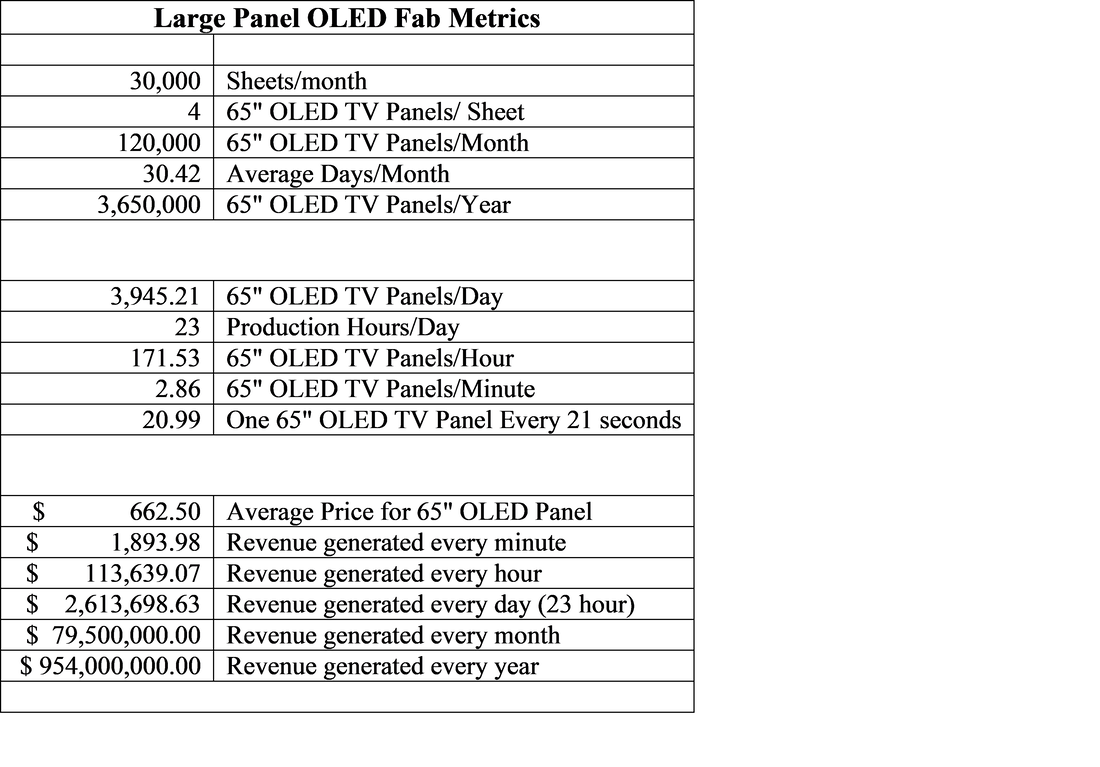

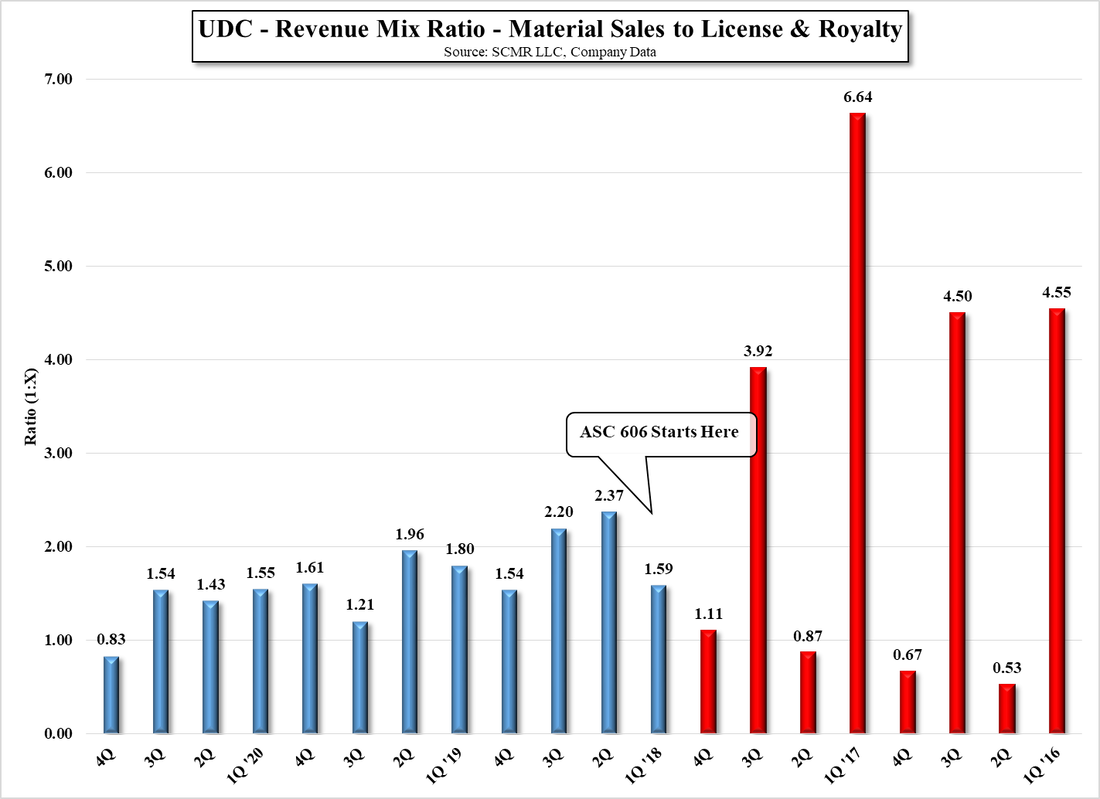

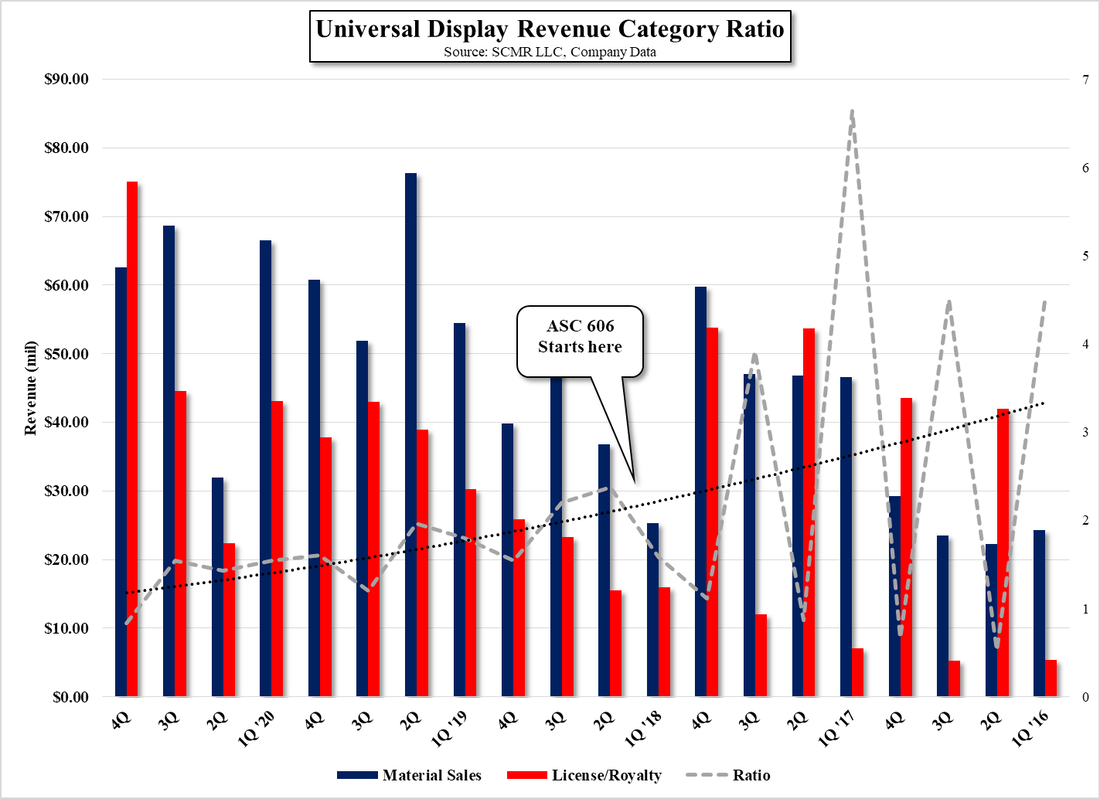

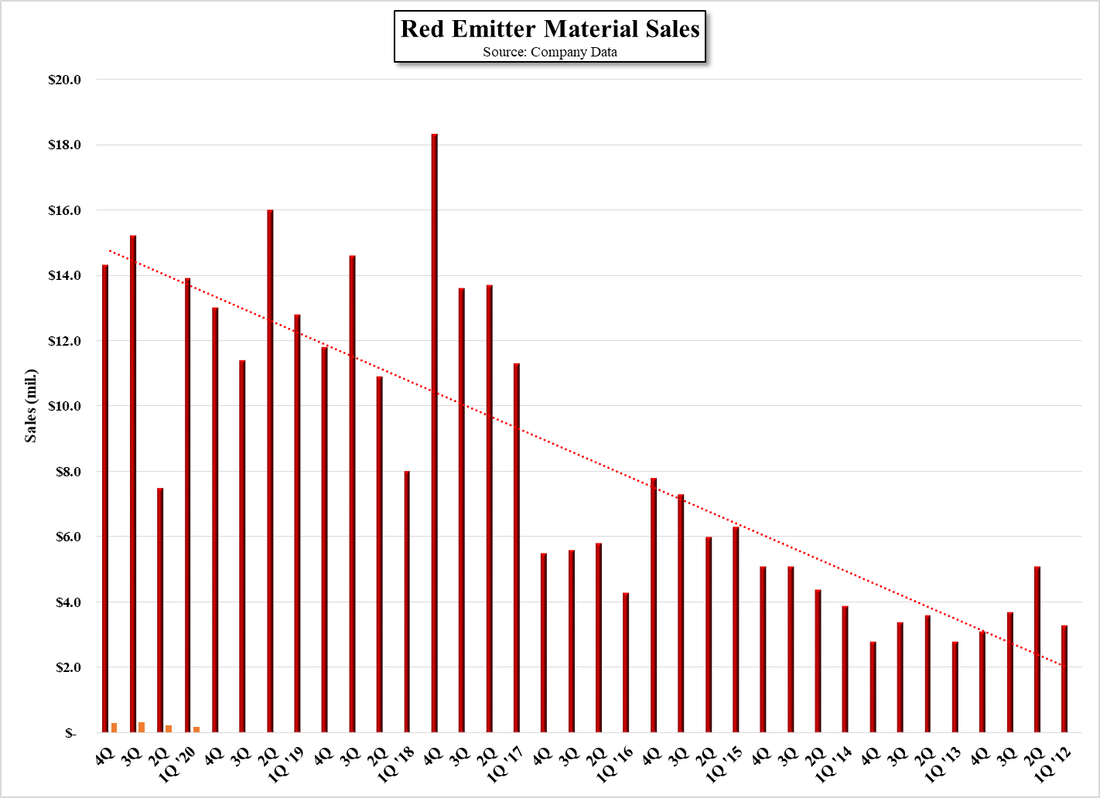

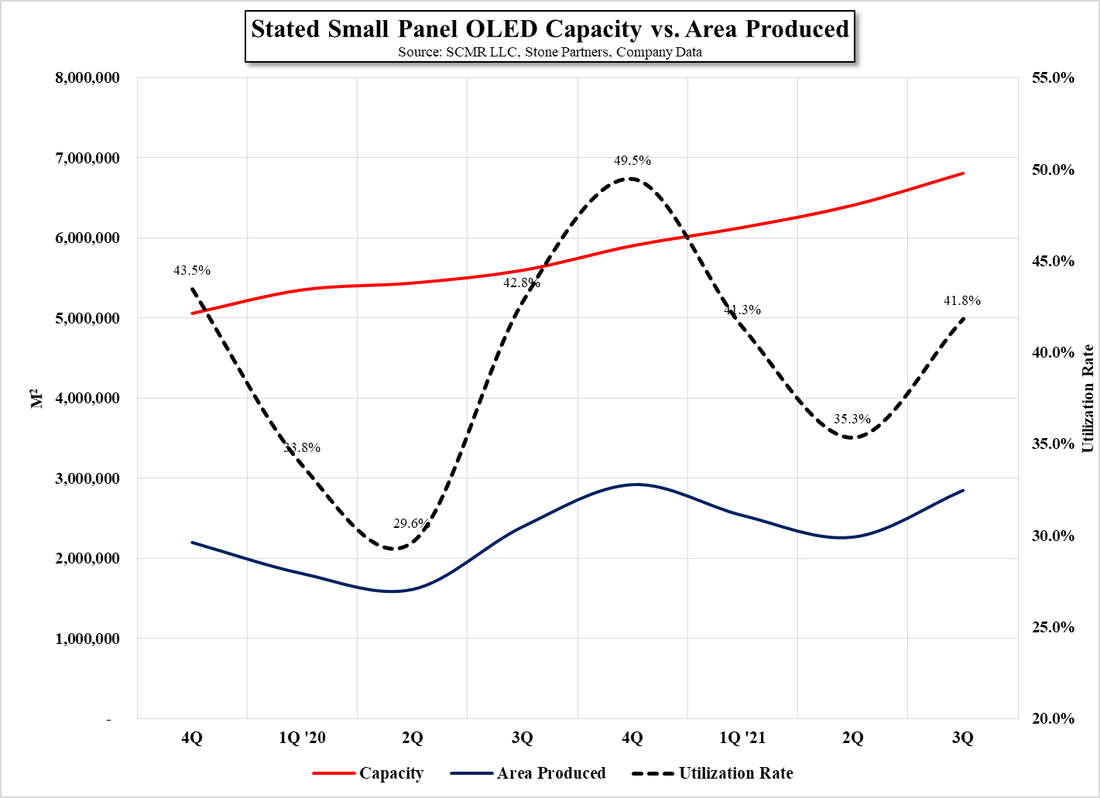

Japan Display Goes Litho…

Photolithography is the platform on which the semiconductor industry is built. The concept of photolithography etch is fundamental to almost all semiconductor production and is the most common way in which structures at the micron level are formed. In the display space however, photolithography is used in the formation of the TFT (thin-film) electronics that control display pixels, but the pixels themselves, at least in OLED displays, are formed using the deposition of OLED materials through CVD (Chemical Vapor Deposition) tools that vaporize the OLED materials and deposit them through fine metal masks, essentially screens that form red, green, and blue sub-pixels that generate the millions of color combinations needed for full color displays.

There are problems with OLED material deposition, one of which is the masks themselves. They are made of INVAR, a nickel-iron alloy that is able to maintain shape and uniformity under the temperature conditions used in CVD (up to 500⁰C) but at the same time must be unusually thin and placed extremely close to the substrate to create precise sub-pixel placement. The requisite thinness limits the size of these masks, as they begin to sag above Gen 6 substrate size, and the buildup of material on the mask surface requires they be cleaned and replaced regularly, pushing OLED display producers to look for alternative deposition methods.

One promising technique is ink-jet printing where multiple nozzles place OLED material droplets on the substrate as they move across its length. This allows for precise control over the materials, resulting in a substantial reduction in the amount of OLED emitter material waste but in order for the material to pass through the nozzles, it must be put into solution which means mixing the emitter materials with a solvent which can change the characteristics of the OLED materials or require ‘soluble’ materials that are different from those used in CVD deposition.

There are problems with OLED material deposition, one of which is the masks themselves. They are made of INVAR, a nickel-iron alloy that is able to maintain shape and uniformity under the temperature conditions used in CVD (up to 500⁰C) but at the same time must be unusually thin and placed extremely close to the substrate to create precise sub-pixel placement. The requisite thinness limits the size of these masks, as they begin to sag above Gen 6 substrate size, and the buildup of material on the mask surface requires they be cleaned and replaced regularly, pushing OLED display producers to look for alternative deposition methods.

One promising technique is ink-jet printing where multiple nozzles place OLED material droplets on the substrate as they move across its length. This allows for precise control over the materials, resulting in a substantial reduction in the amount of OLED emitter material waste but in order for the material to pass through the nozzles, it must be put into solution which means mixing the emitter materials with a solvent which can change the characteristics of the OLED materials or require ‘soluble’ materials that are different from those used in CVD deposition.

Fine Metal Mask - Distance distortion - Source: Decker, Wolfgang & Belan, Rob & Heydemann, Volker & Armstrong, Sean & Fisher, Tim. (2016). Novel Low Pressure Sputtering Source and Improved Vacuum Deposition of Small Patterned Features Using Precision

AR/VR displays require very high resolution displays in order to keep the optic system from becoming confused about what it is seeing (similar to motion sickness) and such displays require pixel densities far above the 400 to 500 pixels/inch we see in current smartphones, but both CVD deposition and ink-jet printing fall short of these densities, pushing OLED display producers to look for other alternatives to boost their ability to create high density pixel displays and that is where the aforementioned photolithography comes in. Japan Display (6740.JP) has announced that it will be starting to sample displays to customers this year that are based on ‘maskless’ lithography based material patterning.

JDI’s eLEAP (environmental positive Lithography with maskless deposition Extreme long life, low power, and high luminance Any shape Patterning) is claimed to increase emission efficiency by 60%, which is more than 2 times that of the FMM method and is not limited to Gen 6 substrates. The process is green in that it is more ‘environmentally positive’ without masks that need to be regularly cleaned and therefore uses less toxic material and produces less CO2 emissions. JDI is combining this technology with its expertise in IGZO TFT backplanes to create what it calls a breakthrough in display technology.

While we cannot verify many of JDI’s claims, there are some points that are do make sense. We expect that the JDI system involves the use of supercritical Carbon Dioxide, which is a form of ‘dry ice’ that is low-cost, non-flammable, and can be used as a developing solvent that does not degrade OLED materials, which are critically sensitive to water, air, and many of the solvents used in lithography, and possibly fluorinated solvents that have less onerous characteristics toward organic (OLED) materials. Since lithographic patterning is only limited by the size and shape of the substrate, almost any shape display could be patterned in theory, and given that no metal masks are used, three of the claims are possible.

JDI’s eLEAP (environmental positive Lithography with maskless deposition Extreme long life, low power, and high luminance Any shape Patterning) is claimed to increase emission efficiency by 60%, which is more than 2 times that of the FMM method and is not limited to Gen 6 substrates. The process is green in that it is more ‘environmentally positive’ without masks that need to be regularly cleaned and therefore uses less toxic material and produces less CO2 emissions. JDI is combining this technology with its expertise in IGZO TFT backplanes to create what it calls a breakthrough in display technology.

While we cannot verify many of JDI’s claims, there are some points that are do make sense. We expect that the JDI system involves the use of supercritical Carbon Dioxide, which is a form of ‘dry ice’ that is low-cost, non-flammable, and can be used as a developing solvent that does not degrade OLED materials, which are critically sensitive to water, air, and many of the solvents used in lithography, and possibly fluorinated solvents that have less onerous characteristics toward organic (OLED) materials. Since lithographic patterning is only limited by the size and shape of the substrate, almost any shape display could be patterned in theory, and given that no metal masks are used, three of the claims are possible.

SCO2 Patterning - Source: HA Soo Hwang, Alexander Zakhidov et al, Department of Material Science & Engineering, Department of Chemistry, Cornell University, Ithaca, NY

The one area that cannot be verified is, ‘Extreme long life, low power, and high luminance’. JDI claims a lifetime improvement of greater than 3X over conventional deposition based OLED displays (see Figure 3) and a 2X improvement in Peak brightness. We can understand the low power portion as JDI is pairing eLEAP technology with its expertise in IGZO backplanes, which have lower power demands than other backplane technologies, and the claim of higher luminance (subjectively ‘brightness’) seems to be based on the technology’s ability to increase the size of RGB sub-pixels by placing them closer together in each pixel, but neither have been verified, so these claims need to be verified.

Japan Display eLeap Lifetime Comparison - Source: Japan Display

Japan Display eLEAP pixel view - Source: Japan Display

There have been a a number of smaller companies that have been researching using photolithography for OLED deposition, in particular IMEC (pvt) and Orthogonal (pvt), a Cornell spin-off, but JDI would be the first to commercialize the process if it is successful in creating customer demand, particularly from AR/VR display buyers who are always looking to increase resolution without excessive cost. We expect it will take some time for JDI to develop its eLEAP technology to the point where a full scale production line could be built, but given the mature nature of photolithographic tools, and the use of same for the TFT side of the display business, it is certainly a possibility from an infrastructure POV and one that has less limitations than current processes. Given JDI’s on and off relationship with Apple (AAPL), there has been speculation that the ‘significant customer interest’ JDI mentions in its press release is coming from Apple, but we hesitate to make such conclusions. All in it would be a very important step for JDI if they were able to commercialize this technology, giving them an advantage in the high resolution display market, but we expect the timeline for a viable commercial product is still some time away.

RSS Feed

RSS Feed