If You Build it They Will Come, or Will They?

As we have noted, Samsung Display (pvt), LG Display (LPL) and most recently China’s BOE (200725.CH) have been working toward developing the technology necessary to produce IT OLED panels on larger substrates, moving from Gen 6 sheets, which are 2.78 m2 to Gen 8.5 sheets, which are 5.5 m2 to increase the efficiency of the process. Recently is seems that other OLED producers are also looking to make such a change, although we believe the motivation and potential for success are different from those producers mentioned above. Visionox (002387.CH) has been the name most often mentioned as a potential developer of such technology, although we have our doubts as to whether such stories are anything more than self-promotion.

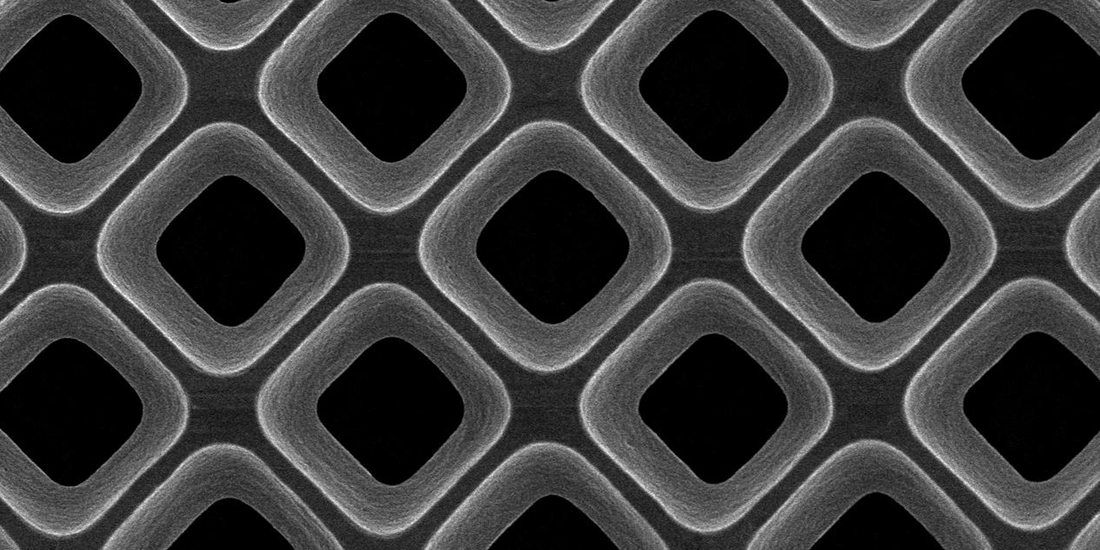

As OLED display technology migrates to larger devices, OLED deposition technology comes up against some roadblocks, the largest of which is the use of fine metal masks that force gaseous OLED materials to form the pattern on substrates that become pixels on a display. These masks are made of a nickel/iron alloy that is able to remain stable under the heat and high and low pressures found in OLED deposition equipment, as it is absolutely necessary that the FMM ‘screens’ keep the OLED materials in perfect order and spacing during production. While the FMM are designed to handle heat and pressure they must also react to gravity, which can cause them to sag and misplace pixels, causing a panel to fail. While this is not a problem for small OLED displays, such as those used in watches and smartphones, as the displays and masks get larger, such as might be the case for notebook or monitor panels, the effects of gravity get worse and yield management becomes more difficult.

Currently the number of OLED displays produced for IT products is relatively small when compared to smartphone production, but that is expected to change over the next few years with OLED adoption increasing for such products, which makes solving the production issues with larger OLED panels all the more important. It is especially important to SDC, LGD, and BOE, all of whom are OLED display suppliers to Apple (AAPL), who is expected to continue to migrate more display based products to OLED. Each of the three has been working toward find solutions that will improve OLED IT panel yields, each with their own ‘slant’ to the problems, but with each knowing that they have the ‘ear’ of Apple as they progress. Visionox however is not a supplier of flexible OLED panels to Apple, with Chinese brand Honor (pvt) their biggest OLED display customer, along with Xiaomi (1810.HK) for whom they produce OLED watch displays.

To give some perspective in 2021, Honor purchased ~24m OLED panels, and while that might sound like a large quantity, it represents ~3.9% of the OLED display market (unit volume), and while Xiaomi has a larger share (~13.9%) given the size of OLED watch displays relative to smartphones or OLED IT panels, it represents only a small amount of small panel OLED industry capacity. Apple however purchased ~184m OLED displays last year, most of which went toward iPhone production, giving them a ~29.6% share of the overall small panel OLED market, which is why the three mentioned above are working so hard to solve OLED IT production issues, especially under the assumption that Apple will continue to expand OLED penetration among its IT products. While all three OLED producers are taking R&D risk and potentially large capital risk, the goal of becoming a primary supplier of small panel IT OLED products to Apple is in their headlights.

That said, it is not the same for Visionox, who would have to get qualified as a primary small panel OLED supplier at Apple before they would even have a shot at competing with SDC, LGD, or BOE for Apple’s incremental OLED IT business, so why would they circulate such stories? Industry folk, and we certainly can see their point, infer that it is to garner support from the Chinese government in the form of subsidies. Much of the early construction costs and operating expenses for panel producers in China are paid for through provincial or city-based subsidies that can defray construction costs that might normally be prohibitive, allowing Chinese producers to grow more quickly than non-subsidized producers, and during the early years of operation, those subsidies can offset low yields and low utilization rates for Chinese fabs. As China has already become the capacity leader in LCD panel production, government organizations are want to give subsidies for such capacity, but a challenge to incumbent OLED leaders like SDC and LGD can still garner local government financial support, giving Visionox the hope that by dangling the idea of building out capacity to challenge others for Apple’s OLED IT business, they might set the wheels in motion for potential government help.

Visionox is said to be testing the OLED IT waters at its V3 Gen 6 fab in Hefei to work through production issues, and then would build a new Gen 8.5 OLED line in another location. The V3 fab is being built in two phases with “the 2nd phase promoted in a timely manner” according to the company late last year. Perhaps additional financial support is being hinted at for the phase 2 construction and equipment, which we had expected to be completed later this year, although not oriented to IT panel production. If Visionox is able to solve the necessary IT OLED production issues on the V3 phase 1 line, it would encourage funding sources to push forward with phase 2 and potentially add a new Gen 8.5 fab designed specifically for IT OLED panels. By indicating that there was potential for a new Gen 8.5 OLED fab to be built, the company can begin selling the idea to city leaders in other locations to see if funding is available and hopefully create a bidding war, similar to what occurred when Samsung was looking for a new silicon fab location in the US.

There is a lot of speculation here, but certainly not any that has not been seen by us over the years in the display space, so while we don’t like to speculate, the Visionox story has many similarities to others we have heard over the years, and feels as if we have been to this rodeo before. We could be wrong, with Visionox much further along with Apple or the technology needed for IT OLED production, but we are less sanguine about the idea knowing that Visionox only grew their share of the small panel OLED market from 4.7% in 2020 to 4.9% in 2021, while Samsung Display and LG Display’s real competitor BOE grew its share from 7.3% in 2020 to 10.0% last year, which amounted to a 66.9% increase in unit volume y/y. Without a very dedicated customer base already established, we expect it will be necessary for Visionox to win a few more games before they build ‘it’, especially knowing who ‘they’ are.

As OLED display technology migrates to larger devices, OLED deposition technology comes up against some roadblocks, the largest of which is the use of fine metal masks that force gaseous OLED materials to form the pattern on substrates that become pixels on a display. These masks are made of a nickel/iron alloy that is able to remain stable under the heat and high and low pressures found in OLED deposition equipment, as it is absolutely necessary that the FMM ‘screens’ keep the OLED materials in perfect order and spacing during production. While the FMM are designed to handle heat and pressure they must also react to gravity, which can cause them to sag and misplace pixels, causing a panel to fail. While this is not a problem for small OLED displays, such as those used in watches and smartphones, as the displays and masks get larger, such as might be the case for notebook or monitor panels, the effects of gravity get worse and yield management becomes more difficult.

Currently the number of OLED displays produced for IT products is relatively small when compared to smartphone production, but that is expected to change over the next few years with OLED adoption increasing for such products, which makes solving the production issues with larger OLED panels all the more important. It is especially important to SDC, LGD, and BOE, all of whom are OLED display suppliers to Apple (AAPL), who is expected to continue to migrate more display based products to OLED. Each of the three has been working toward find solutions that will improve OLED IT panel yields, each with their own ‘slant’ to the problems, but with each knowing that they have the ‘ear’ of Apple as they progress. Visionox however is not a supplier of flexible OLED panels to Apple, with Chinese brand Honor (pvt) their biggest OLED display customer, along with Xiaomi (1810.HK) for whom they produce OLED watch displays.

To give some perspective in 2021, Honor purchased ~24m OLED panels, and while that might sound like a large quantity, it represents ~3.9% of the OLED display market (unit volume), and while Xiaomi has a larger share (~13.9%) given the size of OLED watch displays relative to smartphones or OLED IT panels, it represents only a small amount of small panel OLED industry capacity. Apple however purchased ~184m OLED displays last year, most of which went toward iPhone production, giving them a ~29.6% share of the overall small panel OLED market, which is why the three mentioned above are working so hard to solve OLED IT production issues, especially under the assumption that Apple will continue to expand OLED penetration among its IT products. While all three OLED producers are taking R&D risk and potentially large capital risk, the goal of becoming a primary supplier of small panel IT OLED products to Apple is in their headlights.

That said, it is not the same for Visionox, who would have to get qualified as a primary small panel OLED supplier at Apple before they would even have a shot at competing with SDC, LGD, or BOE for Apple’s incremental OLED IT business, so why would they circulate such stories? Industry folk, and we certainly can see their point, infer that it is to garner support from the Chinese government in the form of subsidies. Much of the early construction costs and operating expenses for panel producers in China are paid for through provincial or city-based subsidies that can defray construction costs that might normally be prohibitive, allowing Chinese producers to grow more quickly than non-subsidized producers, and during the early years of operation, those subsidies can offset low yields and low utilization rates for Chinese fabs. As China has already become the capacity leader in LCD panel production, government organizations are want to give subsidies for such capacity, but a challenge to incumbent OLED leaders like SDC and LGD can still garner local government financial support, giving Visionox the hope that by dangling the idea of building out capacity to challenge others for Apple’s OLED IT business, they might set the wheels in motion for potential government help.

Visionox is said to be testing the OLED IT waters at its V3 Gen 6 fab in Hefei to work through production issues, and then would build a new Gen 8.5 OLED line in another location. The V3 fab is being built in two phases with “the 2nd phase promoted in a timely manner” according to the company late last year. Perhaps additional financial support is being hinted at for the phase 2 construction and equipment, which we had expected to be completed later this year, although not oriented to IT panel production. If Visionox is able to solve the necessary IT OLED production issues on the V3 phase 1 line, it would encourage funding sources to push forward with phase 2 and potentially add a new Gen 8.5 fab designed specifically for IT OLED panels. By indicating that there was potential for a new Gen 8.5 OLED fab to be built, the company can begin selling the idea to city leaders in other locations to see if funding is available and hopefully create a bidding war, similar to what occurred when Samsung was looking for a new silicon fab location in the US.

There is a lot of speculation here, but certainly not any that has not been seen by us over the years in the display space, so while we don’t like to speculate, the Visionox story has many similarities to others we have heard over the years, and feels as if we have been to this rodeo before. We could be wrong, with Visionox much further along with Apple or the technology needed for IT OLED production, but we are less sanguine about the idea knowing that Visionox only grew their share of the small panel OLED market from 4.7% in 2020 to 4.9% in 2021, while Samsung Display and LG Display’s real competitor BOE grew its share from 7.3% in 2020 to 10.0% last year, which amounted to a 66.9% increase in unit volume y/y. Without a very dedicated customer base already established, we expect it will be necessary for Visionox to win a few more games before they build ‘it’, especially knowing who ‘they’ are.

RSS Feed

RSS Feed