China Smartphones/5G

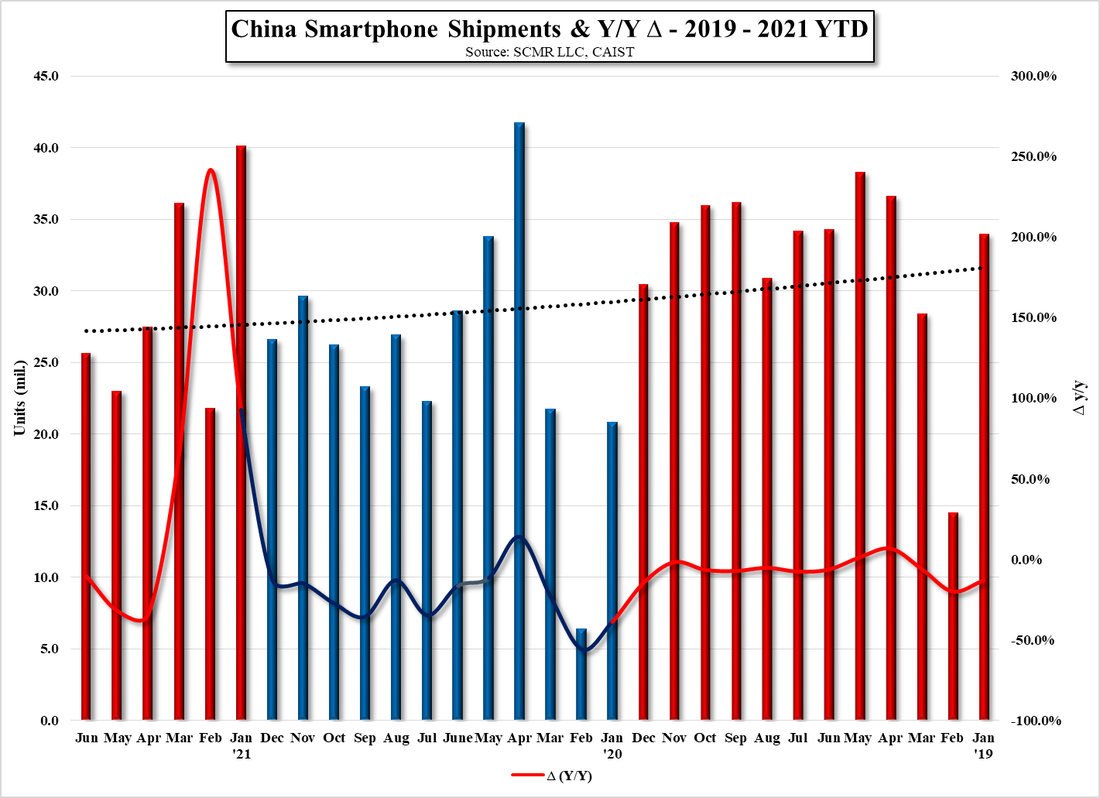

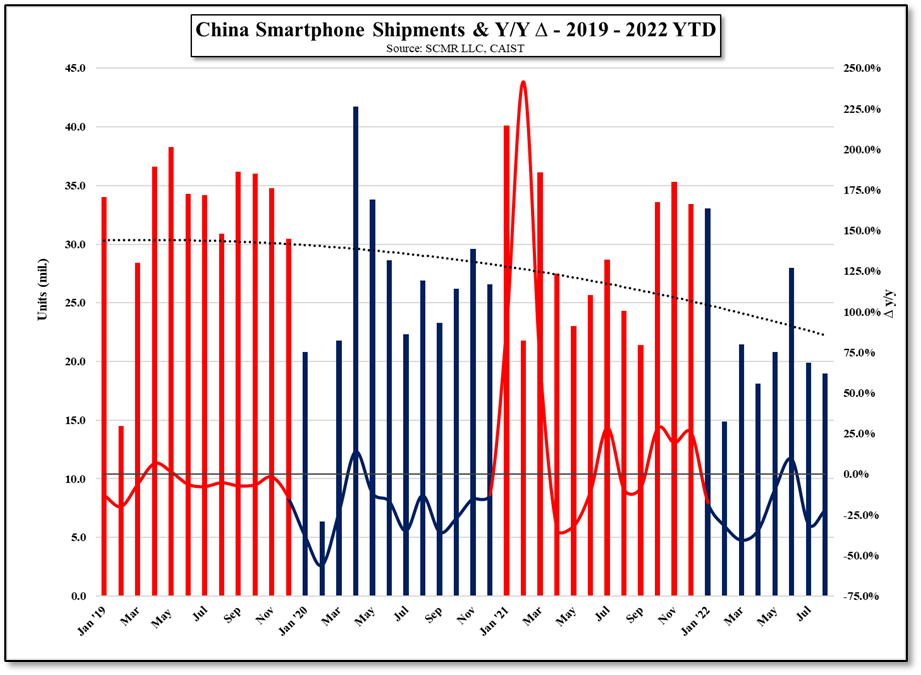

We had made a forecast for Chinese smartphone shipments for the 4th quarter and while the December numbers are not yet in, the official Chinese smartphone shipments for the last two months are 47.16m units, surprisingly 15.6% higher than our estimate, which pushes us to raise our December shipment number from 19.4m units to 22m units. If this is correct (or close), that would put the full year at 265,65m units, down 24.3% y/y, and the 4th quarter up 16.4% q/q but still down 32.0% y/y, and above our most recent 252m unit estimate. Most recently we have seen a full year tally of Chinese smartphone shipments totaling 287m units, which would imply a 44m unit shipment month in December, making it the best month this year, by 33%, so we are wanting to understand what the basis for that estimate was, given that our 11 month data is based on information provided by the Chinese government, which, if anything, leans a bit to the high side.

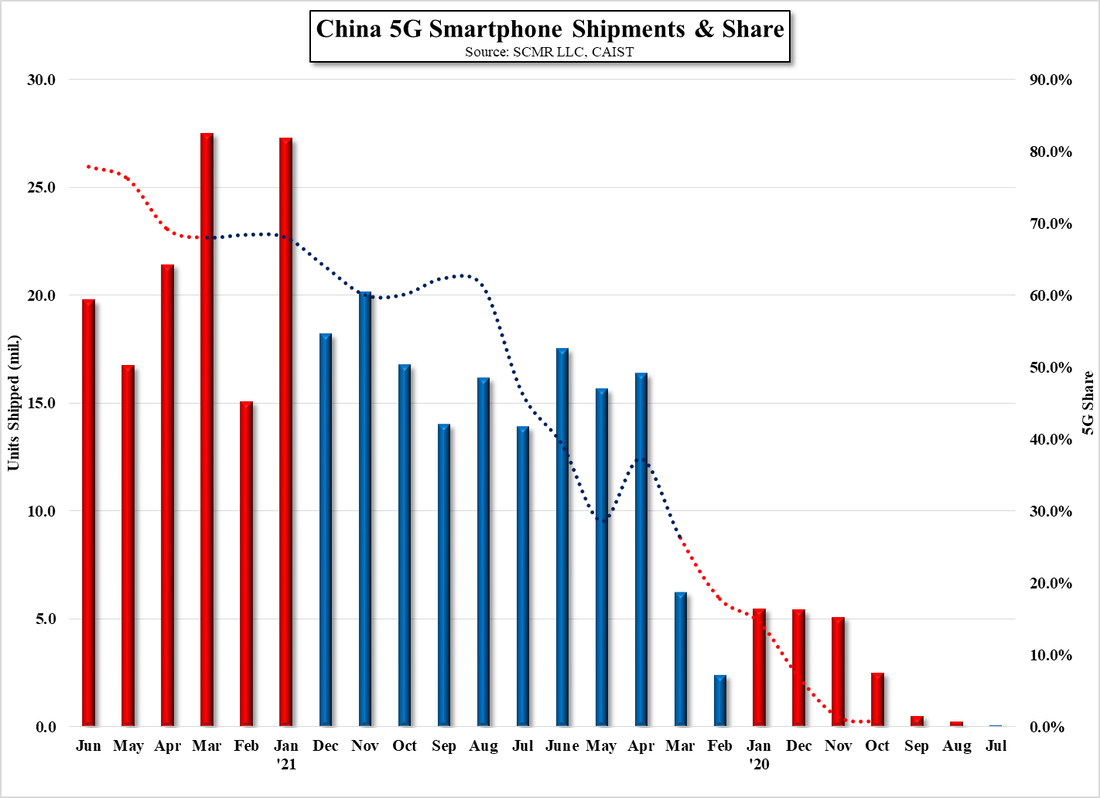

Over the last year 5G shipments in China have tracked fairly closely to overall shipments, representing between 85.1% and 72.2% of total shipments, although the spread narrowed considerably during 2H of 2022. For the full year, using a proportional 16.97m 5G units in December, we estimate 5G shipments for the full 2022 year to be 207.6m units, or 78.1% of total shipments, down 22.0% y/y, the first year 5G shipments have declined since 2019 when China began releasing such data. Given the current share, which we expect to expand a bit further this year, we expect 5G shipments in China to be a function of the overall health of the Chinese smartphone market, with far less dependency on the growth of 5G installations across the country than in previous years and more on China’s own macro environment.

Strict COVID restrictions slowed 5G deployment progress across China last year, and with many of those restrictions being lifted, deployments will likely pick-up, but we are quite skeptical as to the coverage data that the Chinese government has been promoting, and if the data in the US is any example, it bears little practicality to consumers. Typically many cities that are claimed as ‘covered’ have very spotty 5G service and while the coverage maps look well filled, the detail is far less so, with statistics used more for promotion and politics than actual consumer results.

Chinese brands continue to hold the major share of the Chinese domestic market (84.9%) and while it has deteriorated a bit over the last 4 years (86.5% last year), incursions, particularly by Apple (AAPL), have made little impact on overall domestic brand share in the Chinese smartphone market. With Samsung Electronics (005930.KS) the only major smartphone brand with a very minor share in China, we expect relatively little change unless Samsung continues to expand and market its foldable line on the Mainland, which, while facing domestic competition, seems to be considered among the most prestigious smartphone devices with Chinese consumers, along with Apple. However price sensitive buyers do have domestic foldable alternatives and there are still many pockets of nationalistic pride that would push marginal buyers to domestic brands, so for the 2023 year, we expect only a minor reduction in domestic share.

All in, it was a difficult year for CE in China, and smartphones in particular, but while we are careful to temper any enthusiasm against both a poor macro-economic situation on the Mainland, and a festering anti-China manufacturing posture for many global companies, we do take heart in that in recent months, while poor in terms of y/y performance, shipments have been, at the least, relatively stable, which we expect to continue into 1Q. The Chinese smartphone market is maturing, and with that comes slower growth and more macro affectations, which certainly seems to be the case in recent months. As that continues we expect the Chinese smartphone market to have basically the same competitive and economic characteristics of the global smartphone market and track more closely to the global markets each year. That said, Chinese brands have the advantage of lower cost, but also face some political issues, such as those in India, that can offset those cost advantages. It is up to both the Chinese government and Chinese smartphone brands as to how those issues will play out this year, and over the last year both did little to smooth those relationships that can help Chinese brands gain share outside of the Mainland. Maybe 2023 will be different, although it is still hard to be overly optimistic.

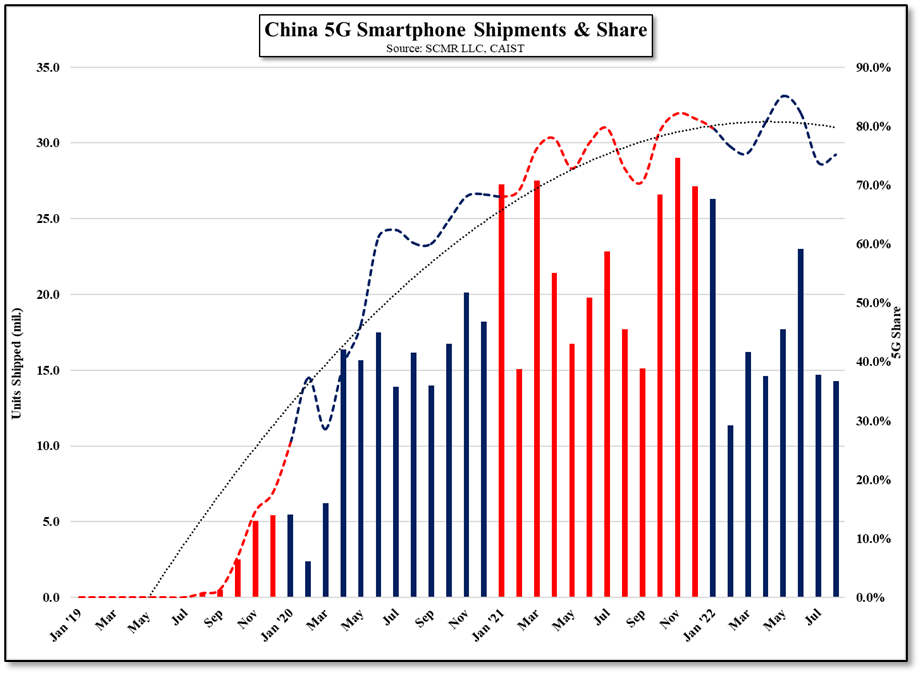

Over the last year 5G shipments in China have tracked fairly closely to overall shipments, representing between 85.1% and 72.2% of total shipments, although the spread narrowed considerably during 2H of 2022. For the full year, using a proportional 16.97m 5G units in December, we estimate 5G shipments for the full 2022 year to be 207.6m units, or 78.1% of total shipments, down 22.0% y/y, the first year 5G shipments have declined since 2019 when China began releasing such data. Given the current share, which we expect to expand a bit further this year, we expect 5G shipments in China to be a function of the overall health of the Chinese smartphone market, with far less dependency on the growth of 5G installations across the country than in previous years and more on China’s own macro environment.

Strict COVID restrictions slowed 5G deployment progress across China last year, and with many of those restrictions being lifted, deployments will likely pick-up, but we are quite skeptical as to the coverage data that the Chinese government has been promoting, and if the data in the US is any example, it bears little practicality to consumers. Typically many cities that are claimed as ‘covered’ have very spotty 5G service and while the coverage maps look well filled, the detail is far less so, with statistics used more for promotion and politics than actual consumer results.

Chinese brands continue to hold the major share of the Chinese domestic market (84.9%) and while it has deteriorated a bit over the last 4 years (86.5% last year), incursions, particularly by Apple (AAPL), have made little impact on overall domestic brand share in the Chinese smartphone market. With Samsung Electronics (005930.KS) the only major smartphone brand with a very minor share in China, we expect relatively little change unless Samsung continues to expand and market its foldable line on the Mainland, which, while facing domestic competition, seems to be considered among the most prestigious smartphone devices with Chinese consumers, along with Apple. However price sensitive buyers do have domestic foldable alternatives and there are still many pockets of nationalistic pride that would push marginal buyers to domestic brands, so for the 2023 year, we expect only a minor reduction in domestic share.

All in, it was a difficult year for CE in China, and smartphones in particular, but while we are careful to temper any enthusiasm against both a poor macro-economic situation on the Mainland, and a festering anti-China manufacturing posture for many global companies, we do take heart in that in recent months, while poor in terms of y/y performance, shipments have been, at the least, relatively stable, which we expect to continue into 1Q. The Chinese smartphone market is maturing, and with that comes slower growth and more macro affectations, which certainly seems to be the case in recent months. As that continues we expect the Chinese smartphone market to have basically the same competitive and economic characteristics of the global smartphone market and track more closely to the global markets each year. That said, Chinese brands have the advantage of lower cost, but also face some political issues, such as those in India, that can offset those cost advantages. It is up to both the Chinese government and Chinese smartphone brands as to how those issues will play out this year, and over the last year both did little to smooth those relationships that can help Chinese brands gain share outside of the Mainland. Maybe 2023 will be different, although it is still hard to be overly optimistic.

China Smartphone Shipments & Y/Y ROC - 2019 - 2022 - Source: SCMR LLC, CAIST

China Total & 5G Smartphone Shipments - Source: SCMR LLC, CAIST

CHina Domestic Brand Smartphone Shipment Share - Source: SCMR LLC, CAIST

RSS Feed

RSS Feed