Universal Display – 2Q – Disappointing But Not Unexpected

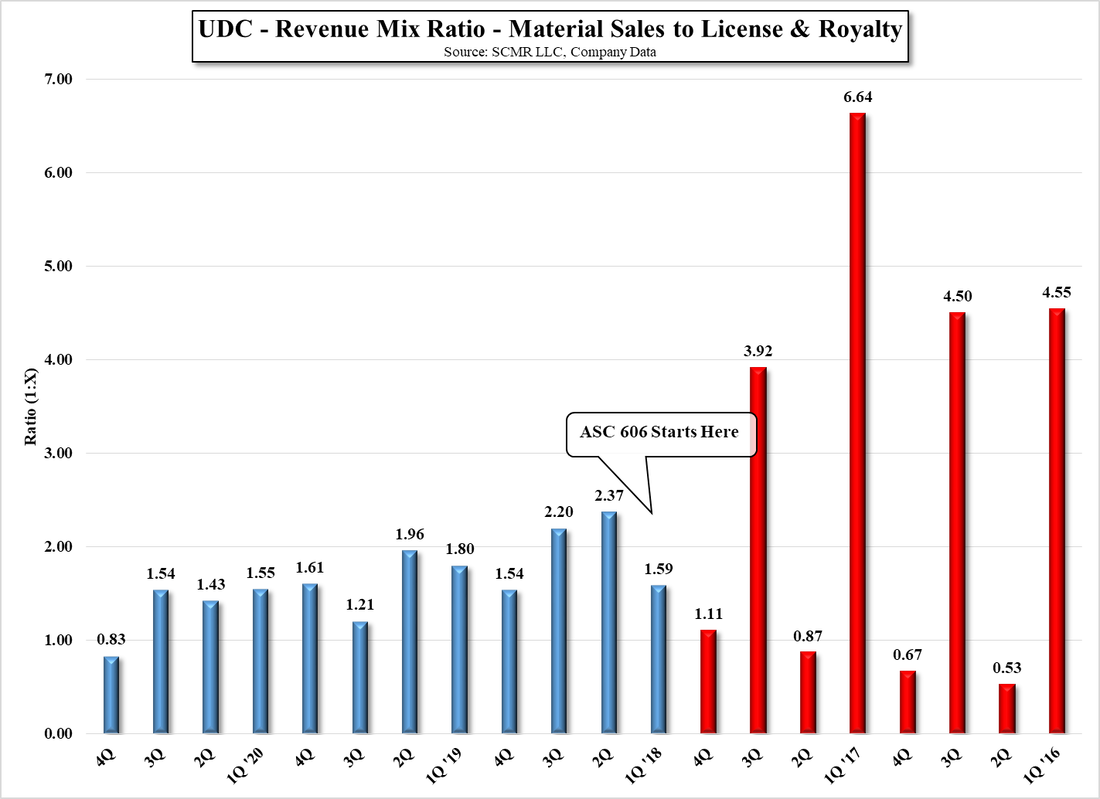

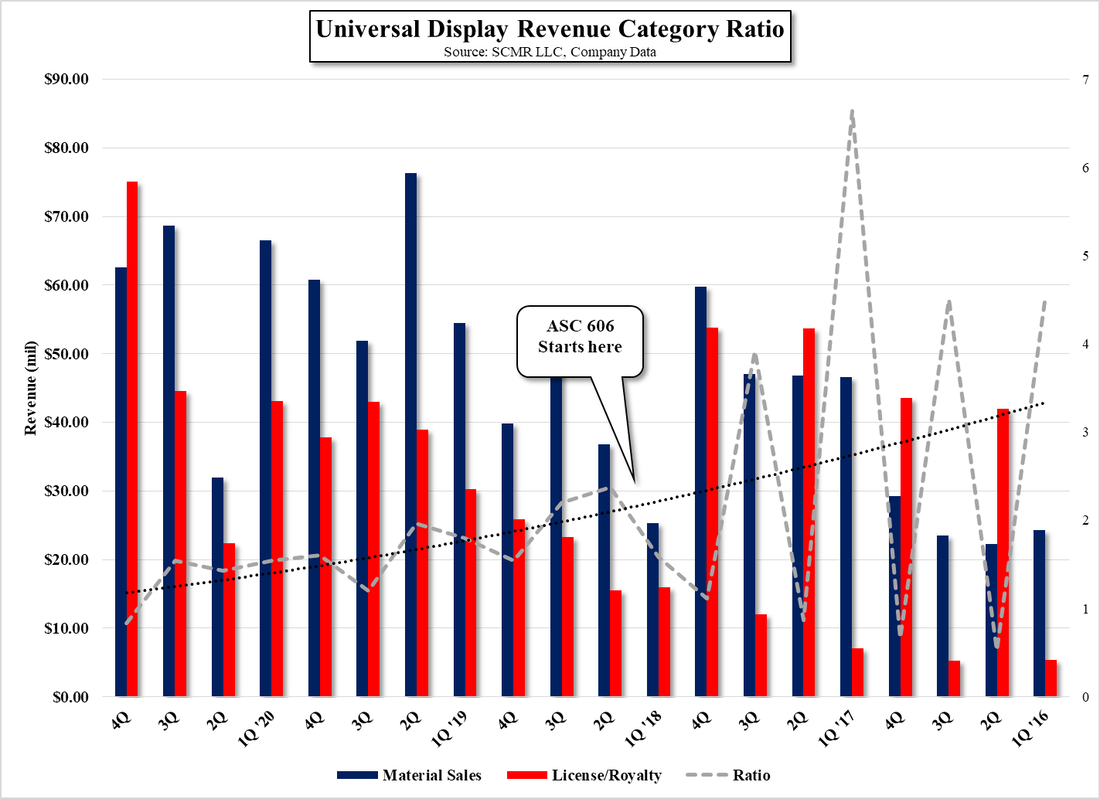

Universal Display (OLED) reported 2Q revenue results ($136.6m) that were down 9.2% q/q but up 5.3% y/y and short of consensus of between $149.6m and $151.2m, with OLED material sales of $71.9m, down 17.1% q/q and down 7.2% y/y, while royalty &^ license revenue ($60.3m) increased slightly (0.8%) q/q and was up 25.0% y/y. OLED material margin declined slightly to 65.2% while overall margin increased from 78.0% to 80.1%. UDC lowered their full year guidance from a range of $625m to $650m to $600m single point, with a range of $540m to $660m while guiding material margins to the low end of the previous range of 65% to 70% and OP Ex increase also to the low end of the 10% to 15% previous range. The ratio between material sales and license/royalty revenue is estimated to be 1.3 to 1 as deferred revenue is recognized from contracts that are near EOL.

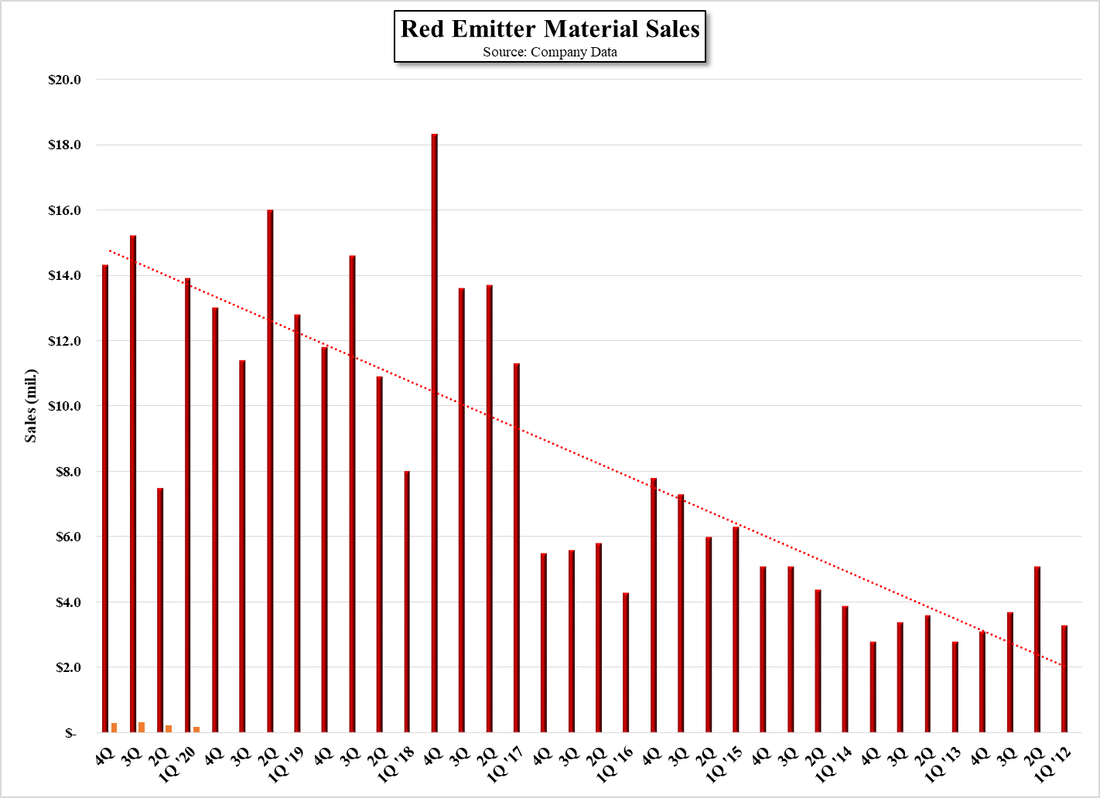

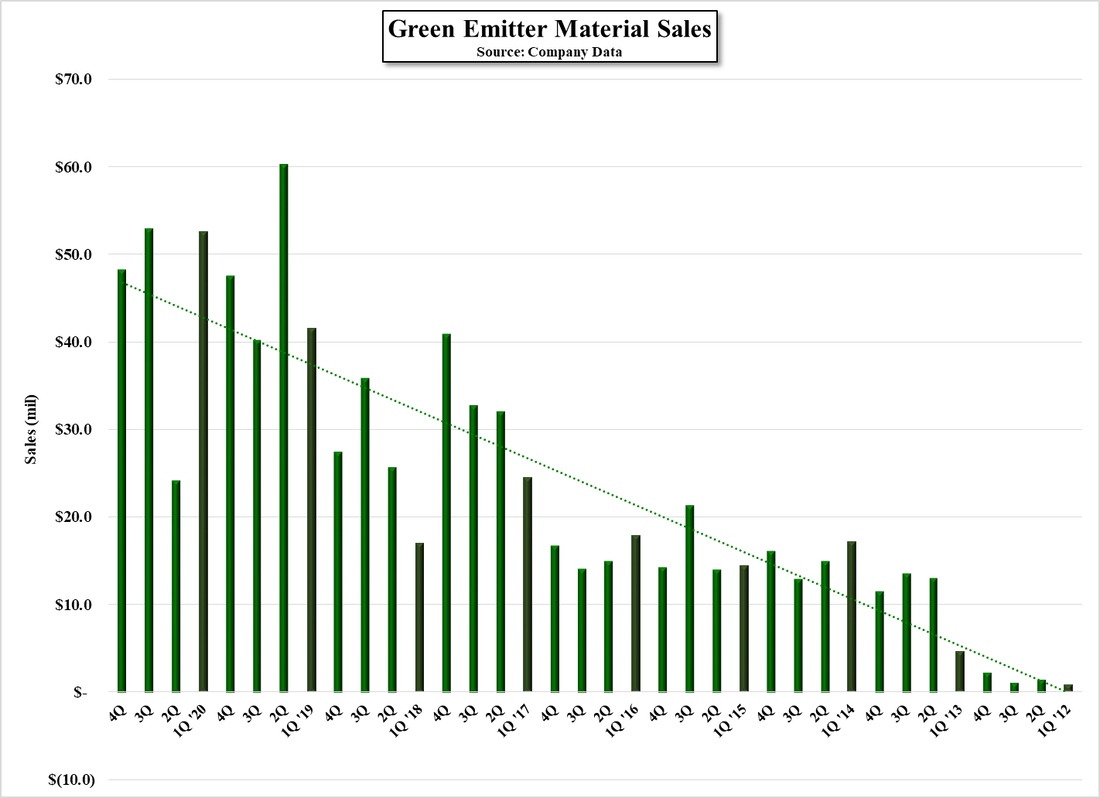

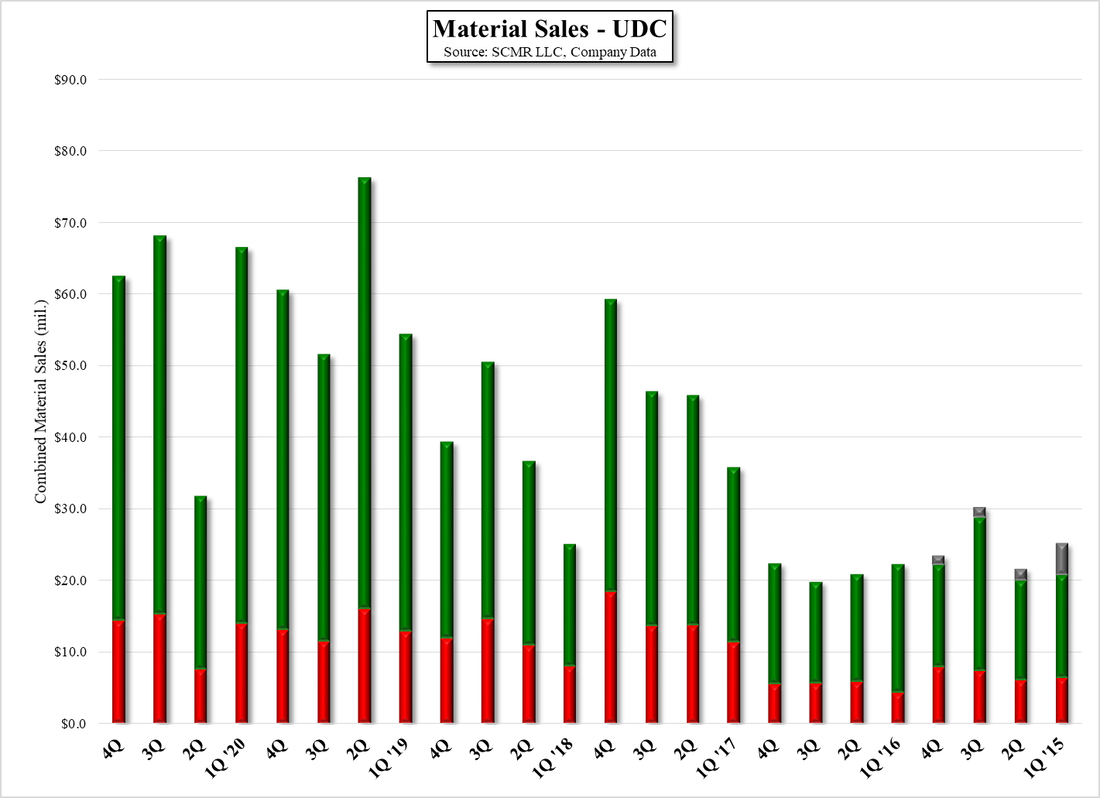

From a customer standpoint, we believe Samsung Display (pvt) reduced material purchases slightly q/q while LG Display (LPL) increased, with royalty/license up on increased unit volumes, while BOE (200725.CH) saw a 6.7% drop in combined sales, and China sales down 7.6% q/q but still up 41% y/y. While macro issues are certainly in play in China, along with COVID lockdowns, we expect overall material and license revenue to continue to grow as Chinese panel producers, particularly BOE, expand their small panel OLED customer base, despite the occasional bumps. On an overall basis, while we look specifically at quarterly red and green emitter sales, we feel smoothing the numbers across 6 quarters gives a better understanding of material sales growth by filtering out quarterly ordering inconsistencies. We do note that raw material inventory levels increased substantially in 2Q (see Figure 2 & Figure 3) although the price of iridium, a metal on which UDC’s phosphorescent emitters are based, seems to have stabilized, however given the 3Q release of the new iPhone line, we expect UDC is making sure they have enough raw material to supply Apple’s (AAPL) three iPhone display suppliers, all of whom are UDC’s largest customers, which is similar to what occurred in 2Q 2020.

Given the obvious macro issues that are facing the CE space, the weakness in UDC’s sales is not surprising and the days of OLED production capacity growth masking macro or seasonality are long gone, but we do note that revenue across the large panel LCD space declined by 17.6% q/q in 2Q, so a decline of 9.2% would seem to imply that overall OLED growth is still able to provide some protection from the full effects of weakening demand and high inventory levels, while the guidance also implies a bit over 8% sales growth for the full year. While management looks at the current conditions as short-term, with a strong focus on 2024 when a number of planned OLED capacity additions are expected to come on-line, we expect that a weak 2H and 2023 Chinese New Year might slow those plans. There are considerations as to deposition equipment ordering, which must be done far in advance of actual production to insure delivery schedules, but even those can slip by a quarter or so if things deteriorate further or Chinese finding becomes more difficult.

There is still considerable play in full-year sales for UDC, although we now expect sales of $597m, which implies hefty 4Q y/y revenue growth of 17.5% and a relatively flat 3Q as Apple releases the iPhone 14 family and a variety of smaller volume but higher surface area products are released for the holidays, with the potential for some of the growth to be pulled into 3Q. We still believe there is growth in the OLED display space but with the higher macro risk level that comes from a more mature infrastructure and exposure to rising costs. That said, we believe if there is some degree of safety in the display world, it is in the OLED space and as the primary material supplier to the industry UDC has the most exposure..

From a customer standpoint, we believe Samsung Display (pvt) reduced material purchases slightly q/q while LG Display (LPL) increased, with royalty/license up on increased unit volumes, while BOE (200725.CH) saw a 6.7% drop in combined sales, and China sales down 7.6% q/q but still up 41% y/y. While macro issues are certainly in play in China, along with COVID lockdowns, we expect overall material and license revenue to continue to grow as Chinese panel producers, particularly BOE, expand their small panel OLED customer base, despite the occasional bumps. On an overall basis, while we look specifically at quarterly red and green emitter sales, we feel smoothing the numbers across 6 quarters gives a better understanding of material sales growth by filtering out quarterly ordering inconsistencies. We do note that raw material inventory levels increased substantially in 2Q (see Figure 2 & Figure 3) although the price of iridium, a metal on which UDC’s phosphorescent emitters are based, seems to have stabilized, however given the 3Q release of the new iPhone line, we expect UDC is making sure they have enough raw material to supply Apple’s (AAPL) three iPhone display suppliers, all of whom are UDC’s largest customers, which is similar to what occurred in 2Q 2020.

Given the obvious macro issues that are facing the CE space, the weakness in UDC’s sales is not surprising and the days of OLED production capacity growth masking macro or seasonality are long gone, but we do note that revenue across the large panel LCD space declined by 17.6% q/q in 2Q, so a decline of 9.2% would seem to imply that overall OLED growth is still able to provide some protection from the full effects of weakening demand and high inventory levels, while the guidance also implies a bit over 8% sales growth for the full year. While management looks at the current conditions as short-term, with a strong focus on 2024 when a number of planned OLED capacity additions are expected to come on-line, we expect that a weak 2H and 2023 Chinese New Year might slow those plans. There are considerations as to deposition equipment ordering, which must be done far in advance of actual production to insure delivery schedules, but even those can slip by a quarter or so if things deteriorate further or Chinese finding becomes more difficult.

There is still considerable play in full-year sales for UDC, although we now expect sales of $597m, which implies hefty 4Q y/y revenue growth of 17.5% and a relatively flat 3Q as Apple releases the iPhone 14 family and a variety of smaller volume but higher surface area products are released for the holidays, with the potential for some of the growth to be pulled into 3Q. We still believe there is growth in the OLED display space but with the higher macro risk level that comes from a more mature infrastructure and exposure to rising costs. That said, we believe if there is some degree of safety in the display world, it is in the OLED space and as the primary material supplier to the industry UDC has the most exposure..

Universal Display - Quarterly Sales & Forecast - Source: SCMR LLC, Company Data

Universal Display - Raw Material Inventory as a Percentage of Material Sales - Source: SCMR LLC, Company Data

Universal Display - Material Margins - Source: SCMR LLC, Company Data

Material Sales - UDC - Source: SCMR LLC, Company Data

Universal Display Revenue Category Ratio - Source: SCMR LLC, Company Data

Red & Green Emitter Sales- Absolute & Smoothed - Source: SCMR LLC, Company Data

Universal Display - Regional Sales - Source: SCMR LLC, Company Data

Universal Display - Regional Share - China & Korea - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed