Universal Display – Iridium Inflation & Transitioning to Next-Generation Architecture

The Fourth-quarter Catch-Up: An Accounting Signal of Pricing Shifts

Universal Display (OLED) reported fourth-quarter sales that were in-line with consensus and slightly better than our estimate of $171.7 million. In that number was a cumulative $10 million catch-up adjustment, roughly double that of fourth quarter 2024. We believe the adjustment and the company’s conservative 2026 guidance ($650 to $700 million), have some significance to each other and reflect the unusual state of the OLED industry this year. While we can spend time detailing UDC’s fourth-quarter and full year 2025 results, we see this “connection” as an indicator of the company’s current view of the OLED space and the general status as to the development of a blue phosphorescent emitter.

The 4th quarter conference call sent a few “smoke signals” as to how UDC management is looking at the 2026 year, particularly the ASC 606 adjustment that was made in 4th quarter, and the mention of the increasing price of iridium, the heavy metal used in many of UDC’s phosphorescent materials.

The Iridium Factor: Pass-Throughs and Supply Chain Volatility

The price of iridium remained relatively stable through the first half of 2025 but began to climb in 3Q and spiked in 4th quarter. Iridium is one of the rarest metals on earth and is typically produced as a byproduct of platinum mining, making it unusually sensitive to disruptions. As Russia produces between 10% and 15% of the global supply, when the government of Russia began a ‘reclassification’ of rare earths and strategic minerals in November of last year, in response to Western sanctions, panic buying began. In December, the EU began developing new sanctions against Russia that included Russian metal imports. This, combined with both the Russian sanction response and some 4th quarter demand[1], caused the price of iridium to rise by almost 45%, as shown below (Units=oz.).

12/31/24 $4,200

03/31/25 $4,250

06/30/25 $4,200

09/30/25 $4,600

12/31/25 $6,650

While we believe that the emitter materials UDC produced in fourth quarter were synthesized with iridium purchased about six months earlier at lower prices, we expect the impact of the iridium price hike seen in fourth quarter 2025 will be affecting materials produced by UDC in 2H 2026. Given the material cost escalators built into the company’s supply contracts, we expect UDC will increase material prices in second half, accounting for the company’s comments concerning 2026 being a more “normal” year, with a stronger 2nd half.

Revenue Recognition Mechanics: The "TETP" Early Warning

That said, companies that operate under ASC 606 must reassess each customers contract model on a quarterly basis, and the fourth- quarter hike in iridium prices likely caused the ~$10 million catch-up that UDC recorded in 4th quarter, roughly twice what it was in 2024. We see this near-term revenue recognition boost as a bit of an “early warning” of a price increase in 2026. The reassessment of the ASC 606 model reflects the higher cost in fourth-quarter, but more importantly points to the pass-through of the iridium price hikes later this year.

Shifting Fundamentals: Material Intensity vs. Royalty Revenue

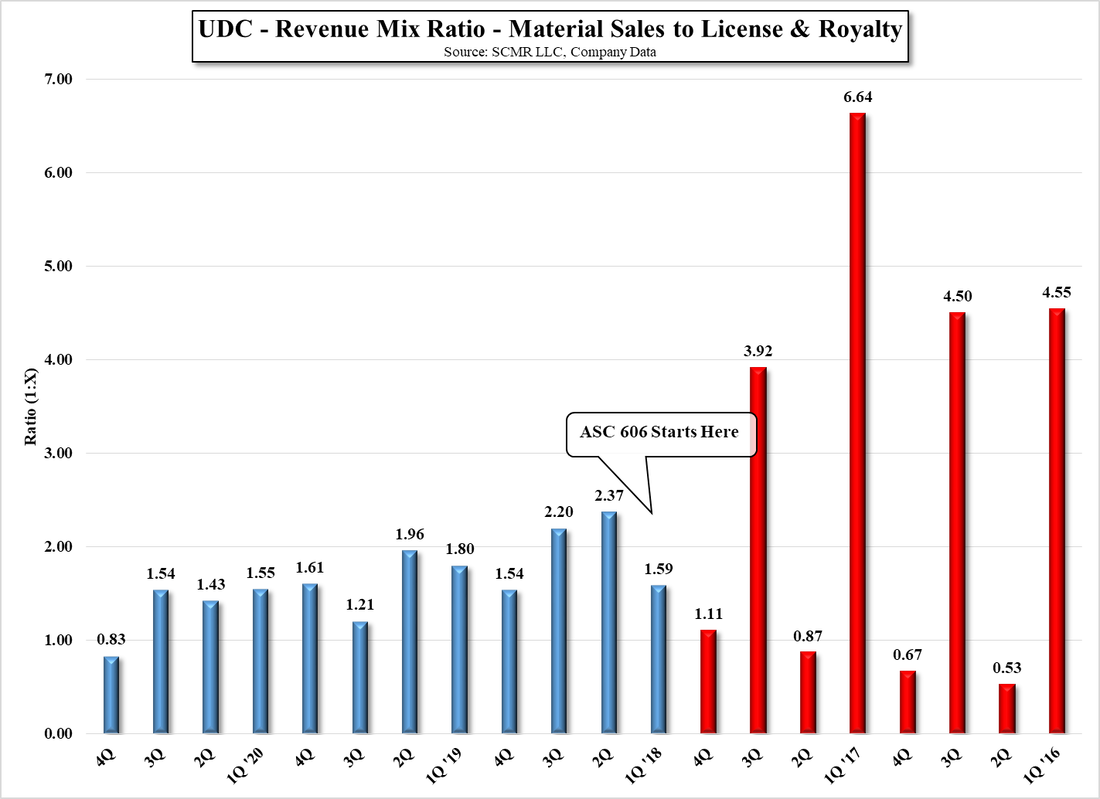

This is also confirmed by the lower gross margin guidance for 2026 given by management. This indicates higher revenue but revenue that just covers the higher material cost and does not add to the bottom line as would existing materials produced after the price hike. This lower gross margin guidance also jives with the 1Q 2026 company guidance on UDC’s material-to-royalty ratio (1.3:1), which implies that 2026 will be a year more heavily weighted toward material sales, which carry a lower gross margin than license/royalty revenue. The cause for this shift could be the higher material ASP caused by the iridium price hike, but, on a more positive note, it also could be a result of the increased use of tandem emitter material stacks, which imply higher material sales per device unit leading to a lower material to license ratio.

[1] Iridium is a catalyst for Green Hydrogen PEM electrolyzers

Universal Display (OLED) reported fourth-quarter sales that were in-line with consensus and slightly better than our estimate of $171.7 million. In that number was a cumulative $10 million catch-up adjustment, roughly double that of fourth quarter 2024. We believe the adjustment and the company’s conservative 2026 guidance ($650 to $700 million), have some significance to each other and reflect the unusual state of the OLED industry this year. While we can spend time detailing UDC’s fourth-quarter and full year 2025 results, we see this “connection” as an indicator of the company’s current view of the OLED space and the general status as to the development of a blue phosphorescent emitter.

The 4th quarter conference call sent a few “smoke signals” as to how UDC management is looking at the 2026 year, particularly the ASC 606 adjustment that was made in 4th quarter, and the mention of the increasing price of iridium, the heavy metal used in many of UDC’s phosphorescent materials.

The Iridium Factor: Pass-Throughs and Supply Chain Volatility

The price of iridium remained relatively stable through the first half of 2025 but began to climb in 3Q and spiked in 4th quarter. Iridium is one of the rarest metals on earth and is typically produced as a byproduct of platinum mining, making it unusually sensitive to disruptions. As Russia produces between 10% and 15% of the global supply, when the government of Russia began a ‘reclassification’ of rare earths and strategic minerals in November of last year, in response to Western sanctions, panic buying began. In December, the EU began developing new sanctions against Russia that included Russian metal imports. This, combined with both the Russian sanction response and some 4th quarter demand[1], caused the price of iridium to rise by almost 45%, as shown below (Units=oz.).

12/31/24 $4,200

03/31/25 $4,250

06/30/25 $4,200

09/30/25 $4,600

12/31/25 $6,650

While we believe that the emitter materials UDC produced in fourth quarter were synthesized with iridium purchased about six months earlier at lower prices, we expect the impact of the iridium price hike seen in fourth quarter 2025 will be affecting materials produced by UDC in 2H 2026. Given the material cost escalators built into the company’s supply contracts, we expect UDC will increase material prices in second half, accounting for the company’s comments concerning 2026 being a more “normal” year, with a stronger 2nd half.

Revenue Recognition Mechanics: The "TETP" Early Warning

That said, companies that operate under ASC 606 must reassess each customers contract model on a quarterly basis, and the fourth- quarter hike in iridium prices likely caused the ~$10 million catch-up that UDC recorded in 4th quarter, roughly twice what it was in 2024. We see this near-term revenue recognition boost as a bit of an “early warning” of a price increase in 2026. The reassessment of the ASC 606 model reflects the higher cost in fourth-quarter, but more importantly points to the pass-through of the iridium price hikes later this year.

Shifting Fundamentals: Material Intensity vs. Royalty Revenue

This is also confirmed by the lower gross margin guidance for 2026 given by management. This indicates higher revenue but revenue that just covers the higher material cost and does not add to the bottom line as would existing materials produced after the price hike. This lower gross margin guidance also jives with the 1Q 2026 company guidance on UDC’s material-to-royalty ratio (1.3:1), which implies that 2026 will be a year more heavily weighted toward material sales, which carry a lower gross margin than license/royalty revenue. The cause for this shift could be the higher material ASP caused by the iridium price hike, but, on a more positive note, it also could be a result of the increased use of tandem emitter material stacks, which imply higher material sales per device unit leading to a lower material to license ratio.

[1] Iridium is a catalyst for Green Hydrogen PEM electrolyzers

Divining the causation for management’s conservative guidance, the implications of the ASC 606 catch-up, and the modified material/license ratio lead us to focus more on the ASC model that governs how companies recognize long-term contractual revenue. The basis for the model is the relationship between actual material sales and the recognition of license/royalty revenue. The rule ties the recognition of license/royalty revenue to material sales over the life of the contract, using the estimated value of the contract as the basis that is adjusted each quarter. Therefore license/royalty is recognized as material is sold on a per-gram basis rather than when it is received. This makes quarterly results highly sensitive to changes (such as material prices or new architectures) in the “Total Estimated Transaction Price” of a particular contract. As these changes affect the TETP the company is required to make positive or negative catch-up adjustments that reflect how the full five-year contract value has changed over the period.

The 2026 "Puts and Takes": Analyzing the Bridge to 2027

Based on the factors above and others mentioned on the call, here are the puts and takes we see for 2026.

Positives

Tandem Architecture – As we have mentioned in previous notes, tandem OLED architecture leads to the use of higher material volumes per unit. As this architecture becomes more common, the overall rate of material consumption on a per-unit basis will increase, causing the value of a long-term contract to increase

Cash – With $955 million in cash (~17% of market cap) and little need for major capital expenditures, the company increased its dividend in fourth-quarter. While not a dividend play by any means, it gives investors a cushion when waiting for an incremental step up in sales. The company’s cash and investments alone generated ~46.4% of the 2025 dividend payout.

Neutral

Blue – UDC management made few comments about the status of blue phosphorescent material development, other than the standard ‘…making progress…”. We believe that blue development is a mixed bag for UDC in 2026 as the adoption of current blue phosphorescent materials faces a more competitive picture than only a year or so ago. Tandem and multiple layer structures are giving OLED producers the ability to capture some of the power, efficiency, or lifetime advantages of blue phosphorescent emitter materials using materials that are more mature and readily available. This puts blue into a more discretionary adoption mode, where OLED producers can take time to evaluate the physical advantages of the material against the cost of adoption, leading to a more conservative adoption profile. That said, when it is adopted, there will be a substantial increment in sales over time and the value of those contracts that include blue will be stepped up.

Negatives

Gen 8.6 adoption – Will not much of a surprise, the commissioning of Samsung Display’s Gen8.6 IT OLED fab in second quarter and a similar fab from BOE (200725.CH) likely in third quarter, will contribute relatively small amounts to sales this year relative to expectations in 2024 and early 2025. There is nothing holding these fabs back, but as we have noted in the past, the ramp toward profitable yields and utilization takes time, with the bulk of the incremental sales from these fabs more likely seen in 2027.

Leverage – Under the company’s conservative sales guidance and Operating expense growth of 7% to 9% *R&D and SG&A), expenses will grow faster than revenue leading to negative operating leverage. While this is a negative we expect that behind the conservative guidance the company is a bit more optimistic about sales prospects for the year. That said, given the fact that we are only a month and a half into the new year and the technology space has already faced some major upheavals (tariff changes), we expect guidance to improve as there is more clarity on a number of the issues we mentioned above, bringing the leverage back to the positive.

Conclusion: A Year of Operational Calibration

The intersection of aggressive raw material inflation and the strategic shift toward high-area IT displays has moved Universal Display into a period of significant operational calibration. The $650 million to $700 million guidance and subsequent margin compression reflect a defensive posture in the face of iridium price volatility, but also widens the potential upside as clarity improves across the 2026 OLED space. UDC’s growth thesis is currently a race between two competing forces: the "mechanical" revenue lift provided by ASC 606 catch-ups and contract escalators, and the structural "purgatory" of waiting for Gen 8.6 fabs and Blue Phosphorescent Emitter adoption to reach commercial maturity.

The path to upside is clear but narrow. If the industry can successfully navigate the "yield tax" of Tandem architectures and the initial yield and utilization issues of new fab ramps, UDC stands to benefit from a significant increase in material intensity per device. However, this potential remains tempered by a negative operating leverage profile and a material-to-license ratio that currently favors lower-margin physical sales over high-margin IP royalties.

Ultimately, 2026 is less about a breakout and more about the durability of UDC’s ability to navigate a difficult year. With a $955 million cash cushion and a dividend program that is nearly 50% subsidized by interest income, UDC is better positioned than most to absorb the "unusual state" of the current market. Investors should view the coming year as a bridge: if management can maintain cost discipline while these headwinds persist, the eventual normalization of raw material prices and the scaling of next-gen fabs in 2027 could turn today's conservative guidance into a foundational floor for the next leg of growth, with “Blue” being a major kicker.

The 2026 "Puts and Takes": Analyzing the Bridge to 2027

Based on the factors above and others mentioned on the call, here are the puts and takes we see for 2026.

Positives

Tandem Architecture – As we have mentioned in previous notes, tandem OLED architecture leads to the use of higher material volumes per unit. As this architecture becomes more common, the overall rate of material consumption on a per-unit basis will increase, causing the value of a long-term contract to increase

Cash – With $955 million in cash (~17% of market cap) and little need for major capital expenditures, the company increased its dividend in fourth-quarter. While not a dividend play by any means, it gives investors a cushion when waiting for an incremental step up in sales. The company’s cash and investments alone generated ~46.4% of the 2025 dividend payout.

Neutral

Blue – UDC management made few comments about the status of blue phosphorescent material development, other than the standard ‘…making progress…”. We believe that blue development is a mixed bag for UDC in 2026 as the adoption of current blue phosphorescent materials faces a more competitive picture than only a year or so ago. Tandem and multiple layer structures are giving OLED producers the ability to capture some of the power, efficiency, or lifetime advantages of blue phosphorescent emitter materials using materials that are more mature and readily available. This puts blue into a more discretionary adoption mode, where OLED producers can take time to evaluate the physical advantages of the material against the cost of adoption, leading to a more conservative adoption profile. That said, when it is adopted, there will be a substantial increment in sales over time and the value of those contracts that include blue will be stepped up.

Negatives

Gen 8.6 adoption – Will not much of a surprise, the commissioning of Samsung Display’s Gen8.6 IT OLED fab in second quarter and a similar fab from BOE (200725.CH) likely in third quarter, will contribute relatively small amounts to sales this year relative to expectations in 2024 and early 2025. There is nothing holding these fabs back, but as we have noted in the past, the ramp toward profitable yields and utilization takes time, with the bulk of the incremental sales from these fabs more likely seen in 2027.

Leverage – Under the company’s conservative sales guidance and Operating expense growth of 7% to 9% *R&D and SG&A), expenses will grow faster than revenue leading to negative operating leverage. While this is a negative we expect that behind the conservative guidance the company is a bit more optimistic about sales prospects for the year. That said, given the fact that we are only a month and a half into the new year and the technology space has already faced some major upheavals (tariff changes), we expect guidance to improve as there is more clarity on a number of the issues we mentioned above, bringing the leverage back to the positive.

Conclusion: A Year of Operational Calibration

The intersection of aggressive raw material inflation and the strategic shift toward high-area IT displays has moved Universal Display into a period of significant operational calibration. The $650 million to $700 million guidance and subsequent margin compression reflect a defensive posture in the face of iridium price volatility, but also widens the potential upside as clarity improves across the 2026 OLED space. UDC’s growth thesis is currently a race between two competing forces: the "mechanical" revenue lift provided by ASC 606 catch-ups and contract escalators, and the structural "purgatory" of waiting for Gen 8.6 fabs and Blue Phosphorescent Emitter adoption to reach commercial maturity.

The path to upside is clear but narrow. If the industry can successfully navigate the "yield tax" of Tandem architectures and the initial yield and utilization issues of new fab ramps, UDC stands to benefit from a significant increase in material intensity per device. However, this potential remains tempered by a negative operating leverage profile and a material-to-license ratio that currently favors lower-margin physical sales over high-margin IP royalties.

Ultimately, 2026 is less about a breakout and more about the durability of UDC’s ability to navigate a difficult year. With a $955 million cash cushion and a dividend program that is nearly 50% subsidized by interest income, UDC is better positioned than most to absorb the "unusual state" of the current market. Investors should view the coming year as a bridge: if management can maintain cost discipline while these headwinds persist, the eventual normalization of raw material prices and the scaling of next-gen fabs in 2027 could turn today's conservative guidance into a foundational floor for the next leg of growth, with “Blue” being a major kicker.

RSS Feed

RSS Feed