Paying the Piper

Paying the Piper

Smartphone Price Inflation Analysis 2024–2025: Apple iPhone vs. Samsung Galaxy BOM Cost Study

Consumer Electronics Inflation Concerns and US Tariff Impact

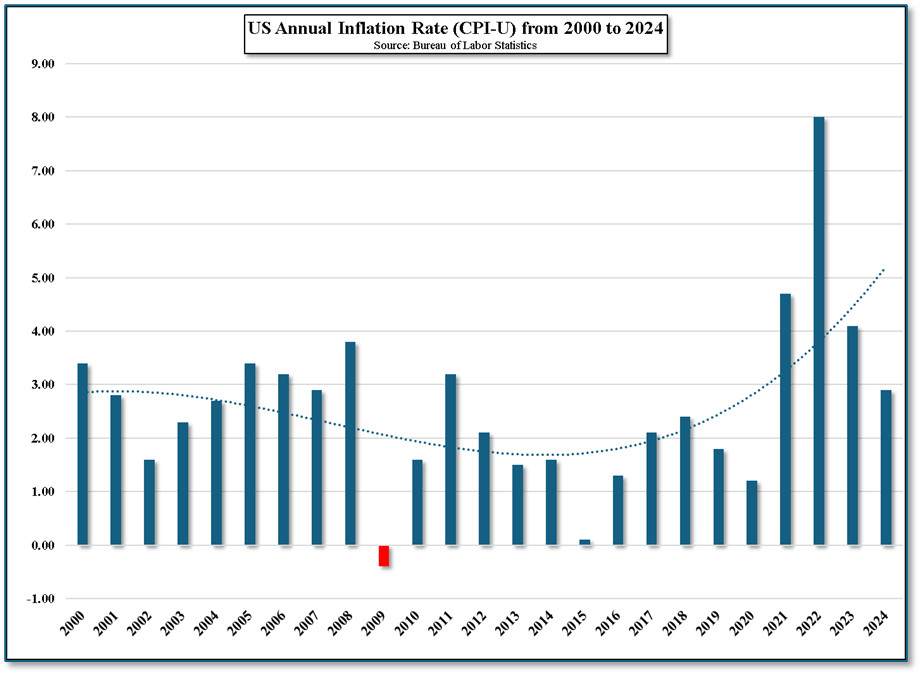

Inflation is a touchy subject when speaking with consumers, who often believe flagship smartphone brands use it to justify price increases. To investigate the true impact of component cost inflation, we analyzed the Bill of Materials (BOM) for the 2025 Apple iPhone 16 Pro Max and the Samsung Galaxy S25 Ultra, two top-tier devices. In a year when the potential exists for US tariffs to add additional costs to many consumer goods, we chose two high profile smartphones to see if we could isolate the effects inflation and component price volatility has had on these phones, particularly the significant NAND Flash and DRAM price increase seen this year.

Smartphone Price Inflation Analysis 2024–2025: Apple iPhone vs. Samsung Galaxy BOM Cost Study

Consumer Electronics Inflation Concerns and US Tariff Impact

Inflation is a touchy subject when speaking with consumers, who often believe flagship smartphone brands use it to justify price increases. To investigate the true impact of component cost inflation, we analyzed the Bill of Materials (BOM) for the 2025 Apple iPhone 16 Pro Max and the Samsung Galaxy S25 Ultra, two top-tier devices. In a year when the potential exists for US tariffs to add additional costs to many consumer goods, we chose two high profile smartphones to see if we could isolate the effects inflation and component price volatility has had on these phones, particularly the significant NAND Flash and DRAM price increase seen this year.

Figure 1 - US Annual Inflation Rate (CPI-U) from 2000 to 2024 - Source: Bureau of Labor Statistics

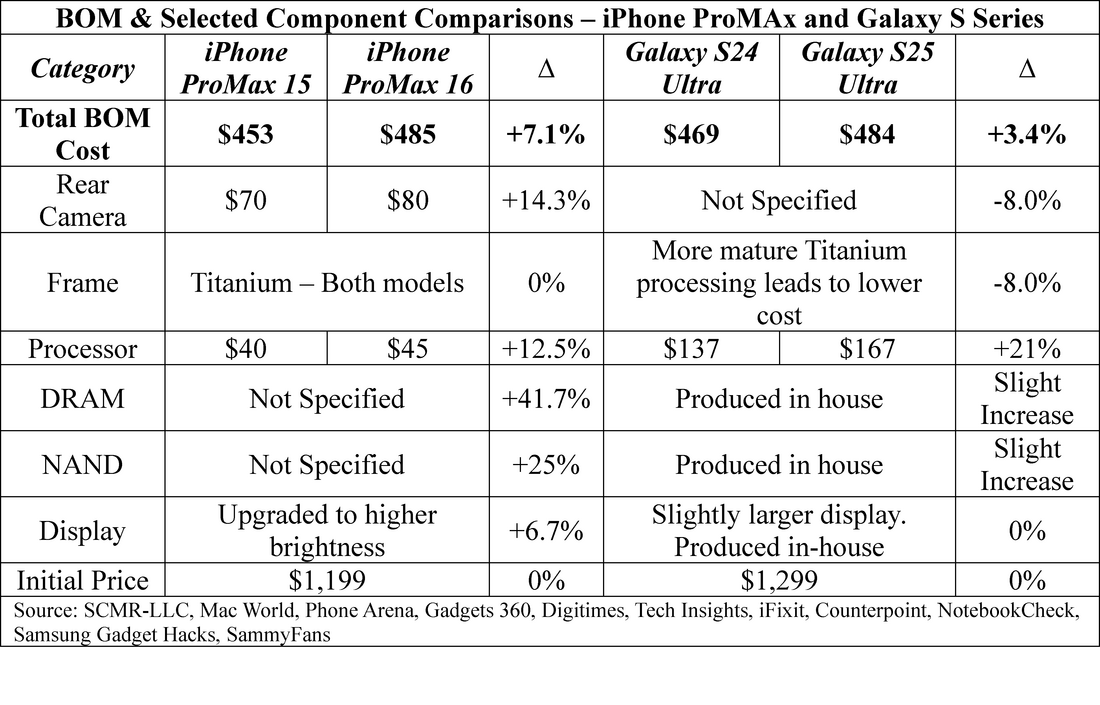

The two phones we chose are Apple’s (AAPL) iPhone Pro Max (Model 15 & 16) and the Samsung (005930.KS) Galaxy Ultra S Series (Model S24 & S25), both representing line top tier of their respective product lines and highly popular across the globe, especially in the US market.

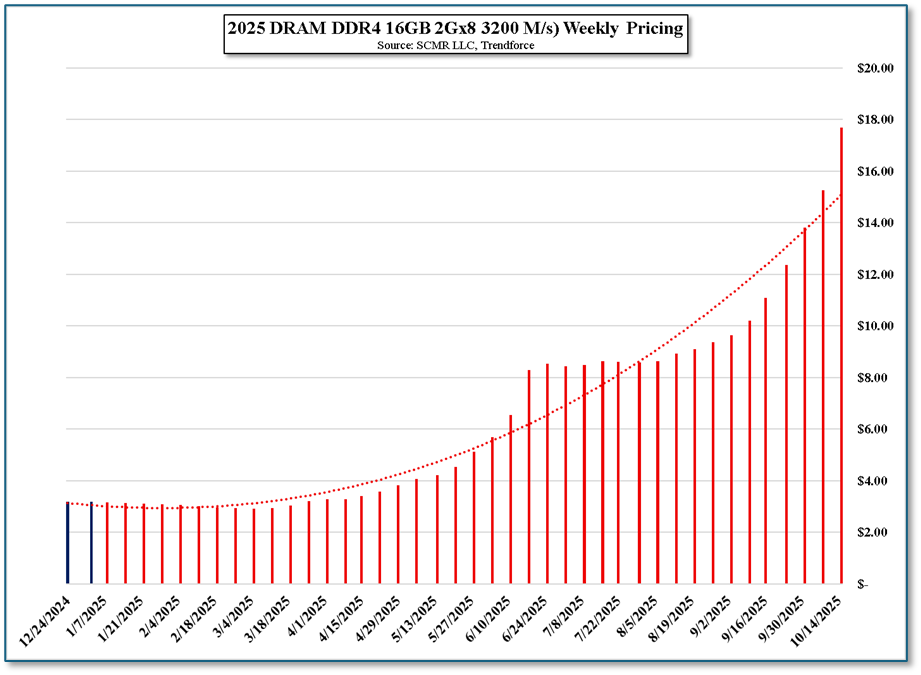

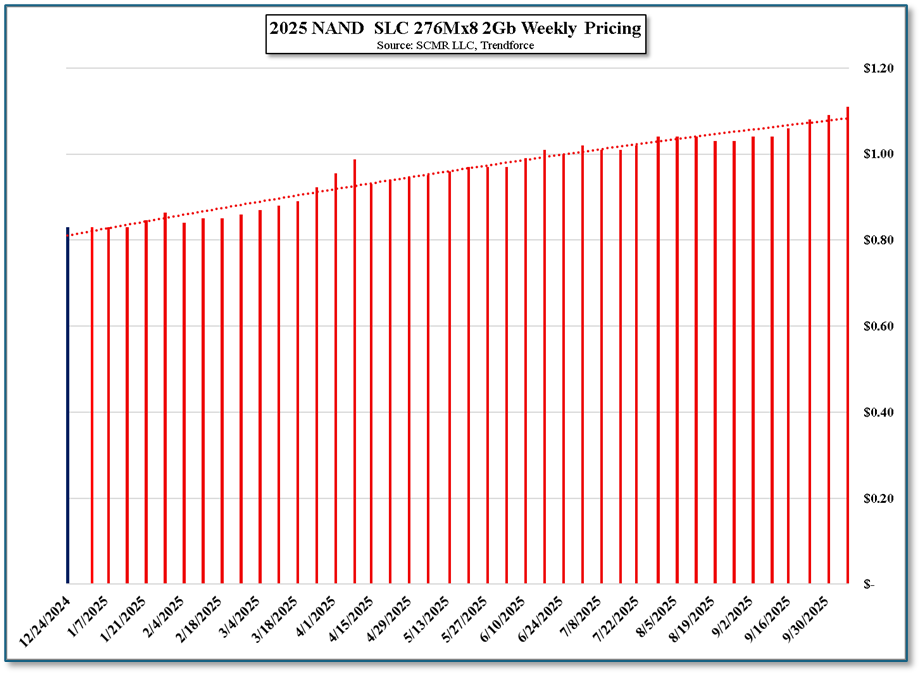

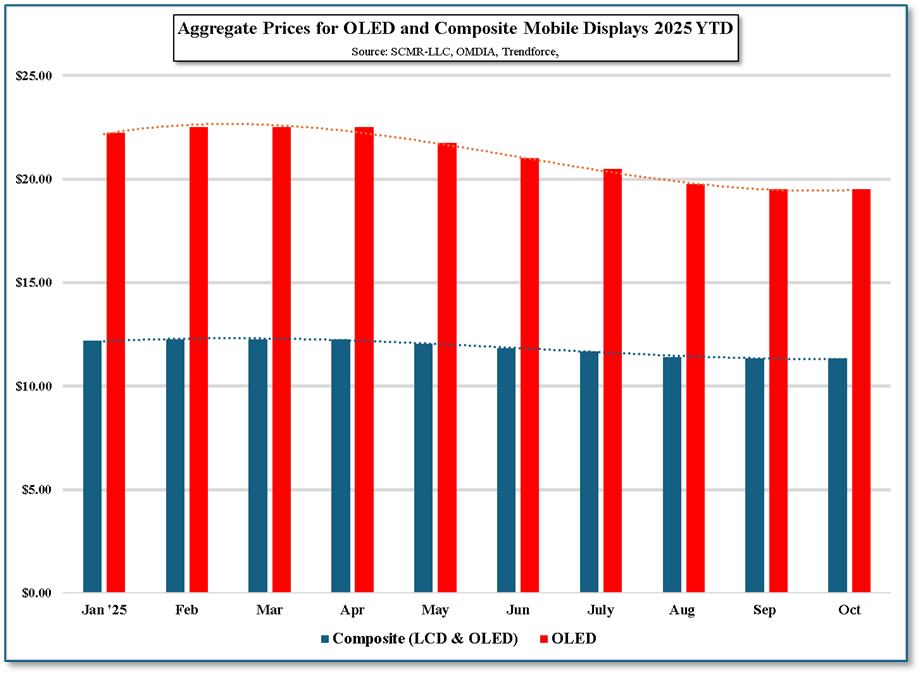

Both iPhone models have a 6.9” LTPO OLED display (brightness improved on the iPhone 17 Pro Max), while the Samsung S24 has a slightly smaller (6.8”) LTPO OLED display as opposed to the 6.9” LTPO OLED display of the S25 Ultra, and while it is difficult to track the absolute pricing of these specific displays, we can track the aggregate price of OLED displays in that category, as shown in Figure 4. We note that the price of the OLED displays indicated in the chart declined by 18.8% YTD. Memory prices (DDR4) have moved in the opposite direction, increasing between 188.0% and 454.2% depending on the type used. We estimate that the average smartphone uses between 8GB and 12 GB internal RAM (DRAM) and between 256GB and 1 TB of NAND Flash storage, with NAND increasing in price between 38.6% and 61.3% YTD.

These are just two of the many components in these particular smartphones, so we focus on total BOM for each as a way to understand how inflation has changed the smartphone flagship margin picture this year. We note that in the BOM comparisons there are a number of components that have been upgraded which, in some cases, means an increase in price related to the feature set and not the cost of a comparable component. The example would be Samsung’s upgrade of the Qualcomm (QCOM) Snapdragon 8 Gen 4 SoC to the Snapdragon 8 Gen 4 Elite SoC which pushes that component’s cost up by ~21%.

Both iPhone models have a 6.9” LTPO OLED display (brightness improved on the iPhone 17 Pro Max), while the Samsung S24 has a slightly smaller (6.8”) LTPO OLED display as opposed to the 6.9” LTPO OLED display of the S25 Ultra, and while it is difficult to track the absolute pricing of these specific displays, we can track the aggregate price of OLED displays in that category, as shown in Figure 4. We note that the price of the OLED displays indicated in the chart declined by 18.8% YTD. Memory prices (DDR4) have moved in the opposite direction, increasing between 188.0% and 454.2% depending on the type used. We estimate that the average smartphone uses between 8GB and 12 GB internal RAM (DRAM) and between 256GB and 1 TB of NAND Flash storage, with NAND increasing in price between 38.6% and 61.3% YTD.

These are just two of the many components in these particular smartphones, so we focus on total BOM for each as a way to understand how inflation has changed the smartphone flagship margin picture this year. We note that in the BOM comparisons there are a number of components that have been upgraded which, in some cases, means an increase in price related to the feature set and not the cost of a comparable component. The example would be Samsung’s upgrade of the Qualcomm (QCOM) Snapdragon 8 Gen 4 SoC to the Snapdragon 8 Gen 4 Elite SoC which pushes that component’s cost up by ~21%.

Figure 2 - 2025 DRAM (DDR4 16GB 2Gx8 3200 M.s) Weekly Pricing - Source: SCMR-LLC, Trendforce

Figure 3 - 2025 NAND SLC 276Mx8 2GB Weekly Pricing - Source: SCMR LLC, Trendforce

Figure 4 - Aggregate Prices for OLED & Composite Mobile Displays - 2025 YTD - Source: SCMR-LLC, OMDIA, Trendforce

Full component BOMs are hard to come by as they tend to be proprietary, but we can look at the composite BOMs totals and selected components. We note that the detail on the BOMs are not always the same so we use the delta of the change when necessary

Manufacturer Margin Absorption and US Carrier Pricing Dynamics

Based on the increases seen in Apple’s 2025 BOM, we estimate that margins on the Pro Max declined by between 2.0% and 2.5% and given that the selling price remained the same, Apple absorbed the reduction. Samsung was less transparent but with a BOM increase of less than half that of Apple, we expect that translated to a 1% margin reduction, which Samsung also absorbed, but the trail does not end there.

Apple sells ~37% of iPhones directly to consumers through Apple stores and Apple.com with the remainder through indirect channels like 3rd party retailers, carriers, and distributors (In the US ~75% of sales go through carriers). When they sell direct, the margin is ~60% (excludes cost of maintaining stores and on-line presence). We estimate that when Apple sells to distributors the margin is ~54%, with the distributors marking up by ~5% when they sell to retailers. Carriers and retailers mark up another 10% to 12% to reach the $1,199 price, although because of the high volumes associated with flagship products, carriers and retailers are often willing to take lower markups. Samsung’s system is similar although they rely more heavily on carriers for distribution globally.

Typically Apple sets a wholesale and retail price for each model which locks in distributor and retail margins. Apple does not allow partners to change their ‘buy’ price, so BOM increases without a corresponding price (MSRP) increase leave Apple to absorb the increase, especially as agreements on buy-in prices with partners are made in advance of the product launch. There are no mechanisms for changing those prices for BOM or specific component price increases, but Apple can indicate far in advance that the buy-in or MSRPO price for the next generation iPhone will increase. Apple does occasionally offer channel partners incentives to stimulate sales in the form of marketing support and specific product promotions, but those costs come out of Apple’s margin, as Apple is known to protect partners with very stable pricing regardless of the circumstances.

Samsung also sets buy-in and MSRP, especially for South Korea and the US but is a bit more flexible in other countries, especially around mid-cycle. Samsung is a bit more aggressive when it comes to promotions for resellers and makes adjustments to promotion levels, marketing rebates, and buy-back incentives to balance increases in BOM. However they never directly shift manufacturing cost increases to partners.

Conclusion: BOM Inflation Adds Complexity to Smartphone Design

Ultimately BOM cost inflation is absorbed by smartphone manufacturers throughout much, if not all, of the product’s first year selling cycle, particularly in the US where carriers and retailers want to make sure they have a steady margin. This makes pre-assembly component cost negotiations even more critical, especially when competitive pressures leave little room for price increases. As tariffs and component price increases filter through BOM at almost every level maintaining steady margins at the manufacturing level is not an easy task and what might seem like modest cost increases for components, transportation, or tariffs are magnified at the manufacturing level , where there is little opportunity to adjust prices once they are set for a particular product cycle. This adds to the complexity of feature decisions during periods of high inflation, and we believe in recent years it has led to a lack of new hardware features in flagship phones.

Based on the increases seen in Apple’s 2025 BOM, we estimate that margins on the Pro Max declined by between 2.0% and 2.5% and given that the selling price remained the same, Apple absorbed the reduction. Samsung was less transparent but with a BOM increase of less than half that of Apple, we expect that translated to a 1% margin reduction, which Samsung also absorbed, but the trail does not end there.

Apple sells ~37% of iPhones directly to consumers through Apple stores and Apple.com with the remainder through indirect channels like 3rd party retailers, carriers, and distributors (In the US ~75% of sales go through carriers). When they sell direct, the margin is ~60% (excludes cost of maintaining stores and on-line presence). We estimate that when Apple sells to distributors the margin is ~54%, with the distributors marking up by ~5% when they sell to retailers. Carriers and retailers mark up another 10% to 12% to reach the $1,199 price, although because of the high volumes associated with flagship products, carriers and retailers are often willing to take lower markups. Samsung’s system is similar although they rely more heavily on carriers for distribution globally.

Typically Apple sets a wholesale and retail price for each model which locks in distributor and retail margins. Apple does not allow partners to change their ‘buy’ price, so BOM increases without a corresponding price (MSRP) increase leave Apple to absorb the increase, especially as agreements on buy-in prices with partners are made in advance of the product launch. There are no mechanisms for changing those prices for BOM or specific component price increases, but Apple can indicate far in advance that the buy-in or MSRPO price for the next generation iPhone will increase. Apple does occasionally offer channel partners incentives to stimulate sales in the form of marketing support and specific product promotions, but those costs come out of Apple’s margin, as Apple is known to protect partners with very stable pricing regardless of the circumstances.

Samsung also sets buy-in and MSRP, especially for South Korea and the US but is a bit more flexible in other countries, especially around mid-cycle. Samsung is a bit more aggressive when it comes to promotions for resellers and makes adjustments to promotion levels, marketing rebates, and buy-back incentives to balance increases in BOM. However they never directly shift manufacturing cost increases to partners.

Conclusion: BOM Inflation Adds Complexity to Smartphone Design

Ultimately BOM cost inflation is absorbed by smartphone manufacturers throughout much, if not all, of the product’s first year selling cycle, particularly in the US where carriers and retailers want to make sure they have a steady margin. This makes pre-assembly component cost negotiations even more critical, especially when competitive pressures leave little room for price increases. As tariffs and component price increases filter through BOM at almost every level maintaining steady margins at the manufacturing level is not an easy task and what might seem like modest cost increases for components, transportation, or tariffs are magnified at the manufacturing level , where there is little opportunity to adjust prices once they are set for a particular product cycle. This adds to the complexity of feature decisions during periods of high inflation, and we believe in recent years it has led to a lack of new hardware features in flagship phones.

RSS Feed

RSS Feed