OLED Laptops

OLED smartphones have been around technically since 2003, although the one OLED smartphone in that year, the Amoi S6, had only a 128 x 128 pixel grayscale OLED display, with Samsung releasing the first full color OLED display in 2004, sporting a massive 1.8” screen on its X120, and LG Electronics following in 2005 with a dual OLED display smartphone, the L5000, and by 2010 there were over 100 OLED smartphone models to choose from. OLED tablets took a bit longer given the larger screen size, with Samsung’s Tab 7.7 in late 2011, although the use of OLED in tablets took longer to develop.

Amoi S6 - Source: GSMArena

With estimates of almost 600m OLED smartphones being produced and over 700m small to mid-sized OLED devices total this year, OLED is no longer a ‘new’ technology and has found a significant place in the display world, but RGB OLED, the type that is used in such devices, has not progressed to IT devices, or has it? We have looked at the laptop market, which would be the logical next-step for OLED displays, and were surprised to find such a large number of OLED laptops. However we also found large discrepancies in estimates for the growth of that market, which is not all that surprising considering there are many ways it can be sliced, such as notebooks, all-in-ones, laptops, gaming laptops, Chromebooks, and even tablets, all of which can be included or excluded from estimates. This leads to vast inconsistencies but using even the lowest possible estimate sources, ~2.6m units this year, the space is growing rapidly from almost nothing (~150,000 units) in 2019.

There are some limiting factors, particularly on the supply side as this relatively new segment must compete for capacity against high volume OLED smartphones, tablets, and smartwatches, all of which have well-established customers and justifiable pricing. Large scale small panel OLED producers, such as Samsung Display (pvt), LG Display (LPL) and BOE (200725.CH), are careful to keep supply closely matched to demand, and even with smaller Chinese OLED producers nipping at their heels, are careful not to over-expand and crater small panel OLED pricing. However, if even the least aggressive estimates are calling for rapid expansion in the OLED notebook space, small panel OLED display producers will have to begin to dedicate more RGB OLED production to what are considerably larger notebook panel sizes, and with Apple (AAPL) looking to join the OLED tablet/laptop fray next year after converting its entire smartphone line, it is a topic close to the hearts of all small panel OLED suppliers.

Right now, OLED laptops come in two sizes almost exclusively, ~13.3” and 15.6”. There are exceptions, but those two sizes are the current norm. If we compare those two sizes against a typical 6.8” 9:16 smartphone display, the 13.3” notebook will take up 3.9 times the substrate space of the smartphone, while the 15.6” notebook would take up 5.3 times the substrate space, simply meaning that in a static capacity model if the mix between laptop sizes were even, the 2.6m OLED laptop estimate for this year would reduce the number of smartphones produced by over 12m units, creating a 2.1% shortfall in small panel OLED smartphone capacity. While these numbers do match exactly to absolute fab production rates, they give a better understanding as to how the competition for small panel OLED capacity will fare as the OLED notebook market develops.

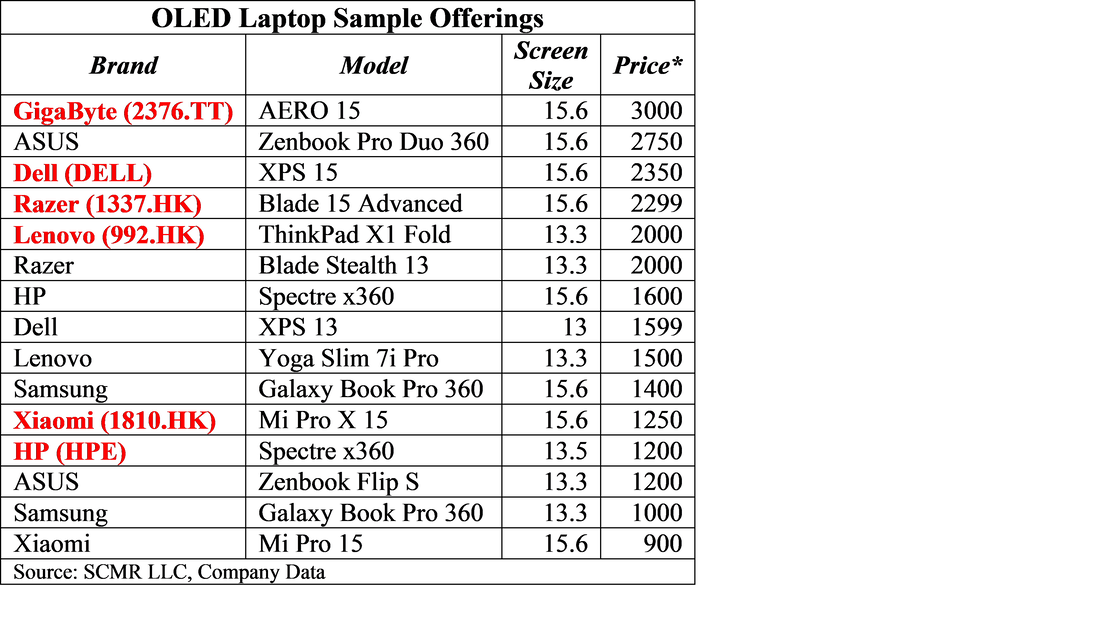

The number of OLED based notebooks varies on a daily basis as newer versions of models are added and older models are sold out, and not all models are available in the US, but the table below gives a sampling of some of those that have been announced and (hopefully) are available currently. We note also that while some models show up on Amazon (AMZN) or Best Buy (BBY) sites, they are out of stock due to component shortages, and pricing, which we show only for reference, varies considerably with processor, memory, and drive configuration. The pricing range is what we consider the most important.

There are some limiting factors, particularly on the supply side as this relatively new segment must compete for capacity against high volume OLED smartphones, tablets, and smartwatches, all of which have well-established customers and justifiable pricing. Large scale small panel OLED producers, such as Samsung Display (pvt), LG Display (LPL) and BOE (200725.CH), are careful to keep supply closely matched to demand, and even with smaller Chinese OLED producers nipping at their heels, are careful not to over-expand and crater small panel OLED pricing. However, if even the least aggressive estimates are calling for rapid expansion in the OLED notebook space, small panel OLED display producers will have to begin to dedicate more RGB OLED production to what are considerably larger notebook panel sizes, and with Apple (AAPL) looking to join the OLED tablet/laptop fray next year after converting its entire smartphone line, it is a topic close to the hearts of all small panel OLED suppliers.

Right now, OLED laptops come in two sizes almost exclusively, ~13.3” and 15.6”. There are exceptions, but those two sizes are the current norm. If we compare those two sizes against a typical 6.8” 9:16 smartphone display, the 13.3” notebook will take up 3.9 times the substrate space of the smartphone, while the 15.6” notebook would take up 5.3 times the substrate space, simply meaning that in a static capacity model if the mix between laptop sizes were even, the 2.6m OLED laptop estimate for this year would reduce the number of smartphones produced by over 12m units, creating a 2.1% shortfall in small panel OLED smartphone capacity. While these numbers do match exactly to absolute fab production rates, they give a better understanding as to how the competition for small panel OLED capacity will fare as the OLED notebook market develops.

The number of OLED based notebooks varies on a daily basis as newer versions of models are added and older models are sold out, and not all models are available in the US, but the table below gives a sampling of some of those that have been announced and (hopefully) are available currently. We note also that while some models show up on Amazon (AMZN) or Best Buy (BBY) sites, they are out of stock due to component shortages, and pricing, which we show only for reference, varies considerably with processor, memory, and drive configuration. The pricing range is what we consider the most important.

RSS Feed

RSS Feed