Slippin’ & Slidin’

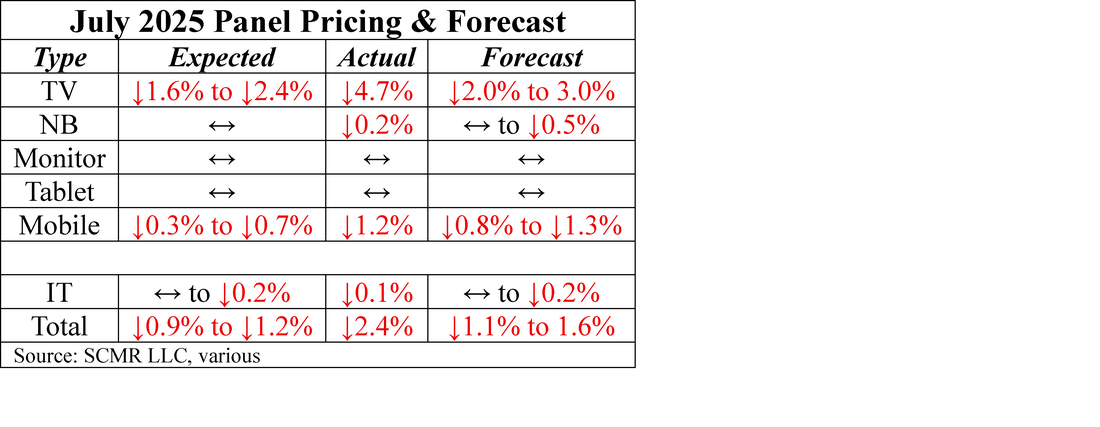

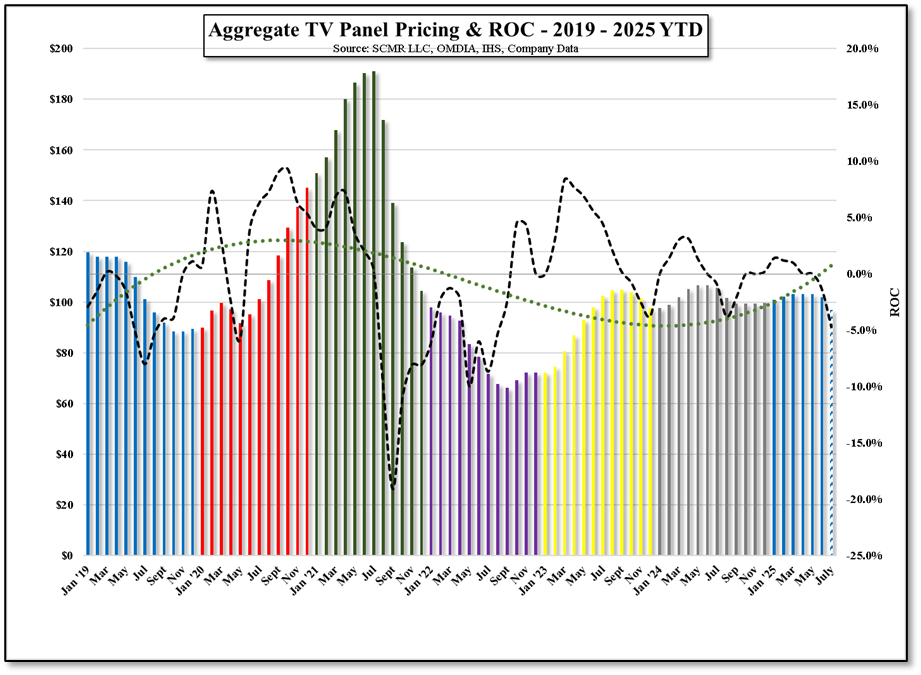

Panel pricing has yet to show the disparity between what panel producers are still hoping for in 3Q (demand improvement) and 4Q and what brands are beginning to expect (weaker than expected demand). There has been no high-level panic in the industry relative to panel prices and at least on the IT side, prices have remained relatively stable, but cracks in the armor are beginning to show in the TV panel space, where prices continue to weaken, putting pressure on the display space and potential profitability for 2H for both panel producers and CE brands. In particular, July TV panel pricing was a bit worse than we had expected, down 4.7% against our ↓2.0% SPA, although we expect a bit less pressure in August. That said, TV panel prices (average) are at their lowest point in the last 24 months.

The general tone seems to have shifted a bit over the last 60 days from one of the glass still being half full to one of hoping that the water is not evaporating more quickly than expected. Outside of tariff pull-ins that are cannibalizing 3Q demand, overall demand remains weak for monitor panels, TV panels, and mobile panels. China subsidies are still stimulating demand for tablets and both subsidies and AI are still helping notebook demand, although memory and CPU price increases could begin to reflect higher prices. The effects of landed CE inventory on the holiday season remain unquantified, but the general economic climate does not seem to be setting up a strong holiday demand cycle. There is still time for that to settle out in a better light but with the most recent tariff deadline approaching, we expect brands will remain cautious until there is some clarity and a bit more stability..

The general tone seems to have shifted a bit over the last 60 days from one of the glass still being half full to one of hoping that the water is not evaporating more quickly than expected. Outside of tariff pull-ins that are cannibalizing 3Q demand, overall demand remains weak for monitor panels, TV panels, and mobile panels. China subsidies are still stimulating demand for tablets and both subsidies and AI are still helping notebook demand, although memory and CPU price increases could begin to reflect higher prices. The effects of landed CE inventory on the holiday season remain unquantified, but the general economic climate does not seem to be setting up a strong holiday demand cycle. There is still time for that to settle out in a better light but with the most recent tariff deadline approaching, we expect brands will remain cautious until there is some clarity and a bit more stability..

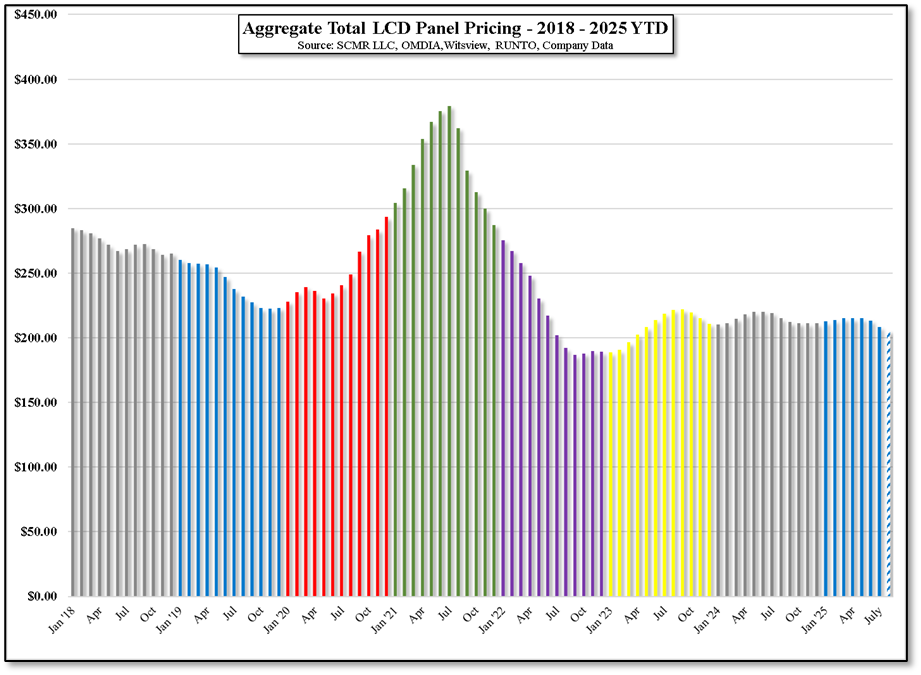

Figure 3 - Aggregate Total LCD Panel Pricing - 2018 - 2025 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO, Company Data

Figure 4 - Aggregate TV Panel Pricing & ROC - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, IHS, Company Data

RSS Feed

RSS Feed