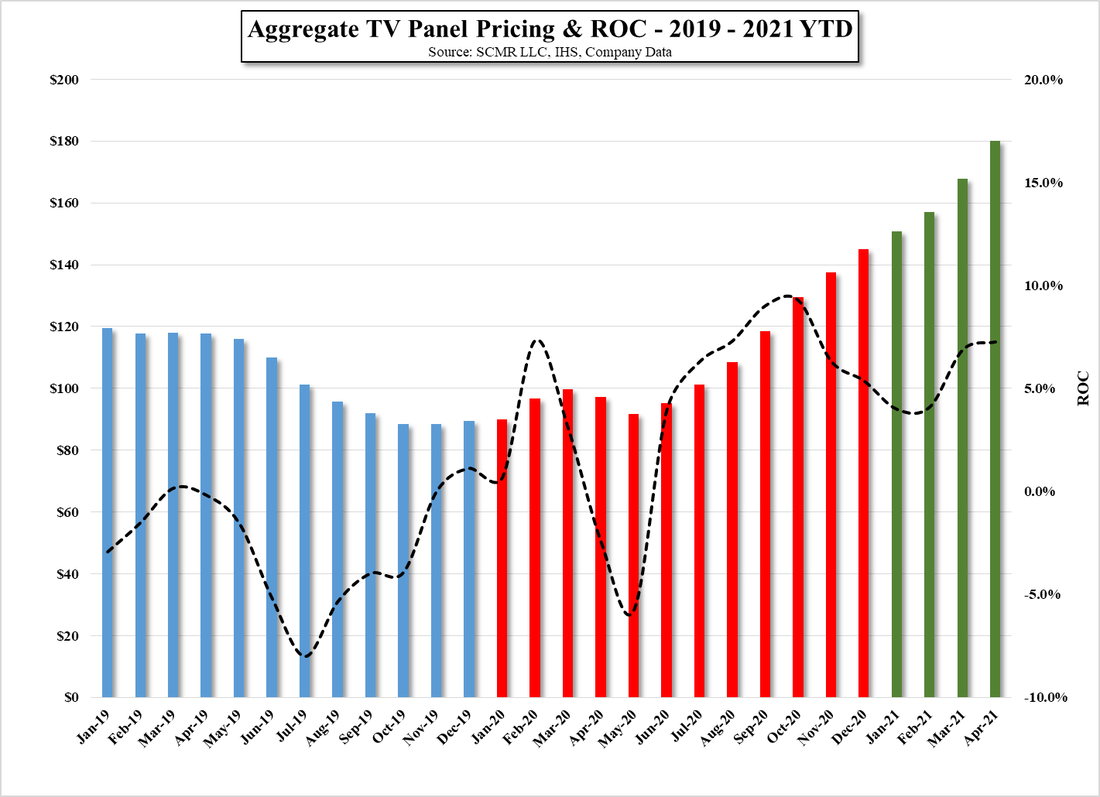

Murata ‘unofficially’ a Bit Worried About ‘Distortion’ in the Parts Market

While Murata (6981.JP) will report its full year results for its March year tomorrow, the President of Murata, the largest producer of MLCCs (Multi-layer Ceramic Capacitors), has indicated a fear that the US-Sino trade tensions are ‘distorting’ the parts market for smartphones. While he indicated that with Hauwei unable to take orders and produce for US customers, other brands, particularly the top three brands, have been increasing orders significantly. “China produces a large number of 5G smartphones. Compared with the demand of the real economy, there are signs of overheating of orders.”

This is coming from a company that is expected to see a potentially large increase in operating profit against earlier forecasts, and while analysts in Japan have mixed views as to whether current MLCC demand is real or over stated, the caution expressed seems to indicate that the company is operating with the understanding that things could change quickly if demand slows. Japanese company managements tend to be far more conservative (at least publicly) than Taiwanese or Chinese management, so we take some of this with a grain of salt, but it is not the first time we have heard a company executive express some reservation about current component order status…

This is coming from a company that is expected to see a potentially large increase in operating profit against earlier forecasts, and while analysts in Japan have mixed views as to whether current MLCC demand is real or over stated, the caution expressed seems to indicate that the company is operating with the understanding that things could change quickly if demand slows. Japanese company managements tend to be far more conservative (at least publicly) than Taiwanese or Chinese management, so we take some of this with a grain of salt, but it is not the first time we have heard a company executive express some reservation about current component order status…

RSS Feed

RSS Feed