Samsung and LG Display to evaluate LCD to OLED conversions

According to the Korean press, Samsung Display (pvt) and LG Display (LPL) are re-evaluating plans to close a number of LCD fabs and convert them to OLED production facilitates. The original concept for both companies was to take relatively low efficiency LCD fabs and either completely close the fab, or convert them to small panel OLED production, which has been in relatively short supply and would potentially be facing increased demand from smartphone brands wishing to add or increase the ratio of OLED smartphones to their lines, in particular, Apple (AAPL) and Chinese brands.

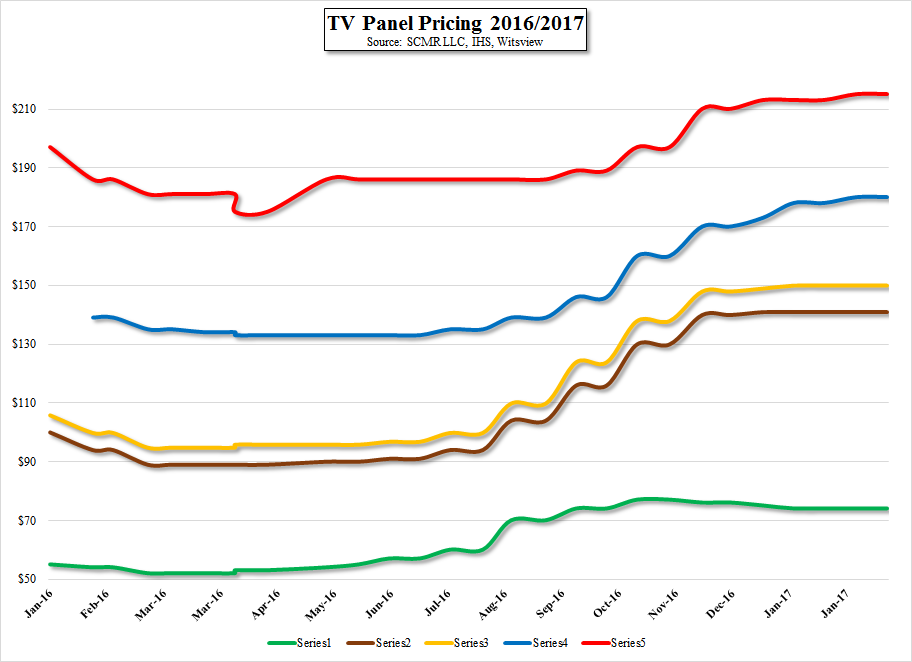

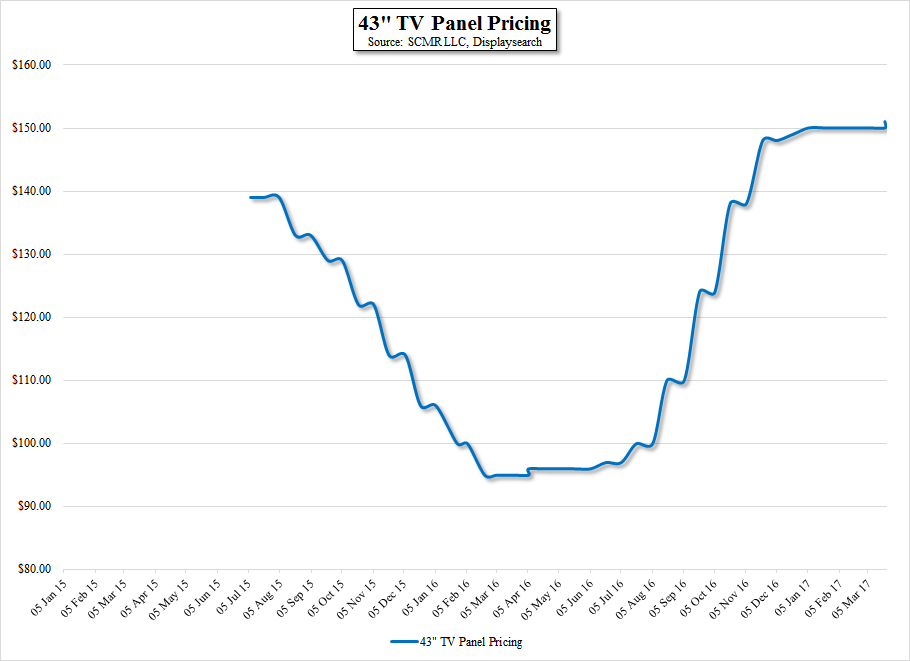

The conversion of such LCD fabs to OLED would give these producers more OLED capacity, however it also has the effect of reducing the supply of LCD display panels, and while in recent weeks the upward pressure on LCD panel pricing has moderated somewhat, the closings that have already taken place and the prospects for additional closings will keep the display industry in a relatively tight supply situation. By holding back the prospective closings, industry participants will better be able to fill demand for those panels that have seen substantial price increases, and participate in the improved pricing and margin environment.

The conversion of such LCD fabs to OLED would give these producers more OLED capacity, however it also has the effect of reducing the supply of LCD display panels, and while in recent weeks the upward pressure on LCD panel pricing has moderated somewhat, the closings that have already taken place and the prospects for additional closings will keep the display industry in a relatively tight supply situation. By holding back the prospective closings, industry participants will better be able to fill demand for those panels that have seen substantial price increases, and participate in the improved pricing and margin environment.

TV Panel Pricing 2016/2017 - Source: SCMR LLC, Witsview, IHS

The potential decision by Samsung Display (Matters have been made worse in this regard due to the acquisition of Sharp (6753.JP) by Hon Hai (2371.TT)/Foxconn (2354.TT) and their subsequent decision to revive the Sharp brand. This reallocation of display panels by Sharp’s management, caused them to curtail panel supply to Samsung Electronics (005930.KS) and Hisense (6000060.CH), the world’s 3rd largest TV brand behind Samsung and LG Electronics (066570.KS), tightening the market further, and forcing Samsung Electronics to go to rival LG Display for replacement panels, limiting LGD’s ability to supply its other potential customers. We believe Sharp had been supplying ~10% of Samsung Electronics’ display panels before the change last December.

Of course altruism for the industry is not the only motivation here, as Samsung owns Samsung Electronics, which provides a significant portion of the company’s profitability, and Samsung Display is a subsidiary of Samsung Electronics, so by missing out on the ability to capitalize on the TV panel price increases seen in recent months, the overall Samsung profitability ‘chain’ becomes limited. But what about OLED? The objective for Samsung’s conversions was to take less efficient LCD plants and convert them to small panel OLED production, which has been in relatively short supply since it became a viable commercial display product. As small panel OLED becomes more popular, along with the potential for Apple to add significantly to demand with an OLED based iPhone display, Samsung Display, as the primary supplier (90%+ of small panel OLED), needed the converted capacity to supply the industry with OLED displays, another profitable product for the company.

The tradeoff is complicated, as Samsung Electronics, as a TV brand, has seen rising costs and lower TV margins over the last year due to the panel price increases. Should Samsung Display limit its plant closings and conversions, the result would likely be panel price stability, or the potential for panel price declines. This would be less desirable for Samsung Display, but very helpful to parent Samsung Electronics, who would see TV margin improvement. Samsung Display also plays into the equation, as the timing of the conversions, some of which would not be completed until 2018, would leave the company without revenue in either the LCD or OLED categories for these fabs, so the question then becomes, is it better to continue to produce what are now higher margin TV panels on the fabs in question for the near term, or lose the near-term revenue and build the potential for additional OLED capacity down the road?

Normally, Samsung takes the longer view, and tends to build for the long-term, but things are moving far more quickly in the display space than they have over the last few years, and the issues facing Samsung management are far different than in previous years. With the Samsung Electronics vice-chairman under indictment, and the dissolution of the Samsung office that controlled affiliates as a group, each affiliate has greater control over their own fate, and the affiliated division heads now in control have a far more detailed view of the issues facing the consumer electronics and display industries than the previous oligarchy. Will this mean better decisions? That depends on how well the affiliates work with each other, but we would expect the focus will be somewhat shorter-term and oriented toward near-term results in order for the ‘new’ management to prove their abilities and expertise.

We doubt the changes will be as cut and dried as the Korean press might indicate, and such decisions are more likely to postpone rather than eliminate, but will this affect Apple’s OLED project for the iPhone 8? Not likely, as we would expect that any agreement between Apple and Samsung Display would be based on a pre-payment toward ‘available volume’, giving Apple semi-dedicated production lines at Samsung Display, based on an agreed upon schedule of capacity expansion (which would be partially financed by an Apple pre-payment). Would it change Apple’s ability to release an OLED iPhone this year or was the potential decision by Samsung to slow the conversions (if true) due to Apple’s less aggressive OLED plans? We will map those rather complex scenarios in days following, but we can look at the impact of the potential Samsung and LG changes.

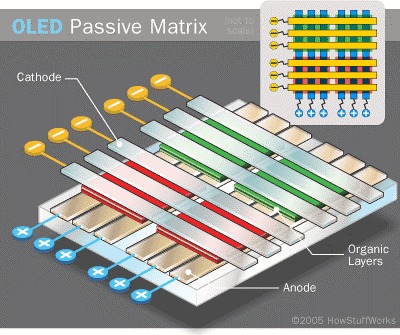

Samsung Display has three commercial OLED facilities named A1, A2, and A3. A1, the smallest of the three, has been producing OLED displays since 2009 and uses a gen 4.5 rigid substrate. A2 has been producing since 2011, and is a gen 5.5 fab, but has some capability for both rigid and flexible substrates. A3, which began limited production in mid-2015 is a Gen 6 fab that is designed for flexible substrates, and continues to be expanded. While Samsung has other R&D and pilot lines, including the Gen 8 lines where it originally produced OLED TVs, their OLED production is based on the three ‘A’ lines. The two major conversion projects were the conversion of L7-1, a Gen 7 LCD fab that was put into service in 2005, with a capacity for 140,000 sheets/month. The conversion to a Gen 6 OLED facility was expected to be done in two phases, with the 1st being put into ramp mode in 3Q 2017 and the 2nd roughly a year later, but the total OLED capacity would be close to 44,000 sheets/month. The 2nd conversion, a Gen 5 a-Si line going back to initial production in 2003 has the maximum capacity of ~200,000 sheets/month, with expectations for the three phase conversion producing 60,000 sheets/month of mixed rigid and flexible OLED capacity, scheduled for phase 1 ramp early in 2018, although few details as to substrate size format have been revealed.

Of course altruism for the industry is not the only motivation here, as Samsung owns Samsung Electronics, which provides a significant portion of the company’s profitability, and Samsung Display is a subsidiary of Samsung Electronics, so by missing out on the ability to capitalize on the TV panel price increases seen in recent months, the overall Samsung profitability ‘chain’ becomes limited. But what about OLED? The objective for Samsung’s conversions was to take less efficient LCD plants and convert them to small panel OLED production, which has been in relatively short supply since it became a viable commercial display product. As small panel OLED becomes more popular, along with the potential for Apple to add significantly to demand with an OLED based iPhone display, Samsung Display, as the primary supplier (90%+ of small panel OLED), needed the converted capacity to supply the industry with OLED displays, another profitable product for the company.

The tradeoff is complicated, as Samsung Electronics, as a TV brand, has seen rising costs and lower TV margins over the last year due to the panel price increases. Should Samsung Display limit its plant closings and conversions, the result would likely be panel price stability, or the potential for panel price declines. This would be less desirable for Samsung Display, but very helpful to parent Samsung Electronics, who would see TV margin improvement. Samsung Display also plays into the equation, as the timing of the conversions, some of which would not be completed until 2018, would leave the company without revenue in either the LCD or OLED categories for these fabs, so the question then becomes, is it better to continue to produce what are now higher margin TV panels on the fabs in question for the near term, or lose the near-term revenue and build the potential for additional OLED capacity down the road?

Normally, Samsung takes the longer view, and tends to build for the long-term, but things are moving far more quickly in the display space than they have over the last few years, and the issues facing Samsung management are far different than in previous years. With the Samsung Electronics vice-chairman under indictment, and the dissolution of the Samsung office that controlled affiliates as a group, each affiliate has greater control over their own fate, and the affiliated division heads now in control have a far more detailed view of the issues facing the consumer electronics and display industries than the previous oligarchy. Will this mean better decisions? That depends on how well the affiliates work with each other, but we would expect the focus will be somewhat shorter-term and oriented toward near-term results in order for the ‘new’ management to prove their abilities and expertise.

We doubt the changes will be as cut and dried as the Korean press might indicate, and such decisions are more likely to postpone rather than eliminate, but will this affect Apple’s OLED project for the iPhone 8? Not likely, as we would expect that any agreement between Apple and Samsung Display would be based on a pre-payment toward ‘available volume’, giving Apple semi-dedicated production lines at Samsung Display, based on an agreed upon schedule of capacity expansion (which would be partially financed by an Apple pre-payment). Would it change Apple’s ability to release an OLED iPhone this year or was the potential decision by Samsung to slow the conversions (if true) due to Apple’s less aggressive OLED plans? We will map those rather complex scenarios in days following, but we can look at the impact of the potential Samsung and LG changes.

Samsung Display has three commercial OLED facilities named A1, A2, and A3. A1, the smallest of the three, has been producing OLED displays since 2009 and uses a gen 4.5 rigid substrate. A2 has been producing since 2011, and is a gen 5.5 fab, but has some capability for both rigid and flexible substrates. A3, which began limited production in mid-2015 is a Gen 6 fab that is designed for flexible substrates, and continues to be expanded. While Samsung has other R&D and pilot lines, including the Gen 8 lines where it originally produced OLED TVs, their OLED production is based on the three ‘A’ lines. The two major conversion projects were the conversion of L7-1, a Gen 7 LCD fab that was put into service in 2005, with a capacity for 140,000 sheets/month. The conversion to a Gen 6 OLED facility was expected to be done in two phases, with the 1st being put into ramp mode in 3Q 2017 and the 2nd roughly a year later, but the total OLED capacity would be close to 44,000 sheets/month. The 2nd conversion, a Gen 5 a-Si line going back to initial production in 2003 has the maximum capacity of ~200,000 sheets/month, with expectations for the three phase conversion producing 60,000 sheets/month of mixed rigid and flexible OLED capacity, scheduled for phase 1 ramp early in 2018, although few details as to substrate size format have been revealed.

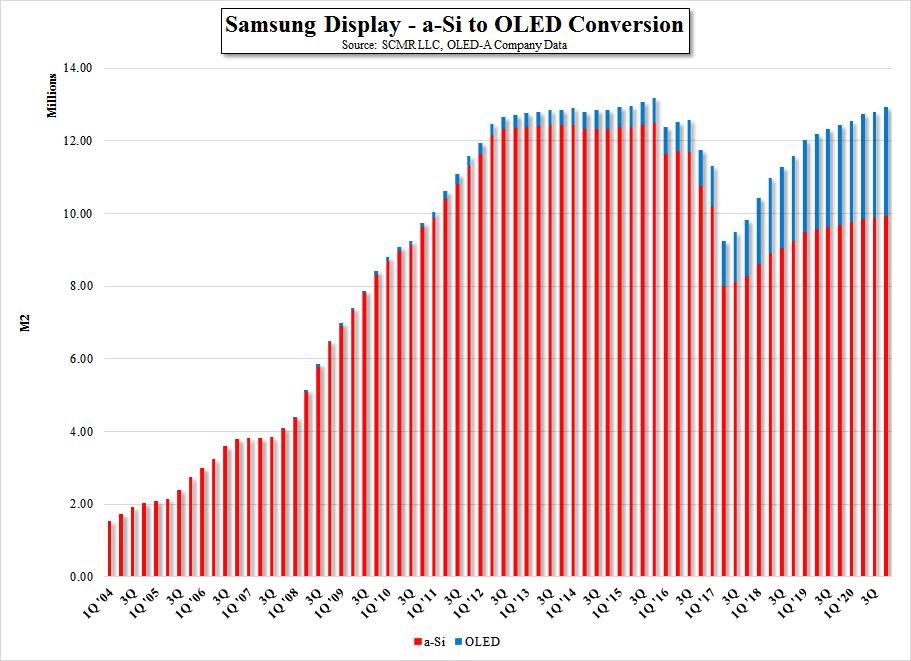

Samsung LCD to OLED Conversion Expectations - Source: SCMR LLC, OLED-A

Table 1 gives a rough idea of how the conversions would affect Samsung Display’s overall capacity on a quarterly basis, but does not give a picture of how the conversions would affect Samsung’s overall capacity on a monthly basis. In the case of L7-1, we believe the fab began to slow production in 3Q 2016, at least on the 1st line, with the goal of the actual conversion taking place at the beginning of this year, and limited OLED production beginning in September 2017. This timeline, which is just for the 1st line, leaves a hole in Samsung Display’s production that extends for a minimum of 9 months and potentially for a year when including the downward ramp of L7-1 production last year. The L6 conversion, which we believe was still on the drawing board until recently, has a similar negative impact on Samsung Display’s overall capacity, and an even more tenuous timeline, but the fact that the conversions would likely take ~9 months still remains. Figure 2 below gives a more ‘timeline’ representation of the Samsung Display conversion process as it stood before today’s press conjecture, and as can easily be seen, the impact on Samsung Display’s overall capacity is quite significant. We note that this chart includes only the conversion of amorphous silicon backplane large panel fabs, as fabs based on LTPS[1] or IGZO[2] would tend to be used for small panel production.

[1] Low Temperature Poly Silicon

[2] “Oxide” – Indium Gallium Zinc Oxide

[1] Low Temperature Poly Silicon

[2] “Oxide” – Indium Gallium Zinc Oxide

Samsung Display - a-Si to OLED Conversion - Source: SCMR LLC, OLED-A, Company Data

While translating these numbers into unit volumes and factory revenue will take a bit more time, and while TV panel production always seems to have the press headlines, small panel production generates more revenue than large panel. While this is not the only consideration, it certainly enters into Samsung’s decisions. One more important issue is that of equipment, in particular OLED deposition tools. We have indicated many times in the past that the production of OLED deposition tools is limited to a very small group of companies with Canon Tokki (7751.JP) the share leader. Tools such as these have lead times of 9 months to 15 months, and therefore tools have to be ordered far in advance of need, and have to be configured to the specs of the OLED lines. Changes to Samsung Displays OLED capex spending timeline could have an effect across the entire industry, giving others access to Canon tools that they might not have had if Samsung Display followed what was thought to be its OLED conversion schedule, although the likelihood of Samsung Display doing anything more than storing a pre-ordered OLED deposition tool for a few quarters would be very unusual. That said, others who supply materials used in the OLED process, would see changes to buying patterns should Samsung Display make any changes to its conversion schedule.

While all is still at the conjecture stage, any change in plans by Samsung Display would be considered significant, especially as to how it affects the OLED display space, the OLED supply chain, and panel pricing across the board. We will continue to evaluate these potential plan changes in days to come, with a full evaluation of the impact on Apple’s OLED plans, and will model a number of scenarios that will detail the overall impact on the display industry.

While all is still at the conjecture stage, any change in plans by Samsung Display would be considered significant, especially as to how it affects the OLED display space, the OLED supply chain, and panel pricing across the board. We will continue to evaluate these potential plan changes in days to come, with a full evaluation of the impact on Apple’s OLED plans, and will model a number of scenarios that will detail the overall impact on the display industry.

RSS Feed

RSS Feed