LG to Introduce Ultra-large OLED TV

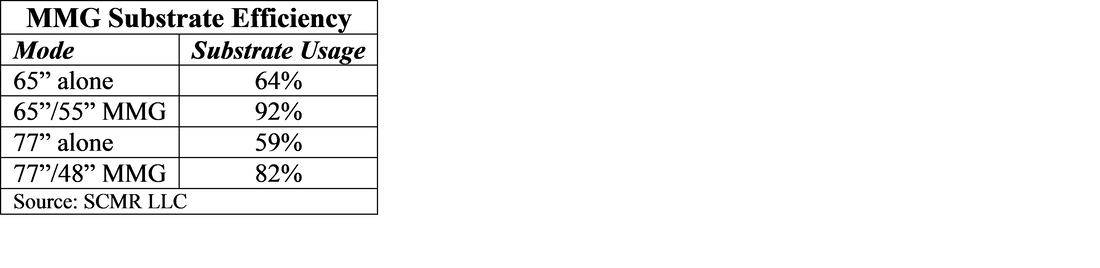

LG Electronics (066570.KS) is expected to introduce a 97” OLED TV at CES in January. This will be LG’s largest OLED TV size, with the maximum currently an 88” 8K model (OLED88ZXPUA) priced at $30,000, although availability is quite limited and delivery times are between 6 and 8 weeks for most retailers. Such large OLED TVs are not produced in large quantities, with less than 2% of LG Display’s (LPL) production being for such large panel sizes, however two 98” OLED TV panels can be cut from a Gen 8.5 substrate with substrate efficiency close to 100%, which makes them viable for OLED lines that are not producing MMG product that mixes both large and smaller OLED panels on the same substrate., a slower process. The price for the 98” TV model remains unknown, but based on the price of smaller sets, it will likely be in the $35,000 to $45,000 range.

LG is not only competing with Samsung’s (005930.KS) Micro-LED TVs, as we noted yesterday, but also with its own micro-LED TV brand, so despite the high price, it is necessary for LG to offer such large size OLED models, which, while certainly expensive compared to smaller OLED TV models, are less expensive than the micro-LED offerings by both vendors. While few consumers can afford the high price tag, such large OLED TVs can be used in commercial settings where the high contrast and color quality are essential to product presentation. Save those pennies.

LG is not only competing with Samsung’s (005930.KS) Micro-LED TVs, as we noted yesterday, but also with its own micro-LED TV brand, so despite the high price, it is necessary for LG to offer such large size OLED models, which, while certainly expensive compared to smaller OLED TV models, are less expensive than the micro-LED offerings by both vendors. While few consumers can afford the high price tag, such large OLED TVs can be used in commercial settings where the high contrast and color quality are essential to product presentation. Save those pennies.

RSS Feed

RSS Feed