Fun With Data – 5G 2021

The Global Mobile Suppliers Association is a trade organization that promotes the use of 3GPP (3rd Generation Partnership Project) standard protocols for mobile telecommunications. Such standards cover those related to 2G, 3G, 4G (LTE) and 5G and the organizations executive members include Apple (AAPL), Ericsson (ERIC), Intel (INTC) Qualcomm (QCOM), Huawei (pvt), Samsung (005930.KS), Nokia (NOK), and ZTE (000063.CH) along with thousands of members and the association also amasses global data on a variety of topics related to the current state of mobile communication. Based on that accumulated data we have put together a sort of 5G year-end summary that points toward the state of 5G today.

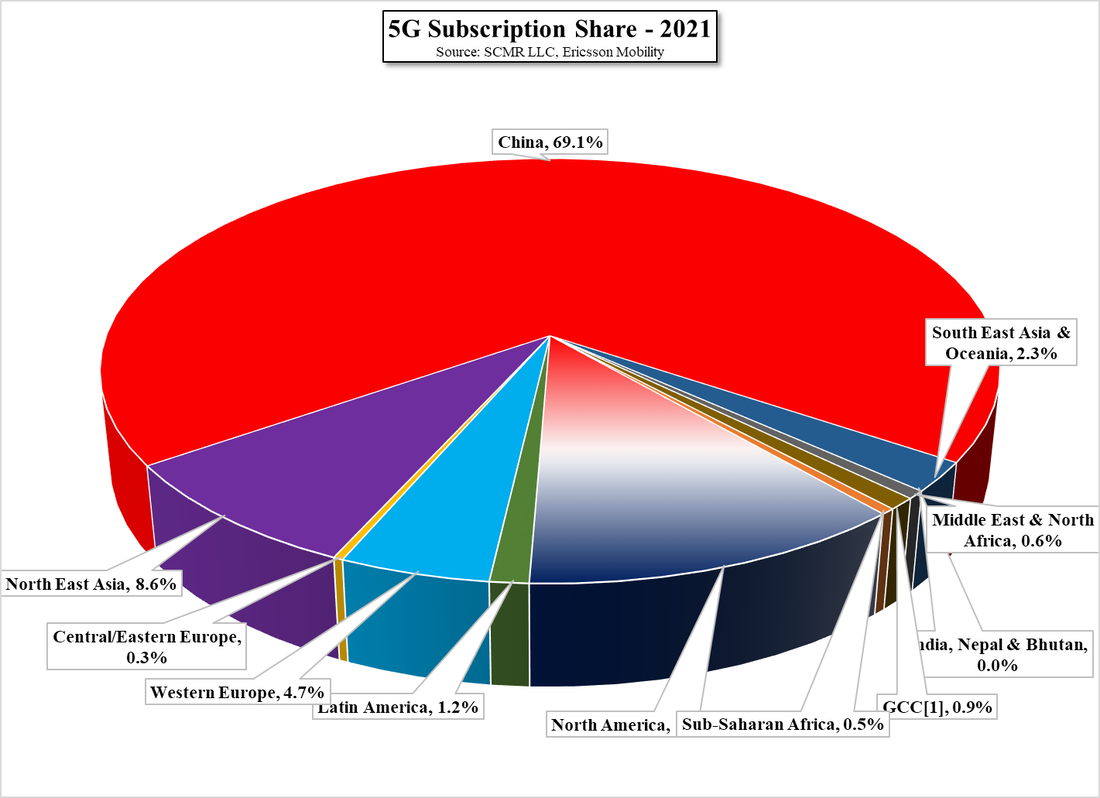

- 481 operators in 144 countries/territories have invested in 5G to date. That is up 16.7% y/y.

- Of those 481 operators, 189 in 74 countries have launched one or more 5G services, up 40% y/y.

- There are 81 operators offering residential or business 5G FWA (Fixed Wireless Access) services, up 84% y/y.

- 32% of FWA service providers offer speed-only based rates, while 36% offer volume-only based fees, with 9% offering both plans.

- FWA quoted speeds range from 50Mbps to 4.2Gbps, with just over half between 250Mbps and 1.0 Gbps.

- 207 5G FWA CPE (Customer Premise Equipment) devices have been announced (up 92% y/y) with 61.8% for indoor use.

- Private network deployments (664 total) are primarily LTE, but currently 5G private networks hold a 20% share, with combined 4G/5G adding another 5%.

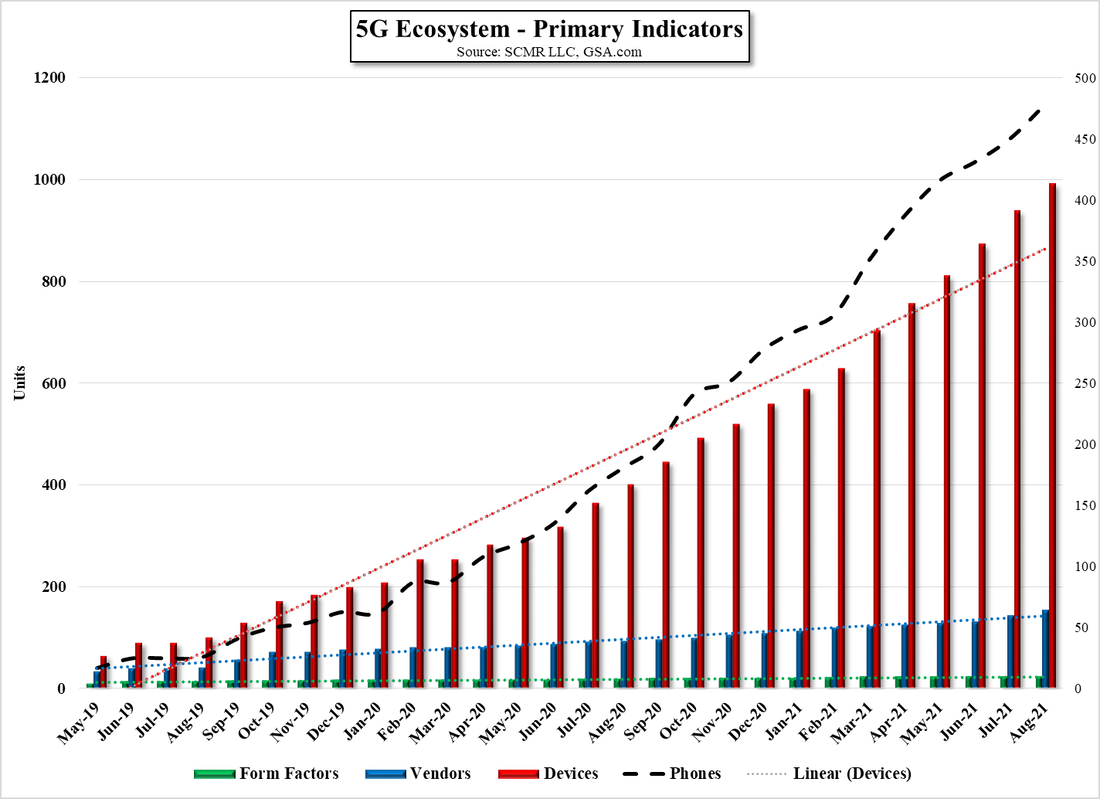

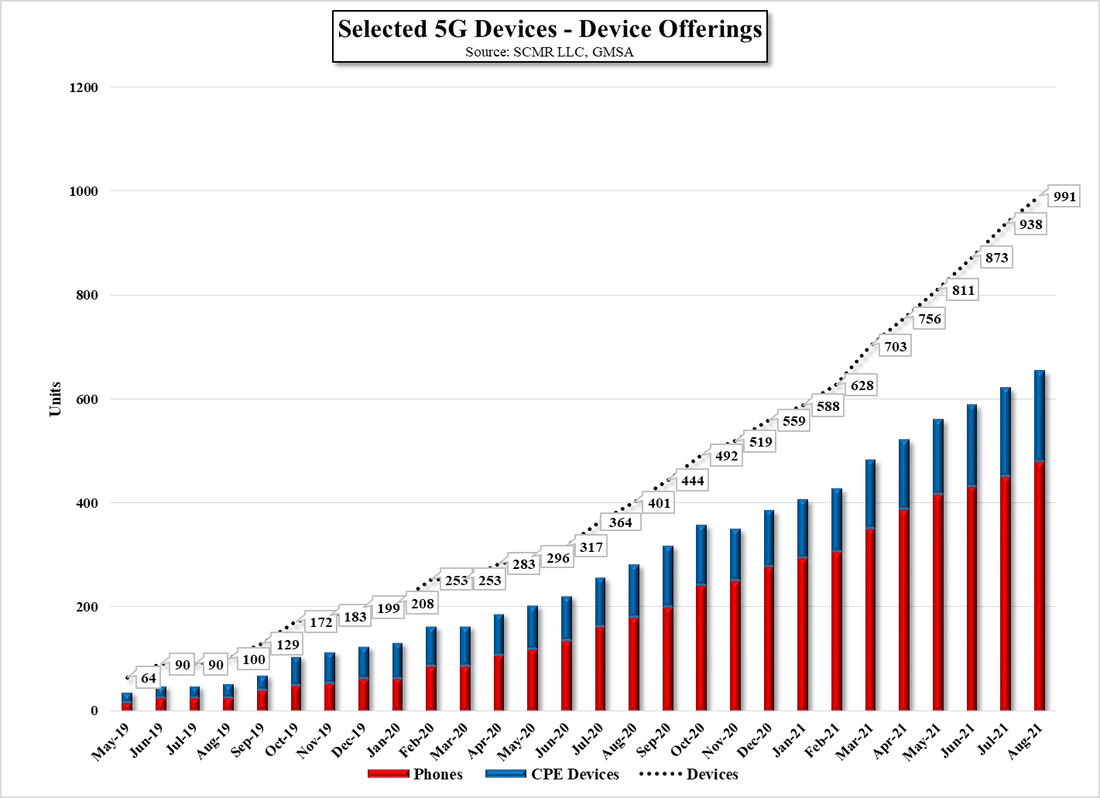

- The total count of announced 5G devices is now over 1,200 with 832 commercial devices

- 5G form factors continue to increase (22 currently), with phones making up the largest share (~50%) (See Fig. 1)

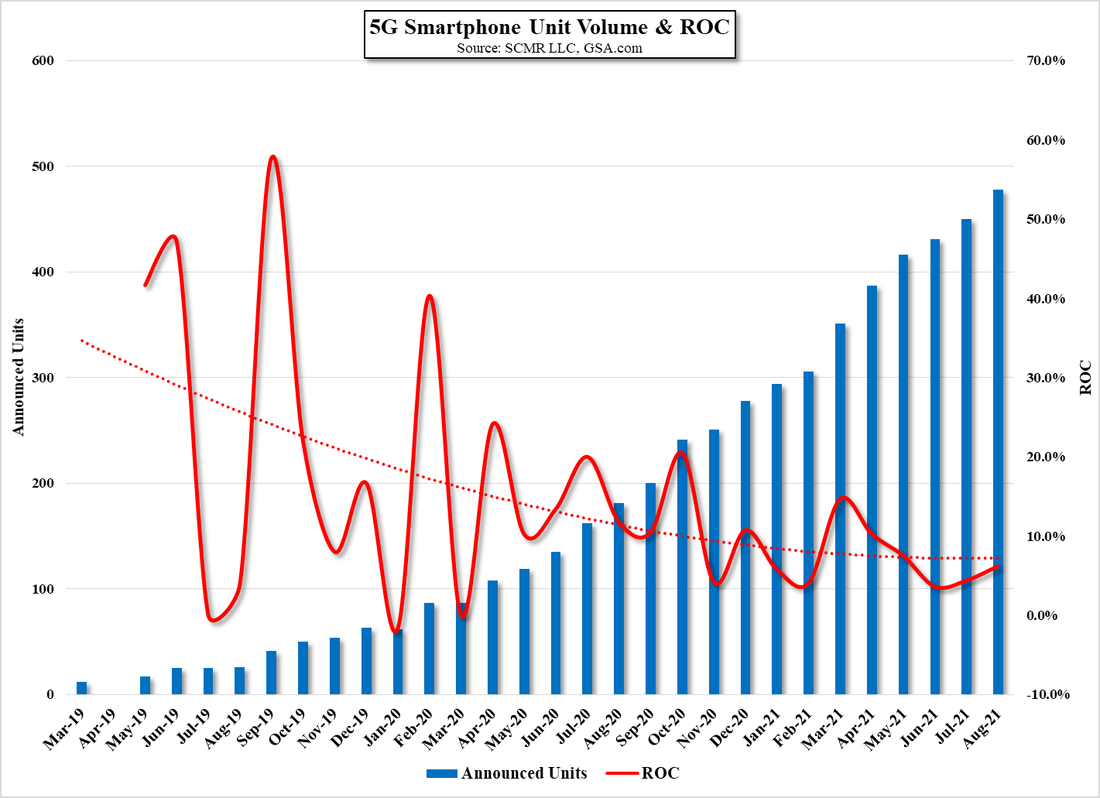

- 596 5G phone models have been announced with 530 commercially available from 40 vendors, with 8 additional vendors with announced models.

- There are 5 suppliers of 5G chipsets and 47 commercially available 5G mobile processors/platforms (up 88% y/y) and 17 commercially available 5G modems, up 70% y/y.

- 55 5G Chipsets support sub-6 GHz spectrum (60.4%), while 36 support mmWave (39.6%)

- 82.1% of all announced 5G devices support sub-6 while 12.4% of announced devices support mmWave.

5G Device Type Share - 12 Months - Source: SCMR LLC, GSA

Top 10 5G Ecosystem Supplier Share by Devices - Source: SCMR LLC, GSA

RSS Feed

RSS Feed