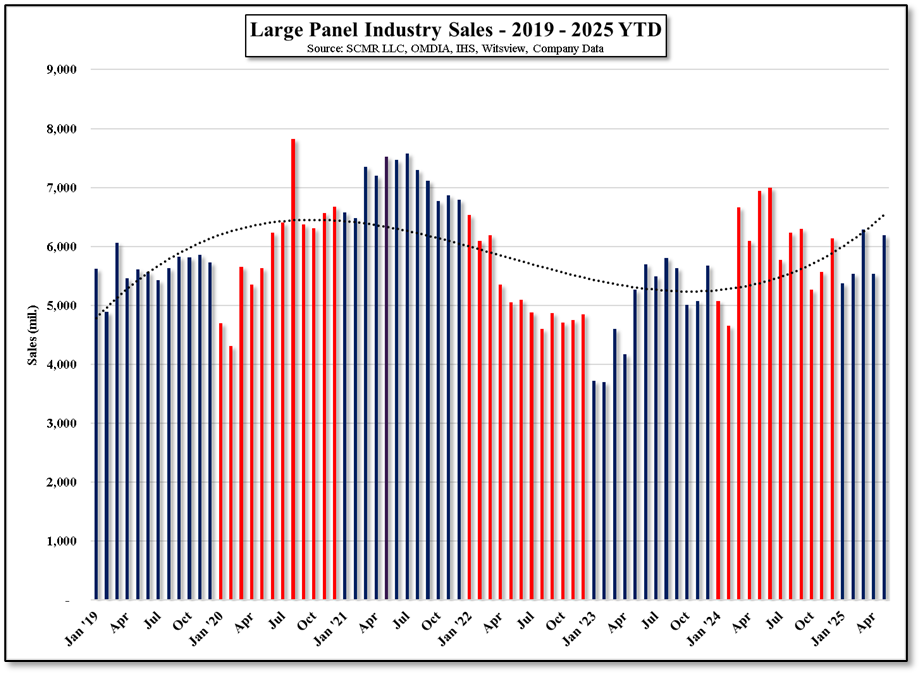

Panel sales this year have been an up and down situation. January and April have been down roughly 12% each m/m, while March and May have been up by roughly the same amounts (February was up slightly). On a cumulative basis against the same period last year, panel sales are down 1.7% and looking at only those that produce large panels, sales are down 2.4% y/y. This comes after a relatively strong May, where sales were up 11.8% m/m but still down 10.7% y/y. 2024 saw most of the strength in panel sales in 2Q and 3Q so this year the industry will face those more difficult comparisons, although the tariff situation has made predictions as to monthly performance almost impossible. That said, we expect June panel sales to be weaker as we expect TV panel prices to decline along with brand demand, and that weakness to carry into August unless some unusual US tariff situation develops when the most recent postponement expires in early July. We estimate that TV panel sales currently make up 50% of total panel sales value, so a downward shift in TV panel pricing and or demand has a significant effect on overall industry panel sales value.

Large Panel Industry Sales - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Witsview, Company Data

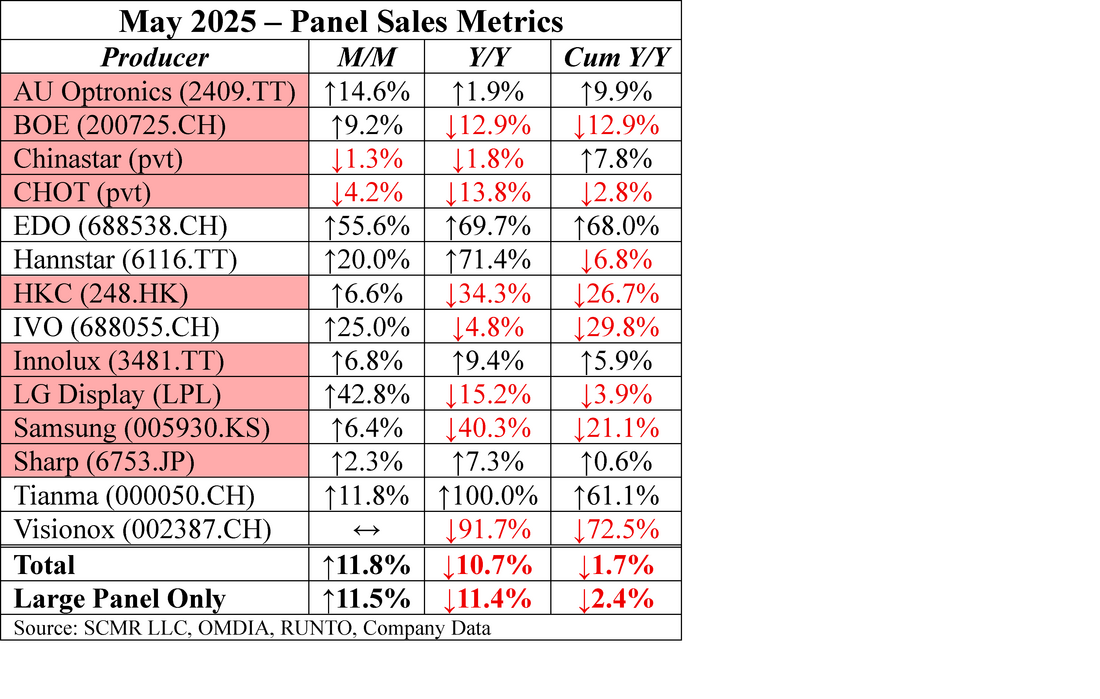

The table below shows the m/m change in panel sales for each supplier for May, the y/y change, and the cumulative y/y change that shows where we stand this year at this point in time, compared to last year. Those highlighted in red are primarily large panel producers.

RSS Feed

RSS Feed