The Conflict – January 2026 LCD Panel Pricing Analysi

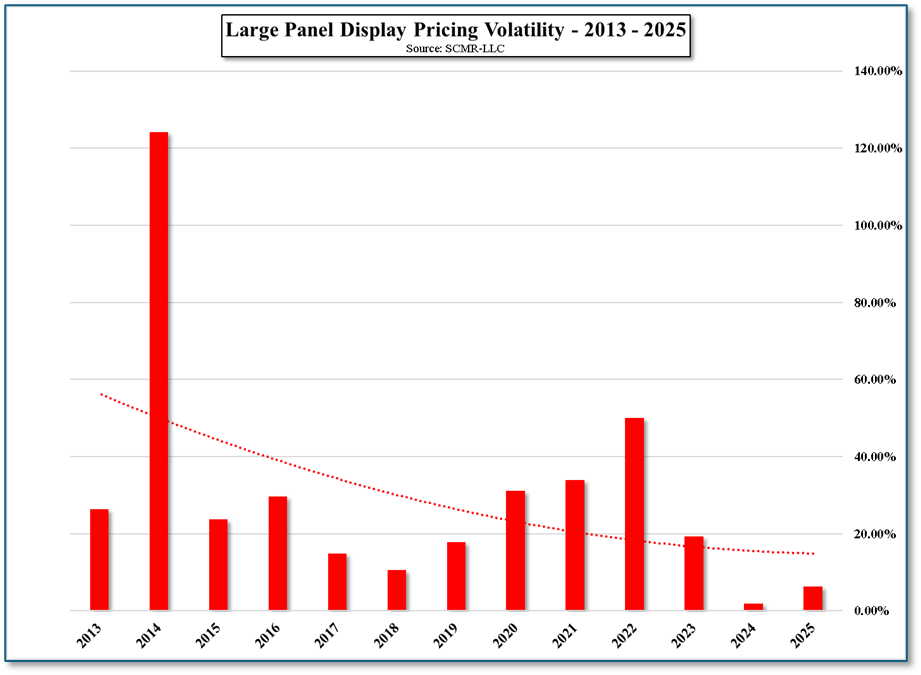

Display panel pricing is a pure supply/demand balance between panel buyers, typically CE brands and OEMs, and panel manufacturers who have spent billions building fabs that produce hundreds of thousands of display panels each month. The display industry has been known for its cycles where prices rise and fall over what is typically a three year period, but as the LCD display industry matures, much of that volatility is being wrung out of the system. The data in the table confirms this shift toward stability, driven primarily by a strategic pivot among Chinese panel producers who now prioritize profitability over aggressive market-share acquisition.

Strategic Utilization Management

We believe the transformation is based on a focus change, primarily from Chinese panel producers, who have come to realize that, despite government subsidies, share is less of a factor than it was in the early days of panel production. In the LCD space China is the dominant producer of large panel displays, and has essentially won the battle for share dominance, but Chinese LCD producers have found funding to be harder to come by in recent years as OLED and now Ai compete for government dollars. This has increased their focus on profitability and has made them more sensitive to pricing extremes.

As we have noted previously, Chinese producers are using utilization management to better balance supply and demand in recent years, which is a short-term solution to imbalances that is easier to recover from than price declines. This has lowered the volatility on a yearly basis and dampened the large pricing swings seen years ago. That said, LCD large panel pricing is both mercurial and nuanced, with the play between brands and producers a monthly negotiation, with different parameters for each display type and technology variation.

December Panel Market Performance

In December 2025 large display pricing saw monitor panel pricing remained flat, as expected, while notebook panel pricing declined by 0.4%, within our expectations of down 0.6% to down 0.4%. TV panels were the exception in December, declining only 0.2% for the month, the low end of our down 0.5% to down 0.2% expectations. This follows declines of over 2.0% for TV panels in the two previous months.

Panel producers lowered utilization in November to reduce supply and that seems to have helped to better balance the TV panel space. However, panel producers are also looking to recover some of the pricing ground they lost in 2025 and are looking to raise prices this month. TV set brands did not see strength during both the 11/11 holiday in China or Black Friday on a more global basis, leaving inventory at higher than expected levels. While we believe brands will make some concessions on TV panel price, we expect they will be short-lived as brands face higher memory costs and new tariffs (see below).

Panel Price Changes for 2025:

The Outlook for Chinese TV brands

Chinese TV set brands are in a more sensitive position at this juncture as they face competition in the US from mainstream brands that do not have as large a tariff burden as Chinese brands, as the new year changed the tariff picture on TV sets once again. In January 2026, the trade landscape for television sets is redefined by a "tariff wall" between China and Mexico. While the US and China have recently reached trade arrangements to de-escalate, the total duties on Chinese electronics remain significantly higher than those on Mexican goods. With Samsung Electronics (005930.KS) and LG Electronics (066570.KS) assembling TV sets primarily in Mexico, even with Chinese government subsidies, non-Chinese TV set brands have some pricing leverage over Chinese brands, who are typically the most aggressive toward set pricing in the US.

TVs Produced in Mexico (The "Zero-Tariff" Advantage)

Televisions produced in Mexico currently enter the US at a 0% tariff rate under the United States-Mexico-Canada Agreement (USMCA), but specific rules for TVs in 2026 make it even more complicated..

Televisions shipped directly from China face a heavy cumulative burden. While the general (MFN) rate for TVs is technically 3.9%, additional trade actions have layered on top of this:

Conclusion: A New Era of Managed Stability

The LCD industry has transitioned from a period of extreme, "cycle-driven" volatility into a mature phase characterized by a more disciplined supply management. The era of 100%+ price swings (as seen in 2014) has been replaced by single-digit annual variances (6.36% in 2025), signaling that Chinese panel producers have successfully shifted their priority from aggressive market-share acquisition to sustained profitability.

Strategic Utilization Management

We believe the transformation is based on a focus change, primarily from Chinese panel producers, who have come to realize that, despite government subsidies, share is less of a factor than it was in the early days of panel production. In the LCD space China is the dominant producer of large panel displays, and has essentially won the battle for share dominance, but Chinese LCD producers have found funding to be harder to come by in recent years as OLED and now Ai compete for government dollars. This has increased their focus on profitability and has made them more sensitive to pricing extremes.

As we have noted previously, Chinese producers are using utilization management to better balance supply and demand in recent years, which is a short-term solution to imbalances that is easier to recover from than price declines. This has lowered the volatility on a yearly basis and dampened the large pricing swings seen years ago. That said, LCD large panel pricing is both mercurial and nuanced, with the play between brands and producers a monthly negotiation, with different parameters for each display type and technology variation.

December Panel Market Performance

In December 2025 large display pricing saw monitor panel pricing remained flat, as expected, while notebook panel pricing declined by 0.4%, within our expectations of down 0.6% to down 0.4%. TV panels were the exception in December, declining only 0.2% for the month, the low end of our down 0.5% to down 0.2% expectations. This follows declines of over 2.0% for TV panels in the two previous months.

Panel producers lowered utilization in November to reduce supply and that seems to have helped to better balance the TV panel space. However, panel producers are also looking to recover some of the pricing ground they lost in 2025 and are looking to raise prices this month. TV set brands did not see strength during both the 11/11 holiday in China or Black Friday on a more global basis, leaving inventory at higher than expected levels. While we believe brands will make some concessions on TV panel price, we expect they will be short-lived as brands face higher memory costs and new tariffs (see below).

Panel Price Changes for 2025:

- TV Panels – down 7.6%

- Notebook Panels – down 2.2%

- Monitor Panels – up 1.2%

- Large Panel Total – Down 4.1%

The Outlook for Chinese TV brands

Chinese TV set brands are in a more sensitive position at this juncture as they face competition in the US from mainstream brands that do not have as large a tariff burden as Chinese brands, as the new year changed the tariff picture on TV sets once again. In January 2026, the trade landscape for television sets is redefined by a "tariff wall" between China and Mexico. While the US and China have recently reached trade arrangements to de-escalate, the total duties on Chinese electronics remain significantly higher than those on Mexican goods. With Samsung Electronics (005930.KS) and LG Electronics (066570.KS) assembling TV sets primarily in Mexico, even with Chinese government subsidies, non-Chinese TV set brands have some pricing leverage over Chinese brands, who are typically the most aggressive toward set pricing in the US.

TVs Produced in Mexico (The "Zero-Tariff" Advantage)

Televisions produced in Mexico currently enter the US at a 0% tariff rate under the United States-Mexico-Canada Agreement (USMCA), but specific rules for TVs in 2026 make it even more complicated..

- Compliance Requirement: To qualify for the 0% rate, the TV must be a "compliant good," meaning it meets specific Rules of Origin, meaning roughly 50% to 60% of the value of the components must be added in Mexico, Canada, or the US.

- Rules of Origin: For TVs, this usually requires that key sub-assemblies (like the screen or motherboard) be produced or undergo significant transformation within North America. For example, If Samsung imports raw components (like a display panel from Korea) under one HTS code and produces a finished TV in Mexico under a completely different HTS code, this "shift" can count as origin, but Samsung must also prove that a specific percentage of the TV's value was created in North America, meaning using parts that were created here. As of January 1, 2026, Mexico has implemented its own tariffs of up to 35% - 50% on Chinese components to prevent China from using Mexico as a "pass-through" to avoid US tariffs.

Televisions shipped directly from China face a heavy cumulative burden. While the general (MFN) rate for TVs is technically 3.9%, additional trade actions have layered on top of this:

- Reciprocal Tariffs: Under executive orders issued in 2025, China faces a cumulative tariff rate estimated at 65.4% for certain electronics to "rebalance" trade deficits.

- Section 301: Even after recent deals to avoid further escalation, many Chinese goods remain subject to an aggregate 45% rate from the ongoing trade disputes.

- De Minimis Removal: Previously, small orders under $800 could enter the US duty-free. As of late 2025, this exemption has been eliminated for China, meaning even individual TV shipments are now taxed.

Conclusion: A New Era of Managed Stability

The LCD industry has transitioned from a period of extreme, "cycle-driven" volatility into a mature phase characterized by a more disciplined supply management. The era of 100%+ price swings (as seen in 2014) has been replaced by single-digit annual variances (6.36% in 2025), signaling that Chinese panel producers have successfully shifted their priority from aggressive market-share acquisition to sustained profitability.

- The Shift to "Utilization Management" - The dominant Chinese producers have moved away from "price wars" and toward utilization management. By proactively throttling supply in response to demand dips, rather than slashing prices to keep fabs running at 100%, producers have successfully dampened the "mercurial" price swings of the past. This strategy effectively stabilized TV panel prices in December 2025, even in the face of disappointing holiday sales.

- The Geo-Political "Tariff Wall" - The 2026 trade landscape creates a stark divergence in market competitiveness. The "Mexico Advantage" provides a critical lifeline for brands like Samsung and LG, allowing them to bypass the ~65% tariff burden faced by direct-from-China shipments. However, the recent 2026 crackdown on "pass-through" components in Mexico means that even these brands must now localize high-value manufacturing (like motherboards and logic) to maintain their 0% duty status.

- The Outlook for 2026 - Heading into the new year, the power dynamic is shifting:

- For Panel Producers: While they ended 2025 with large panel pricing down 4.1% overall, their ability to raise prices in January is capped by high brand inventory levels and rising memory costs.

- For Chinese TV Brands: Facing a massive tariff disadvantage and drying government subsidies, these brands must decide if they can afford to remain aggressive in the US market.

- For the Industry: If Chinese set brands pull back from the US to avoid the tariff wall, the resulting volume drop will make it significantly harder for panel manufacturers to regain the pricing ground they lost in 2025.

Figure 1 - Large Panel Display Pricing Volatility - 2013 - 2025 - Source: SCMR LLC

RSS Feed

RSS Feed