LG to add OLED phones to lineup

LG Electronics is expected to be adding OLED displays to its smartphone lineup for the first time since the October 2013 launch of the G Flex and the follow-up G Flex 2 in January 2015, both of which were built on plastic OLED substrates. The upcoming V30 smartphone, which remains unannounced by LG, is expected to have an OLED display (5.7” or larger) with the potential for conformed edges, and the G7 smartphone, the successor to the current LG flagship G6 (released in March) is also expected to be based on OLED technology.

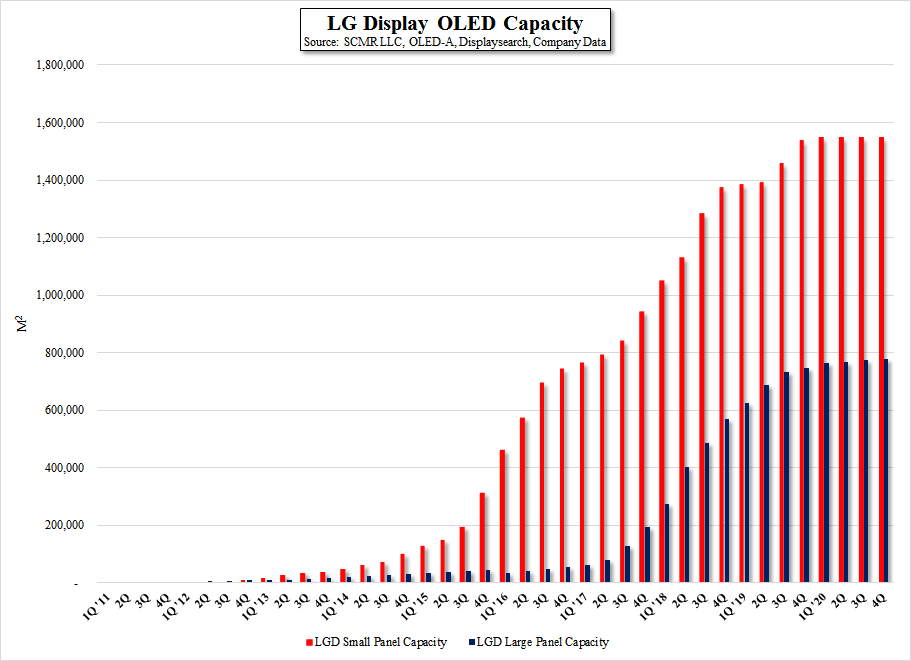

We note that while LG Electronics is known for their OLED TVs, LG Display (LPL) their display production arm, has capabilities for both large panel and small panel OLED production and has been producing OLED displays for other customers, including China based Xiaomi (pvt) as we noted in our 04/19/17 note, and while it is difficult to absolutely classify fabs as ‘small panel’ or ‘large panel’, as they can be repurposed if absolutely needed, we classify small panel fabs as those less than Gen 7 and large panel fabs as those Gen 7 or above. The chart below shows LG Display’s OLED capacity, although it includes capacity for LGD’s OLED lighting fab which we expect to begin production at the end of this year and would not be used for small panel OLED production. LGD will have small panel OLED capacity from three fabs by the end of this year and should be able to easily meet LG Electronics demand for rigid or flexible small panel OLED displays, even with low yields, but the question of ability to produce a conformed display similar to the Samsung S8, is really what is at stake. Samsung Display (pvt) has had significant manufacturing experience producing such displays, while LGD has not, and the ability to produce high quality conformed displays for its parent will be a challenge for LGD.

That said, we expect, regardless of the initial yield, they will be able to produce ‘flexible’ displays this year, and will eventually gain the expertise needed to bring yields up to LCD levels, at which point there will be a viable competitor to Samsung Display’s domination of the small panel OLED display production space. Pressed for timing, we would expect LGD to be in volume production for a conformed OLED smartphone display by mid 2018, and possibly earlier.

We note that while LG Electronics is known for their OLED TVs, LG Display (LPL) their display production arm, has capabilities for both large panel and small panel OLED production and has been producing OLED displays for other customers, including China based Xiaomi (pvt) as we noted in our 04/19/17 note, and while it is difficult to absolutely classify fabs as ‘small panel’ or ‘large panel’, as they can be repurposed if absolutely needed, we classify small panel fabs as those less than Gen 7 and large panel fabs as those Gen 7 or above. The chart below shows LG Display’s OLED capacity, although it includes capacity for LGD’s OLED lighting fab which we expect to begin production at the end of this year and would not be used for small panel OLED production. LGD will have small panel OLED capacity from three fabs by the end of this year and should be able to easily meet LG Electronics demand for rigid or flexible small panel OLED displays, even with low yields, but the question of ability to produce a conformed display similar to the Samsung S8, is really what is at stake. Samsung Display (pvt) has had significant manufacturing experience producing such displays, while LGD has not, and the ability to produce high quality conformed displays for its parent will be a challenge for LGD.

That said, we expect, regardless of the initial yield, they will be able to produce ‘flexible’ displays this year, and will eventually gain the expertise needed to bring yields up to LCD levels, at which point there will be a viable competitor to Samsung Display’s domination of the small panel OLED display production space. Pressed for timing, we would expect LGD to be in volume production for a conformed OLED smartphone display by mid 2018, and possibly earlier.

LG Display OLED Capacity - Source: SCMR LLC, OLED-A, Displaysearch, Company Data

RSS Feed

RSS Feed