Looking Back

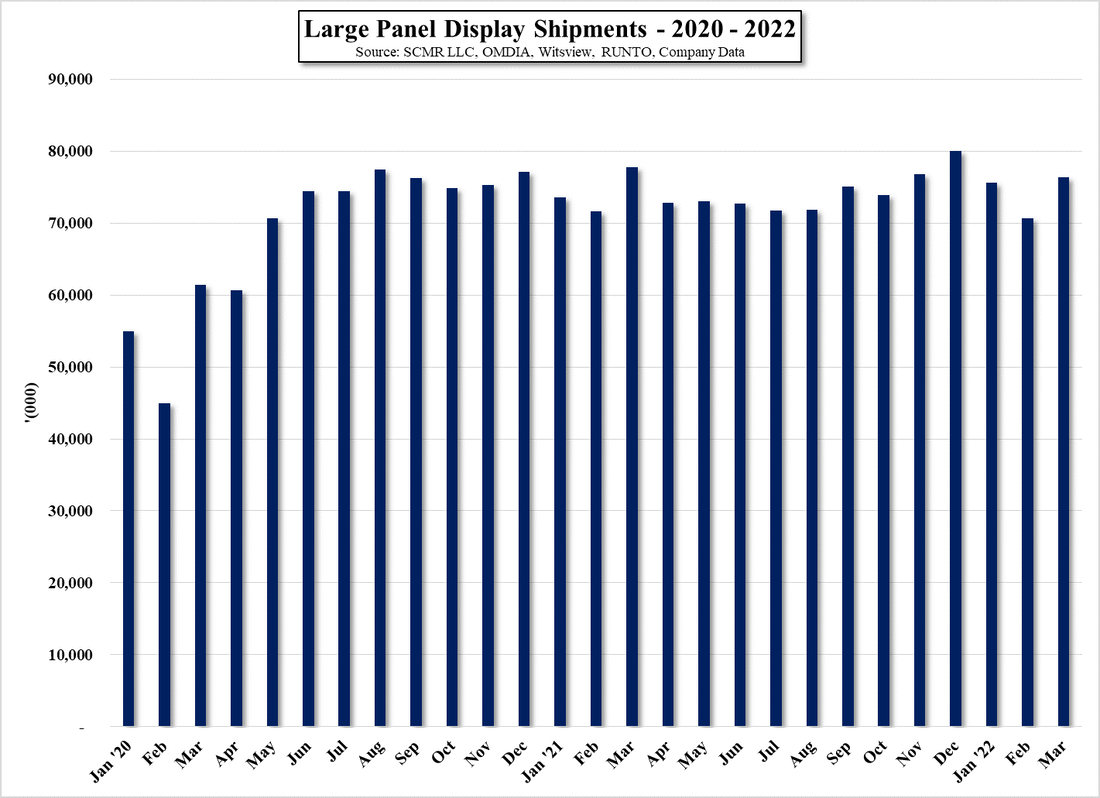

Normally, when we look at monthly display panel sales, they are ~5 weeks old[1] and represent the totals for the previous month. While we do the same this month, it seems a long time has passed since March, making those metrics seemingly less relevant. As CE brands spent much of March pulling forward production and shipments to beat the Trump ‘Liberation Day’ deadline, it is difficult to look at the data the same way it is normally used. That said, large panel shipments were ~73m units, up 11.1% m/m and up 6.0% y/y, while total shipments were 5.1% above the typical (5-year) March shipment average. This put the quarterly shipment total at 202.3m units, 6.2% above typical, indicating that the quarter (Jan/Feb) was already about 1% above average.

In terms of sales, total large panel sales for March were ~$6.24b, up 12.7% m/m, but down 6.4% y/y, while on a YTD basis, sales were up 4.5% y/y. Among those panel manufacturers that are primary large panel producers, the biggest gainers in March were both South Korean producers, Samsung Display (pvt) and LG Display (LPL), up 57.9% m/m and 34.8% m/m respectively. This implies that while both South Korean panel producers accounted for only 21.5% of total panel revenue for March, they accounted for ~38% of March large panel sales growth. SDC feeds parent Samsung Electronics (005930.KS) QD/OLED TV set and OLED monitor line, and, as much of the Samsung’s TV line is assembled in Mexico before shipping to the US, we expect these were rush orders to beat the early April deadline. LG is basically the same in the TV space.

Now that the deadline has been pushed out until July, we expect April large panel shipments will better reflect actual demand and inventory levels but given the capricious nature of comments from the President and White House, it is still difficult to predict what path consumers and CE companies will take in the short-term. At our gut level, we feel that as negotiations with potentially heavily tariffed countries continue, the WH spin will be positive and while the reality of the outcomes is questionable at best, consumer sentiment on trade will improve through May and early June. That said, the offset will be increasing prices of both components and CE products as old inventory is sold, and higher tariffed goods take their place. This leaves us, once again, in a net neutral position for the next month (May) and a slight negative bias for the CE space in 2H thus far, as consumer pre-tariff buys and higher prices weaken typical holiday demand.

[1] 2 weeks from previous quarter mid-point and 3 weeks into following quarter.

In terms of sales, total large panel sales for March were ~$6.24b, up 12.7% m/m, but down 6.4% y/y, while on a YTD basis, sales were up 4.5% y/y. Among those panel manufacturers that are primary large panel producers, the biggest gainers in March were both South Korean producers, Samsung Display (pvt) and LG Display (LPL), up 57.9% m/m and 34.8% m/m respectively. This implies that while both South Korean panel producers accounted for only 21.5% of total panel revenue for March, they accounted for ~38% of March large panel sales growth. SDC feeds parent Samsung Electronics (005930.KS) QD/OLED TV set and OLED monitor line, and, as much of the Samsung’s TV line is assembled in Mexico before shipping to the US, we expect these were rush orders to beat the early April deadline. LG is basically the same in the TV space.

Now that the deadline has been pushed out until July, we expect April large panel shipments will better reflect actual demand and inventory levels but given the capricious nature of comments from the President and White House, it is still difficult to predict what path consumers and CE companies will take in the short-term. At our gut level, we feel that as negotiations with potentially heavily tariffed countries continue, the WH spin will be positive and while the reality of the outcomes is questionable at best, consumer sentiment on trade will improve through May and early June. That said, the offset will be increasing prices of both components and CE products as old inventory is sold, and higher tariffed goods take their place. This leaves us, once again, in a net neutral position for the next month (May) and a slight negative bias for the CE space in 2H thus far, as consumer pre-tariff buys and higher prices weaken typical holiday demand.

[1] 2 weeks from previous quarter mid-point and 3 weeks into following quarter.

Large Panel LCD Industry Sales - 2020 - 2025 YTD - Source: SCMR LLC, OMDIA, Witsview, IHS, Company Data

RSS Feed

RSS Feed