Is BOE Planning a 3rd Gen 10.5 LCD Fab?

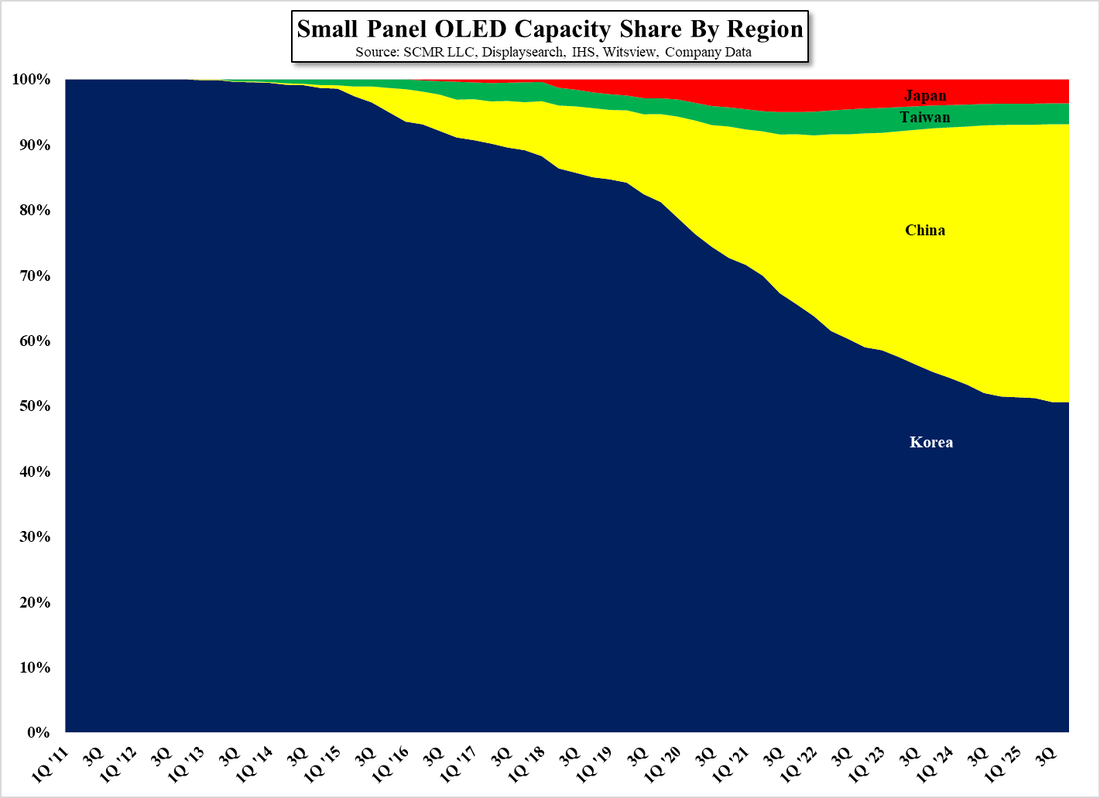

We have been hearing that the world’s largest LCD panel producer, BOE (200725.CH) has begun planning a new Gen 10.5 LCD fab project. While the company will not confirm anything official, BOE is already the global leader in large panel LCD production, and the addition of a 3rd Gen 10.5 LCD fab would certainly move them further ahead of their closest rival, fellow China countryman, Chinastar (pvt), who we expect will have a ~13.5% share of the global LCD market (capacity basis) against BOE’s 26.8% share at the end of this year. While we have yet to see any documents that verify the new project, it would not be surprising to imagine BOE wanting to further capitalize on the large increases seen in LCD panel prices over the last year.

BOE’s last two Gen 10.5 fabs have a stated capacity of 120,000 sheets/month, and while speculation about the new fab is calling for 150,000 sheet/month capacity, we are, at least for now, adding 120k to our fab database, as duplicating an existing fab is always easier and less expensive than changing the configuration. Timing is still a big question, as no announcements have been made, but we plan an announcement, if the project is approved by the board, in September, which would lead us to a phase 1 opening of June 2023 and a phase 2 opening of March 2024, with both ramping to full production over roughly 10 to 12 months. The ramp will begin to increase BOE’s global capacity share in 2023, and more so in 2024 and 2025, although much will depend on the timing and how quickly BOE can find customers to fill the new fab. The table below compares our expectations for BOE’s gross LCD capacity share under current circumstances and with the inclusion of this new Gen 10.5 fb.

BOE’s last two Gen 10.5 fabs have a stated capacity of 120,000 sheets/month, and while speculation about the new fab is calling for 150,000 sheet/month capacity, we are, at least for now, adding 120k to our fab database, as duplicating an existing fab is always easier and less expensive than changing the configuration. Timing is still a big question, as no announcements have been made, but we plan an announcement, if the project is approved by the board, in September, which would lead us to a phase 1 opening of June 2023 and a phase 2 opening of March 2024, with both ramping to full production over roughly 10 to 12 months. The ramp will begin to increase BOE’s global capacity share in 2023, and more so in 2024 and 2025, although much will depend on the timing and how quickly BOE can find customers to fill the new fab. The table below compares our expectations for BOE’s gross LCD capacity share under current circumstances and with the inclusion of this new Gen 10.5 fb.

We note that BOE’s plans for its earlier Gen 10.5 LCD fabs were delayed from their original timeline, in part because of COVID-19, but also as a reflection of what were declining large panel LCD prices. As those prices have increased, the expected profitability of new fabs, at current panel pricing, is very attractive and makes a strong case for government subsidies that now expect to see some sort of return, aside from job creation. BOE’s management has stated that it believes the LCD display industry is exiting an era of cyclicality and becoming a more mature and more predictable industry.

While we agree with the fact that the LCD display space is maturing, we are not convinced that cyclicality is being washed out of the industry. LCD displays will still have to compete with OLED and other potential display technologies, and while mini-LED backlighting and quantum dot enhancement can help to bring LCD specs closer to other display technologies, consumers want bigger and better TVs at lower prices and that means continued competition. Unless the world has permanently changed due to COVID-19, there will always be periods of supply/demand imbalance, during which the profitability of LCD fabs will be marginal. Building a Gen 10.5 fab does give BOE and others an efficiency advantage over older Gen 8.5 LCD fabs, especially with larger LCD panels (65” and over), but assuming that everything will remain the same as it is now years into the future is a dangerous game.

While we agree with the fact that the LCD display space is maturing, we are not convinced that cyclicality is being washed out of the industry. LCD displays will still have to compete with OLED and other potential display technologies, and while mini-LED backlighting and quantum dot enhancement can help to bring LCD specs closer to other display technologies, consumers want bigger and better TVs at lower prices and that means continued competition. Unless the world has permanently changed due to COVID-19, there will always be periods of supply/demand imbalance, during which the profitability of LCD fabs will be marginal. Building a Gen 10.5 fab does give BOE and others an efficiency advantage over older Gen 8.5 LCD fabs, especially with larger LCD panels (65” and over), but assuming that everything will remain the same as it is now years into the future is a dangerous game.

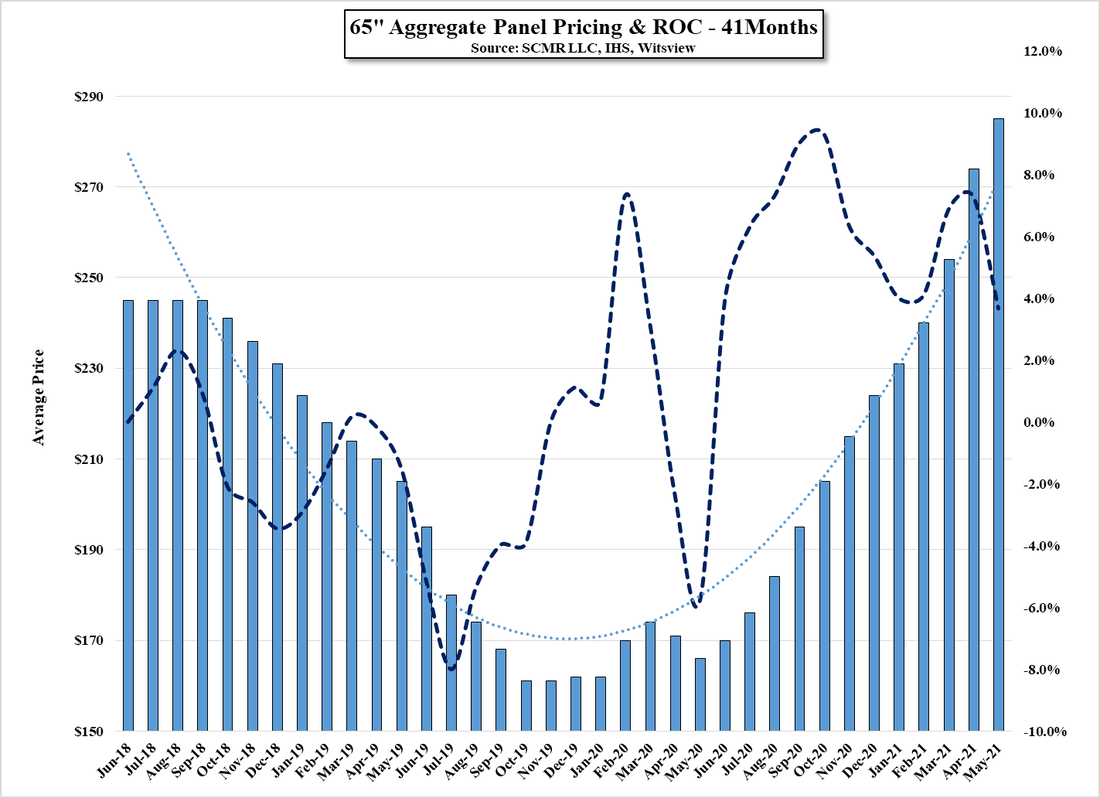

65" Aggregate Panel Pricing & ROC - 41 Months - Source: SCMR LLC, IHS, Witsview

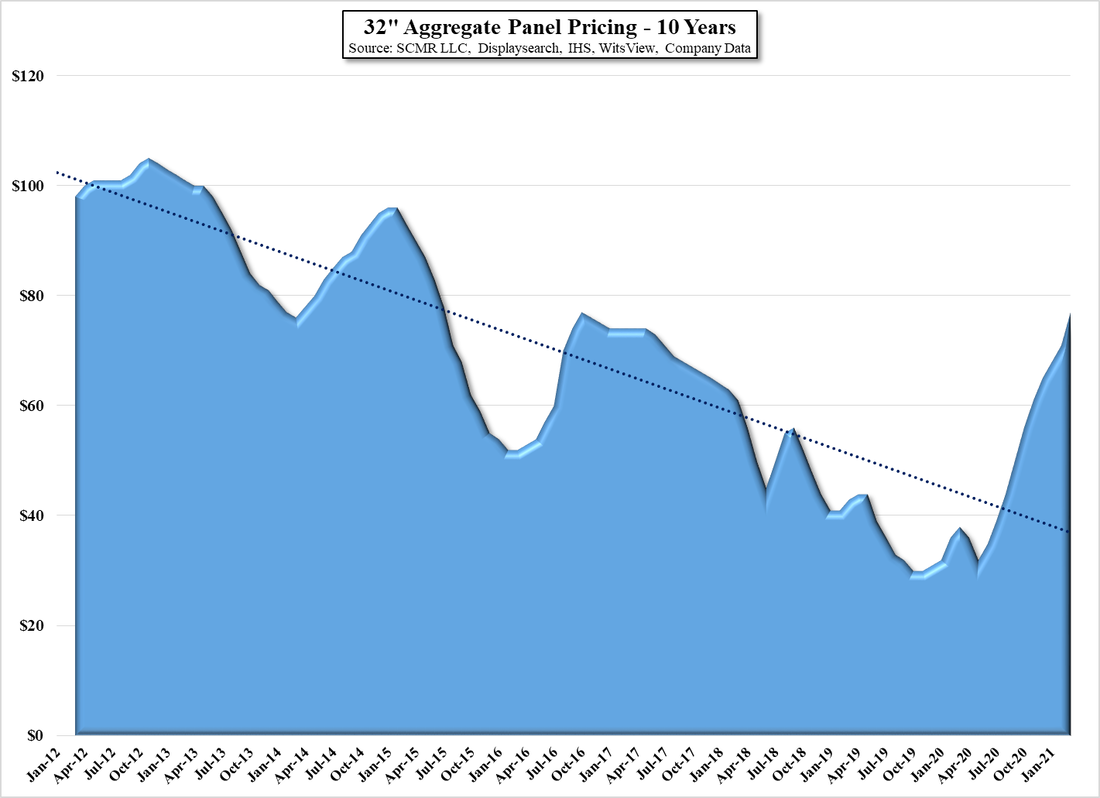

32" Aggregate Panel Pricing - 10 Years - Source: SCMR LC Displaysearch, IHS, Witsview, Company Data

RSS Feed

RSS Feed

{kind=link}