Early March Panel Prices

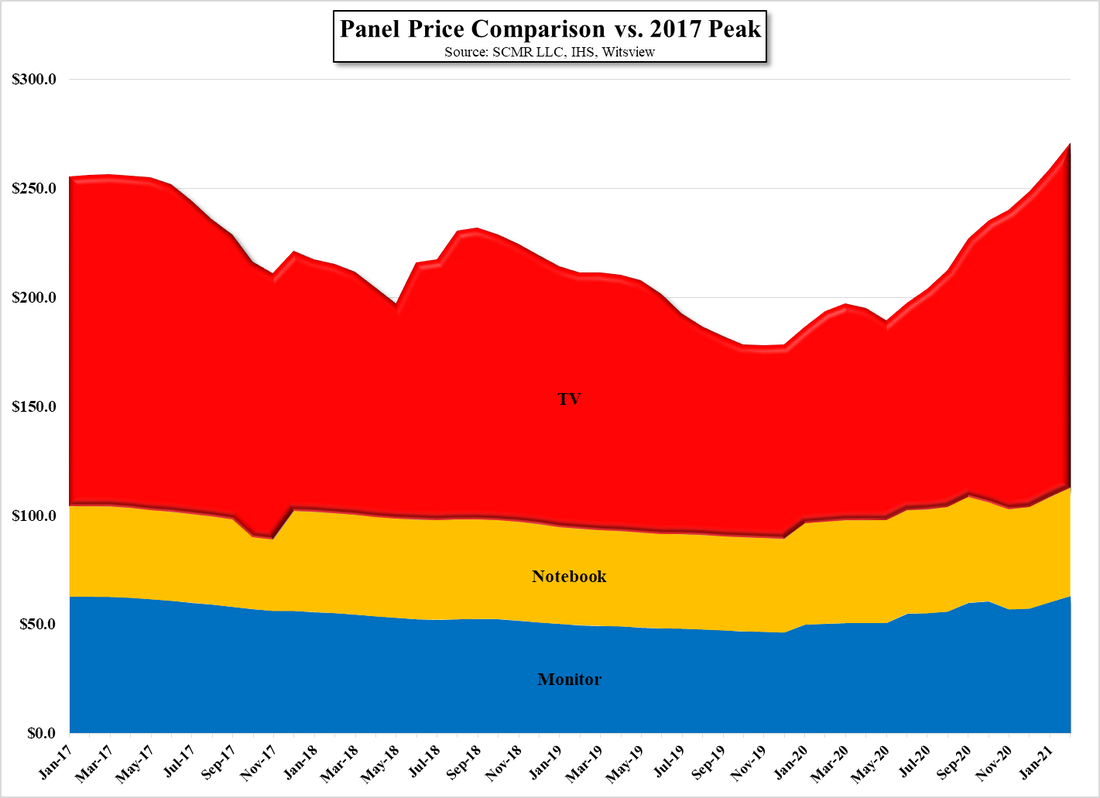

LCD panel prices continue to rise and expectations from panel producers and set producers continue to see the same for much of the 1st half. That said, comments from panel producers also cite the fact that some are not producing at full capacity, despite demand, as component shortages are limiting their ability to deliver completed product. That said, we still expect panel prices to increase this month, with notebook panels up between 2.0% and 2.5%, monitor panels up 1.0% to 1.7%, and TV panels to increase between 2.1% and 3.2%. While we expect it might be hard to pin down a specific comment, there has been talk that panel producers are looking to see panel prices reach peak prices seen in 2017, however those prices have already been reached this year.

While we expect shortages to keep panel buyers under constraints to meet early 2021 quotas, demand is still being ‘regulated’ by the necessity for stay-at-home scenarios, a result of COVID-19, and while the virus is still at pandemic levels, vaccines and a more stringent public health requirements on a global basis, seem to be having at least some effect on hospitalizations. With plans for most educational facilities, at least in the US, to be back to in=person classes by the fall, we expect demand to soften during the summer, but we also expect a lag between when demand slows and when buyers feel they can actually negotiate with panel suppliers given the desperation buyers have faced in past months. Does that push out a slowdown until 3Q or does it happen during the summer? That is a hard question to answer, but we will present four supply/demand scenarios later this week. Without giving too much away, the four scenarios are titled, ‘slow burn’, ‘Black Diamond’, ‘New Normal’, and ‘Avalanche’.

While we expect shortages to keep panel buyers under constraints to meet early 2021 quotas, demand is still being ‘regulated’ by the necessity for stay-at-home scenarios, a result of COVID-19, and while the virus is still at pandemic levels, vaccines and a more stringent public health requirements on a global basis, seem to be having at least some effect on hospitalizations. With plans for most educational facilities, at least in the US, to be back to in=person classes by the fall, we expect demand to soften during the summer, but we also expect a lag between when demand slows and when buyers feel they can actually negotiate with panel suppliers given the desperation buyers have faced in past months. Does that push out a slowdown until 3Q or does it happen during the summer? That is a hard question to answer, but we will present four supply/demand scenarios later this week. Without giving too much away, the four scenarios are titled, ‘slow burn’, ‘Black Diamond’, ‘New Normal’, and ‘Avalanche’.

Panel Price Comparison vs. 2017 Peak - Source: SCMR LLC, IHS, Witsview

RSS Feed

RSS Feed