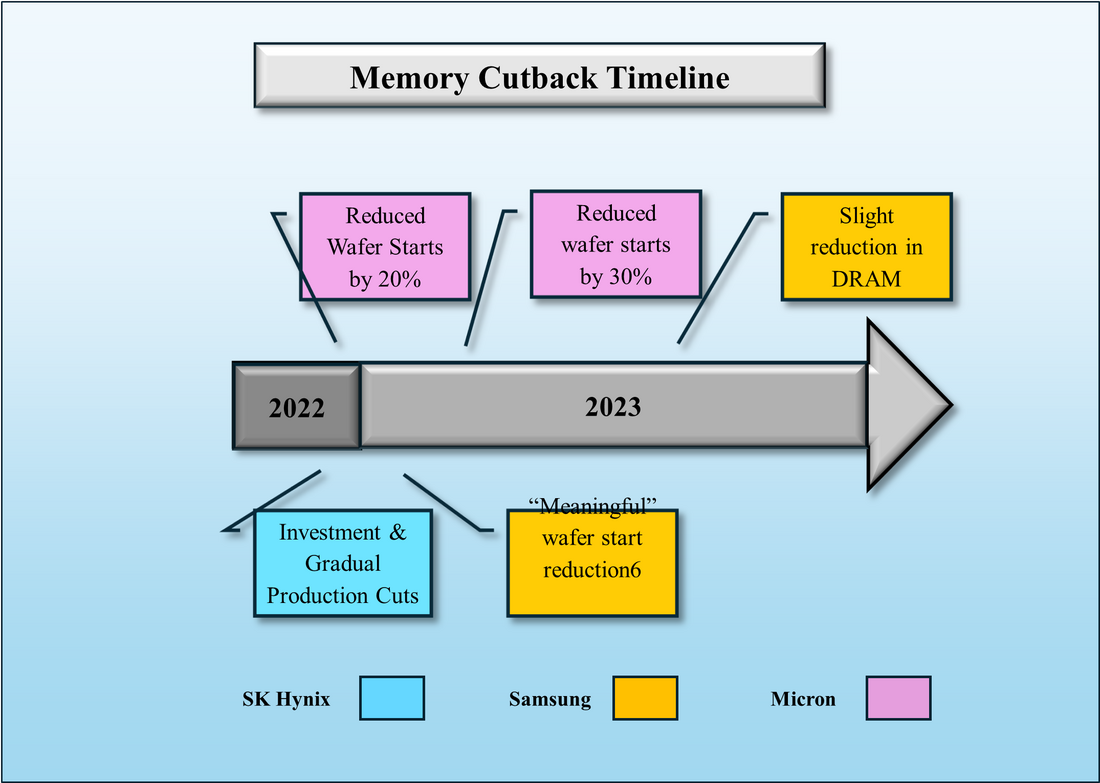

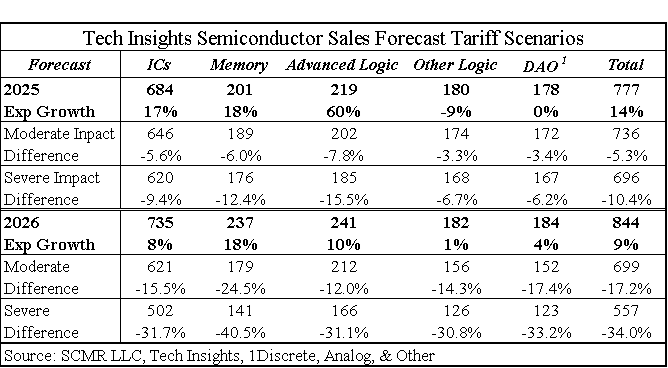

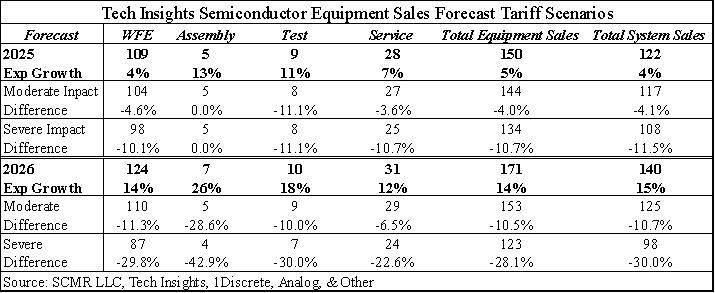

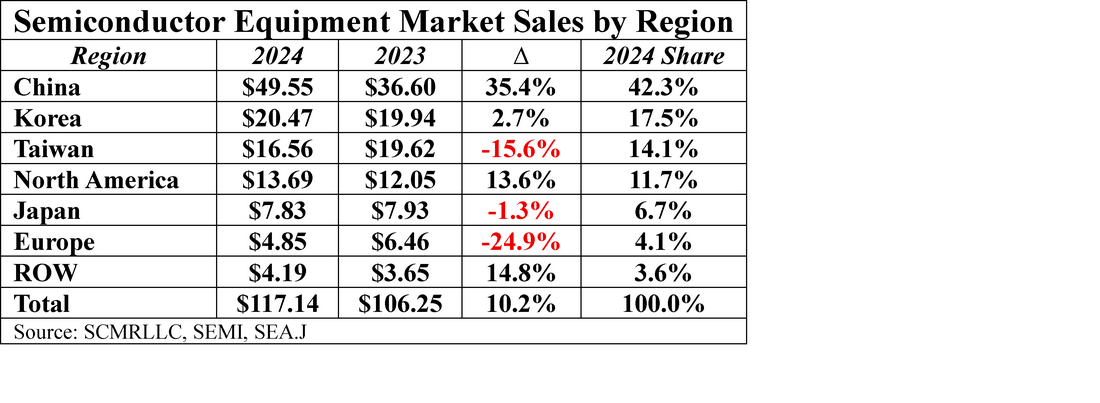

Fun with Data – Semi Ecosystem

The current White House has decried the US Chips Act as a wasteful and a poor strategy (direct subsidies), although it remains in place, with the obvious desire to “bring back the semiconductor business to the US” through tariffs. While the US does not dominate the manufacturing of advanced semiconductors, we have a very robust semiconductor ecosystem that is a leader in the development of semiconductor products and semiconductor technology. Semiconductor Engineering has completed the daunting task of listing 544 US semiconductor institutions in the US semiconductor ecosystem which we have analyzed.

The dataset shows the company/Institution name, the city and state where located, the business type and the activity. To clarify, there are 9 business types and 6 Activities:

Business Types

The dataset shows the company/Institution name, the city and state where located, the business type and the activity. To clarify, there are 9 business types and 6 Activities:

Business Types

- Fabless – 67

- Foundry – 27

- Equipment – 41

- Materials – 58

- IDM (Integrated Device Manufacturer) – 221

- OSAT (Outsourced Assembly & Test) – 4

- IP & EDA (Electronic Design Automation) – 18

- Research & Development – 4

- University R & D Partner - 104

- Fabless – 1

- IDM – 11

- Materials – 3

- Chip Design – 150

- Manufacturing – 196

- Research & Development – 183

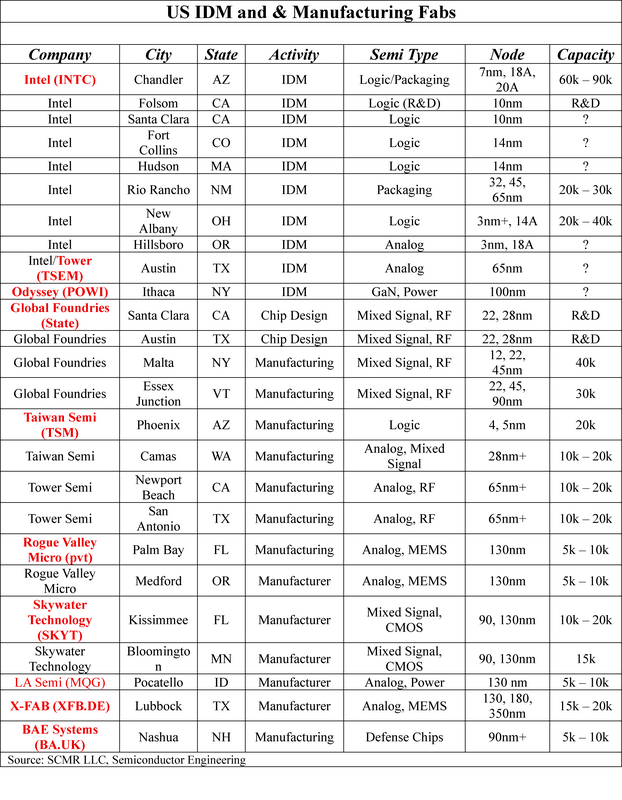

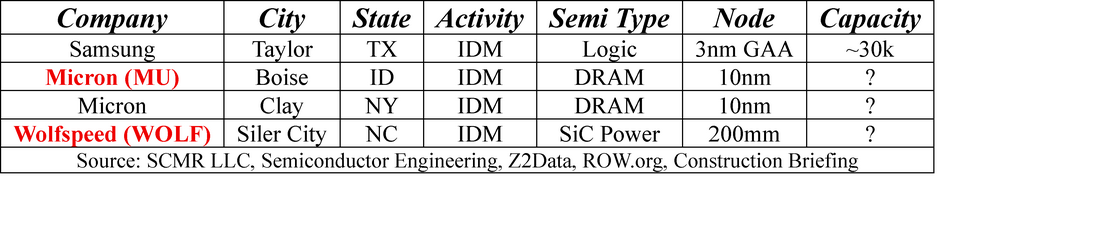

Intel is the only US company that produces advanced semiconductors in the US (10nm or less), and while the current goal is to spur semiconductor production in the US, the CHIPS program has done an impressive job in bringing foreign semiconductor producers into the US. Below is a list of those fabs currently under construction in the US. Notably, all are US companies other than the Samsung (005930.KS) Taylor fab, but only the Samsung fab will produce logic.

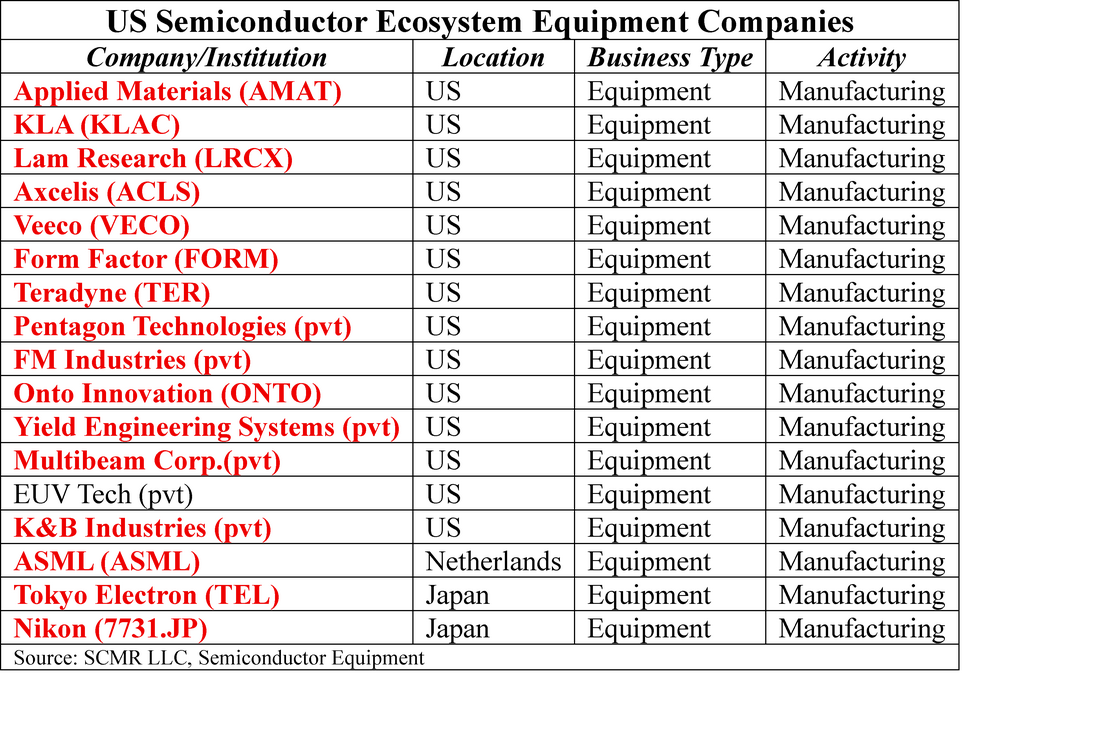

We pull out from the list those companies listed as Business Type – Equipment and Activity as Manufacturing, almost all of which are US based companies:

So while the US does not have much of a local company advanced logic production force, it does have a dominant semiconductor equipment manufacturing and design ecosystem, particularly for advanced products. Unfortunately tariffs and export restrictions limit the growth of this business, which gets little government support. Encouraging local EDA company growth might be a more feasible path for government sponsored subsidy programs, allowing these companys to push the limits of advanced logic and packaging that will allow US foundries, whether owned by US companies or by others, to flourish. Rather than forcing the expansion of US advanced semicomductor manufacturing, a process that will take many years, as long as advanced chips are being produced onshore, less attention should be paid to who is producing them and more toward what they are producing. If our chip design solutions advance more quickly than others, the US semiconductor business will have a distinct advantage over other countries.

RSS Feed

RSS Feed